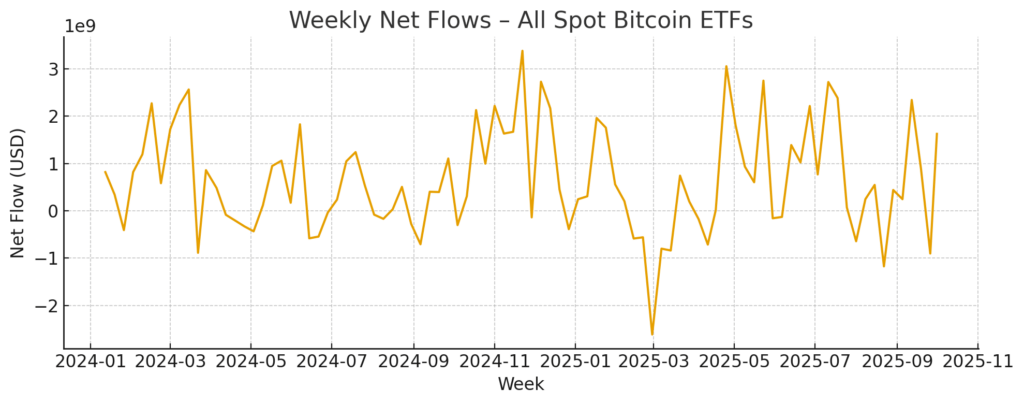

Bitcoin ETFs in the United States experienced a substantial boost last week, pulling in $1.63 billion. This pushes the net intake for the past four weeks to $3.96 billion, marking positive inflow trends for nine of the last twelve weeks.

Over the most recent 12-week period, these ETFs have accumulated $6.08 billion. This figure sits comfortably in the middle range for the year 2025, according to proprietary tracking data compiled from fund disclosures and publicly available flow tables.

Looking at the year-to-date performance, net inflows have reached a total of $22.78 billion, with an even more impressive $58.44 billion since the ETFs were first introduced.

The aggregate assets under management are estimated at $155.9 billion. The average weekly trading volume for the last four weeks stands at $16.17 billion, slightly below the 12-week average of $17.90 billion.

Inflows Strengthen as Quarter Transitions Amid Evolving Policy and Macro Environment.

The Federal Reserve’s interest rate reduction in September, coupled with market expectations of further easing in the fourth quarter, creates a more favorable environment for rate-sensitive investors who utilize ETFs to increase their exposure to Bitcoin.

The initial day of the U.S. government shutdown coincided with gold reaching record highs and a weakening dollar. Historically, this combination of assets has often aligned with stronger performance for crypto exchange-traded products (ETPs). Data from global products confirm this trend.

CoinShares reported consistent weekly inflows through the end of September. Bitcoin attracted the majority of these investments, with $1.03 billion flowing into digital asset funds in the week ending September 29th, of which $790 million was specifically allocated to Bitcoin investment vehicles. Liquidity is primarily concentrated within the ETF market.

Kaiko Research has observed that trading depth during U.S. market hours has increased since the introduction of Bitcoin ETFs. Additionally, they found that ETF net flows account for a relatively small portion of daily Bitcoin returns, with an R² value close to 0.32. This highlights the continuing significant influence of derivatives and broader macroeconomic factors on Bitcoin’s price volatility.

As we enter Q4, simple calculations can illustrate potential net flow scenarios and estimate how much Bitcoin could be removed from the available supply.

