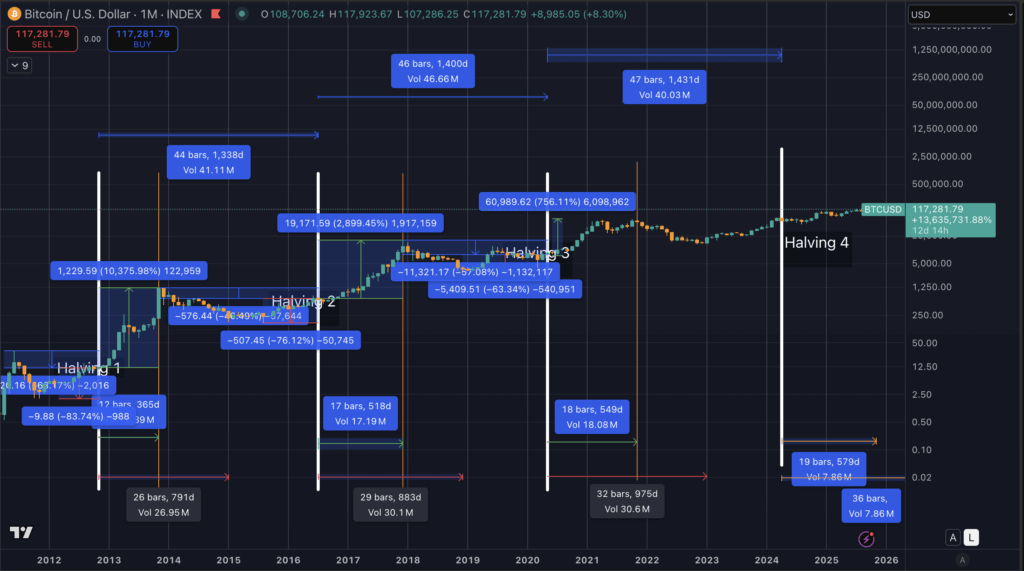

Bitcoin’s value is hovering near $117,000 as market observers analyze the impact of the Federal Reserve’s recent interest rate adjustment, and as a significant 1,065-day milestone post-halving draws near.

Following the Fed’s 0.25% rate reduction yesterday, Bitcoin now finds itself at a crucial intersection. Policy changes and a historical cycle marker, as highlighted by Axios, suggest this 1,065-day period after a previous cycle’s lowest point has often coincided with a “peak valuation”.

This critical assessment window extends through the end of September and the beginning of October. Subsequently, the market’s performance leading up to Thanksgiving will be dictated by capital flows, the dollar’s strength, and interest rate dynamics. These factors will determine whether the upward trend continues or if a topping-out phase, similar to past cycles, begins, potentially leading to price corrections between 40% and 60%, according to Axios.

The demand for spot ETFs is a vital component to monitor, as this transforms the cycle into a question of supply and demand. CoinShares’ latest fund flow report indicates a revival of net inflows into U.S. spot Bitcoin ETFs during late August and early September, totaling billions. SoSoValue also noted a streak of inflows mid-September, highlighted by roughly $260 million invested on September 15.

These numbers stand in contrast to the roughly 452 Bitcoins issued each day after the halving, which is computed at 3.125 Bitcoins per block multiplied by approximately 144 blocks. When ETF demand absorbs multiple thousands of Bitcoins each week, the market faces limitations selling holdings at peak levels, which can cause market top patterns to be gradual plateaus, not abrupt peaks.

Macroeconomic conditions represent the second major influencer.

This month, the euro reached a four-year peak versus the dollar, fueled by growing expectations of rate reductions, while short-term Treasury yields decreased leading into the meeting.

A weakened dollar generally fosters easier global financial conditions and is often correlated with a rise in risk-sensitive assets. Simultaneously, domestic inflation has subsided from the prior year’s high, with the headline Consumer Price Index (CPI) at 2.5% year-over-year in August and the core rate at 3.0%, as reported by the Bureau of Labor Statistics.

The policy outcome is key to shaping whether these supportive conditions persist or wane. For the remainder of 2025, rate cuts coupled with dovish communication, emphasizing progress on inflation without hinting at swift reversals, would likely sustain the dollar’s downward trend and support risk-taking.

Conversely, rate cuts signaling vigilance regarding inflation and limiting further easing could keep interest rates steady, diminishing the upward momentum. The scenario of no rate cut had a low chance of materializing, but it could have tightened financial conditions as the quarter ended, placing heavier reliance on ETF demand to maintain the market’s health.

Bitcoin mining profitability provides context for how significantly price movements affect the supply side. Hashrate has been fluctuating around 1.0 to 1.12 zettahash per second in recent weeks, and network difficulty is near a record high of approximately 136 trillion, according to data collected by Hashrate Index.

