Subject to regulatory clearance, CME Group is planning to expand its trading hours for Bitcoin and Ethereum futures to 24 hours a day, beginning in early 2026. Check the official announcement.

This move will bring the biggest futures market in the United States into alignment with the continuous trading environment of cryptocurrency exchanges. This pivotal change has the potential to alter the way liquidity is distributed between conventional finance and cryptocurrency platforms.

Currently, CME futures trading occurs from Sunday to Friday, with routine breaks each day, mirroring the operational model for stocks and commodities. This arrangement leaves extended periods (Friday evening to Sunday afternoon, as well as brief pauses during the week) when the global spot market operates on exchanges like Binance, Coinbase, and Deribit without a corresponding CME market presence.

This situation has led to what is known as the “CME gap,” where price fluctuations during weekends or off-hours often result in noticeable gaps on trading charts when the market reopens, which traders often try to exploit. By 2026, these gaps may become less significant, or at least less predictable.

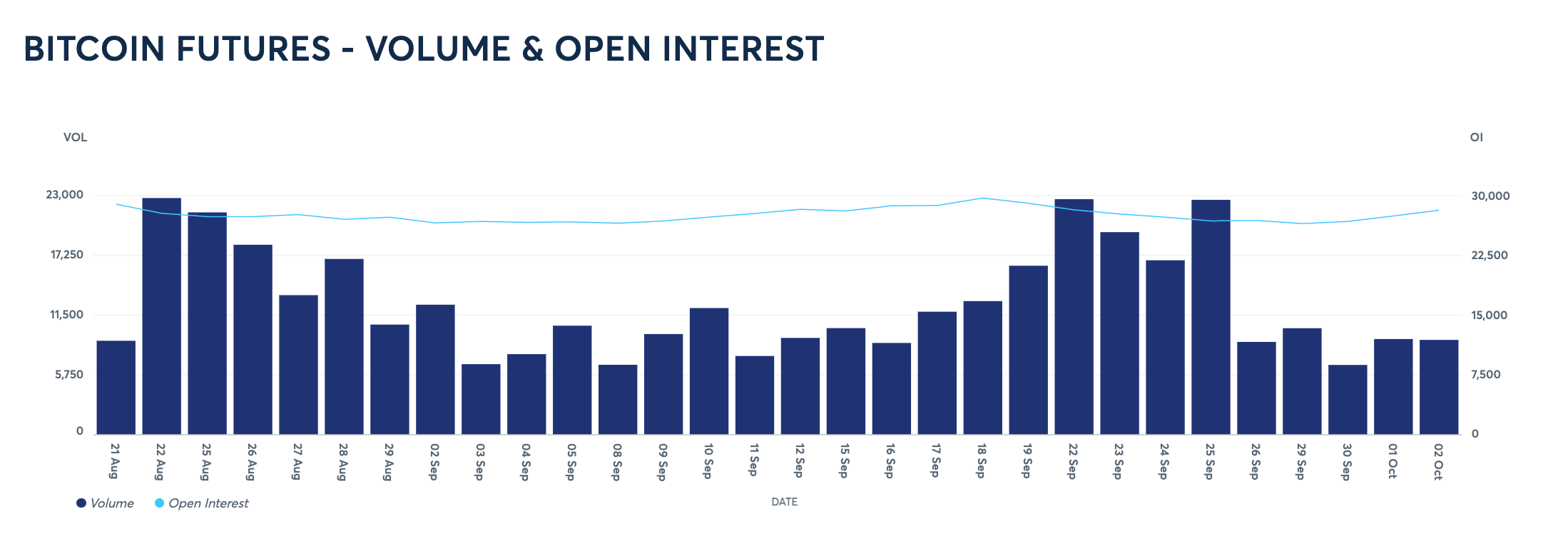

CME’s presence in the cryptocurrency market is already substantial. In the third quarter of 2025, the exchange achieved its second-highest quarterly performance for cryptocurrency futures, with an average daily trading volume close to 20,000 contracts across Bitcoin and Ethereum.

Specifically for Bitcoin, CME’s share of open interest has consistently ranked among the top five globally, frequently accounting for 20–25% of futures activity denominated in USD. This is a significant change from 2017, when CME launched its first Bitcoin contracts into a market primarily controlled by unregulated platforms.

The move to 24/7 trading is a direct response to client demand. Institutions, from asset managers to businesses, have voiced concerns about the inability to manage risk during the most volatile periods in cryptocurrency trading: weekends and Asian market hours.

A CME contract that mirrors Binance’s perpetual futures or Deribit’s options would allow portfolio managers in global financial hubs like New York or London to hedge exposure without needing to use offshore accounts. In addition, ETF market makers, who have contributed to a consistent stream of U.S.-based Bitcoin demand, can maintain balanced basis trades and arbitrage strategies around the clock.

The extended trading hours could have two key liquidity implications.

First, the “weekend effect,” where the price of Bitcoin can fluctuate significantly between Friday’s CME close and Sunday’s reopen, may diminish. This would reduce the built-in volatility premium affecting funding rates and options pricing.

Second, the gap between CME futures and cryptocurrency-native perpetual contracts, already a significant arbitrage opportunity, could narrow as institutional liquidity extends into previously unaddressed trading hours.

CME has stated that trading is planned to begin in early 2026, contingent on regulatory approval. With only a short time left in the current market structure, the focus is shifting from long-term positioning towards short-term trading opportunities. While weekend gaps and Friday closes will still be monitored, traders are beginning to consider the impact of these changes.

The remaining period before this significant change is unlikely to fundamentally alter market behavior. However, arbitrage desks and ETF market makers will have a limited time to capitalize on market inefficiencies before the 24/7 trading environment takes effect.

This is an important development for the Bitcoin market. The CME gap has been a recognized technical feature, closely watched and frequently traded upon by market participants. Its potential disappearance would close one of the few remaining structural gaps between institutional and cryptocurrency-native markets.

With around-the-clock CME contracts, Bitcoin trading will no longer be separated into “weekend” and “weekday” liquidity patterns. The same hedging and arbitrage activities that currently wait until Sunday evening will now be active at all times.

This adjustment may have wider implications for pricing models. Options dealers, ETF arbitrage desks, and basis traders have historically factored weekend risk into their funding calculations.

By the start of 2026, these premiums are expected to decrease, reducing the differences between CME futures and perpetual swaps on overseas exchanges.

This also suggests that the prevailing narrative of weekend volatility, where Bitcoin tends to experience the most significant price movements when traditional finance is closed, may fade, replaced by a more consistent approach to price discovery.