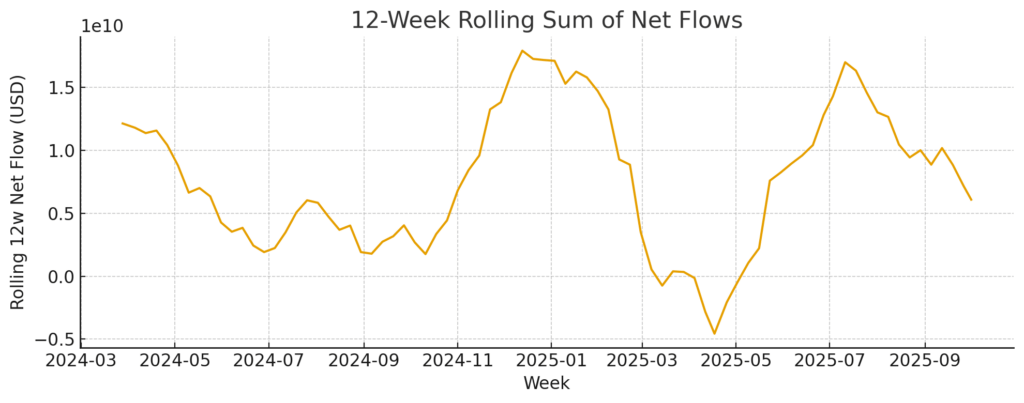

The recent four-week trend annualizes to roughly $12.9 billion for the quarter, while the 12-week average indicates approximately $6.6 billion. The highest and lowest points from 2025 provide the extreme bounds of these estimates.

Assuming a Bitcoin price of $115,000, every $1 billion in net inflows over a four-week period translates to approximately 8,700 BTC being acquired, or around 311 BTC per day.

After the halving event, Bitcoin issuance averages approximately 450 BTC per day, which equates to roughly 41,400 BTC over a 92-day quarter. The table below summarizes these rates and their potential impact on Q4 totals.

| Scenario | Assumption | Q4 net flows (USD) | BTC absorbed at $115k | vs. miner issuance |

|---|---|---|---|---|

| Bull, retouch 2025 best 12-week pace | +$17.1B per 12 weeks | ~+$18.5B | ~161,000 BTC | ~3.9× quarterly issuance |

| Base, sustain last 4-week pace | +$3.96B per 4 weeks | ~+$12.9B | ~112,000 BTC | ~2.7× |

| Moderate, revert to 12-week average | +$6.08B per 12 weeks | ~+$6.6B | ~57,000 BTC | ~1.4× |

| Bear, revisit 2025 worst 12-week run | −$4.56B per 12 weeks | ~−$4.9B | ~−43,000 BTC | ≈−1.0× |

In the Base scenario, U.S. spot Bitcoin ETFs could potentially remove approximately 112,000 BTC from the circulating supply this quarter, representing around 2.7 times the amount of newly issued Bitcoin. Such a reduction typically tightens spot market availability and provides support to the underlying asset when risk appetite remains stable.

The August Consumer Price Index (CPI) registered at 2.9 percent year-over-year, strengthening the narrative of disinflation combined with easing monetary policy, which fuels investor demand.

Seasonality also plays a role, with investors often highlighting October’s historically positive performance for cryptocurrencies.

The rolling 12-week sum of net flows indicates a convergence toward the average after peaking in mid-July. Recent weekly inflows surpass this average trend, suggesting a possible shift from past patterns.

However, if historical trends prevail, net outflows could potentially reach around $500 million per week by December.

The Market Structure Continues to Adapt to ETF Activity.

Kaiko’s research indicates increased trading activity around the periods when U.S. ETFs are created and redeemed. Liquidity during these times has a greater impact on price discovery than before the launch of ETFs, explaining price stability even with mixed flow patterns.

The correlation analysis, where ETF flows only partially explain daily returns, emphasizes the importance of macroeconomic data releases, funding conditions, and positioning on the CME exchange. Traders monitoring futures open interest and volume can leverage CME metrics to confirm risk appetite in conjunction with fund flows. Kaiko’s dashboards offer a comprehensive view of market depth and spreads across different trading venues.

Asset rotation remains a factor. U.S. spot Ethereum ETFs have consistently attracted investment since July, and recent analysis suggests that ETH is gaining relative ground. Reuters reported that Citi increased its year-end ETH price target while reducing its BTC target, citing perceived shifts in investor allocations.

Currently, the U.S. remains the primary driver of demand in this cycle, and CoinShares’ late-September data showed that Bitcoin still dominates weekly investments across global ETPs.

Near-term risks are primarily tied to data releases and policy decisions.

The government shutdown could potentially delay or distort key macroeconomic indicators like nonfarm payrolls and the CPI, leading to increased narrative volatility given the limited reliable information available to investors.

This makes the ETF flow data an even more important indicator of risk sentiment as Q4 begins.

If the current four-week pace is sustained, quarter-to-date net inflows would approach $13 billion by the end of the year.