Consequently, hashprice has stayed at around 53 to 55 dollars per petahash per day, which is consistent with Luxor’s spot values this month. Given that hashprice is generally proportional to Bitcoin price, but inversely related to hashrate, future ranges in the fourth quarter (Q4) can be approximated by considering potential price pathways alongside moderate increases in hashrate as new mining equipment is activated. Given that fees remain minimal, price plays the primary role in the cash flow available to miners.

A basic benchmark clarifies the data feeding projections spanning from the present through Thanksgiving Day, November 27.

| Baseline input | Value | Source or method |

|---|---|---|

| Spot price anchor | ~$116,000 | Current market price |

| Implied volatility | ~30–40% (near-dated) | Deribit DVOL context in early September |

| Issuance | ~452 BTC/day | 3.125 BTC reward × ~144 blocks |

| Hashrate | ~1.0–1.1 ZH/s, trending up | Hashrate Index |

| Hashprice | ~$53–$55 per PH/day | Luxor spot readings |

Utilizing these inputs, the table below presents potential price and miner hashprice ranges through late November, factoring in varying policy stances and ETF flows. It is important to note these represent broad ranges, not precise targets. These illustrate how the tone of rate adjustments and capital flows influence both price and miner revenue under low-fee circumstances and gradual hashrate expansion.

| ETF flows \\ Fed outcome | Cut, dovish tone | Cut, hawkish tone | No cut |

|---|---|---|---|

| Sustained net inflows (multi-week >$1–2B) | BTC $125k–$145k, hashprice $57–$66/PH/day | BTC $110k–$125k, hashprice $48–$58/PH/day | BTC $105k–$120k, hashprice $45–$55/PH/day |

| Flat or net outflows | BTC $115k–$125k, hashprice $50–$57/PH/day | BTC $95k–$110k, hashprice $40–$50/PH/day | BTC $80k–$95k, hashprice $33–$45/PH/day |

The cycle’s stage is crucial for interpreting these ranges.

Axios suggests that past “peak valuations” have commonly occurred around the 1,065-day mark, after which drawdowns began, that were milder in the ETF era than in prior cycles. This provides a secondary signal for investors analyzing trends into early October.

My own analysis pinpointed November 1 as a possible date for the cycle peak, based on historical observations that previous cycle peaks were roughly 100 days after the most recent halving event.

However, strong ETF demand, even if the window suggests a high, could produce a gradual peak and gentler price corrections.

Should the window pass without seeing a new peak, and if flows turn uneven, the market could potentially shift towards the middle ranges of the grid, with prices fluctuating below the existing peak and hashprice limited by gradual hashrate expansion.

Policy decisions will swiftly influence data trends. As reported by Business Insider in their analysis of meeting outcomes, a dovish rate adjustment tends to weaken the dollar and steepen the risk appetite curve, which has historically attracted further investment into both stocks and cryptocurrency. Conversely, a hawkish rate reduction narrows that curve and places more emphasis on unique factors within each asset class.

A decision to not cut rates would have likely tested the lower levels shown in the table, as it removes the near-term stimulus and tends to bolster the dollar’s strength. As BLS reports indicate, the CPI data might lessen the need for unexpected restrictive measures. However, the chairman’s emphasis on data dependence could create uncertainty around the future direction of interest rates, even if a first rate cut does happen.

ETF flow trends are the clearest high-frequency metrics for monitoring against this policy context. CoinShares’ weekly reports offer information on size and regional breakdown, while SoSoValue’s daily reports detail whether investment interest increases or subsides after announcements.

Converting these metrics into supply absorption is quite simple.

At Bitcoin prices ranging from $115,000 to $120,000, $1 billion of net investment translates to approximately 8,300 to 8,700 Bitcoin. Weekly net inflows of $1.5 billion to $2.5 billion equate to 13,000 to 21,000 Bitcoin, or approximately four to seven times the weekly issuance.

Consistent ratios exceeding one, despite moderate outflows on certain days, create a structural cushion for spot prices, potentially decreasing volatility and compressing the left tail in the higher ranges of the grid.

Miner financial statements will serve as a leading indicator if price declines to the lower bands. With the difficulty levels near a record and electricity costs rising for select miners, price declines toward $95,000 coupled with steady hashrate values would push hashprice down into the low 40s per petahash per day.

At this point, hedging operations and delaying of capital expenditures will likely resume, instead of mass shutdowns, but thresholds do vary by company. Data from Hashrate Index on public miner expansion plans shows there is ongoing capacity growth in the pipeline, so hashrate expansion of 3 to 7 percent into November is a reasonable assumption to make for the table above.

The core narrative remains the same approaching Thanksgiving.

The market is weighing a prospective rate reduction that will influence the dollar and short-term interest rates, the level of ETF net demand absorbing or releasing supply compared to the 452-Bitcoin daily issuance rate, and an upcoming 1,065-day cycle mark that Axios has said typically lines up with a cycle high, followed by a decline.

The window for this outcome occurs in late September and early October, and then attention shifts to seeing if capital flows and general economic situations that occur post-decision confirm or deny the usual cycle progression.