A preliminary legislative outline, currently under wraps and circulating among Democratic senators, suggests a significant tightening of regulations for the Decentralized Finance (DeFi) sector. The proposal reportedly seeks to impose Know Your Customer (KYC) and Anti-Money Laundering (AML) obligations on various DeFi elements, encompassing user interfaces, transaction validators, and even those operating network nodes.

Sources

indicate

the confidential document was conceived as a Democratic response to market-structure legislation supported in the House of Representatives. However, the bill has met internal pushback, potentially stalling discussions within the Senate Banking Committee.

The unreleased legislative language stipulates that DeFi applications facilitating monetary exchanges must implement KYC protocols, including web browser-integrated crypto wallets and liquidity exchange platforms.

Further, the draft legislation holds oracle operators responsible, potentially subjecting them to penalties if price data feeds connect to protocols under sanctions.

The Treasury Department may also gain the authority to designate a “restricted list” of protocols deemed excessively risky for use by individuals within the United States.

Senator Ruben Gallego stated that the Democratic proposal represents a good-faith effort to foster a bipartisan agreement regarding the regulatory framework for the cryptocurrency market.

In his words:

“Democrats have demonstrated a commitment to collaboration… They requested concrete proposals, and we have delivered.”

Market impact

This initiative has generated political friction in Washington, D.C., where Republican politicians and participants in the crypto industry express concerns that it could hinder technological advancement and cause Bitcoin and Ethereum liquidity to move overseas.

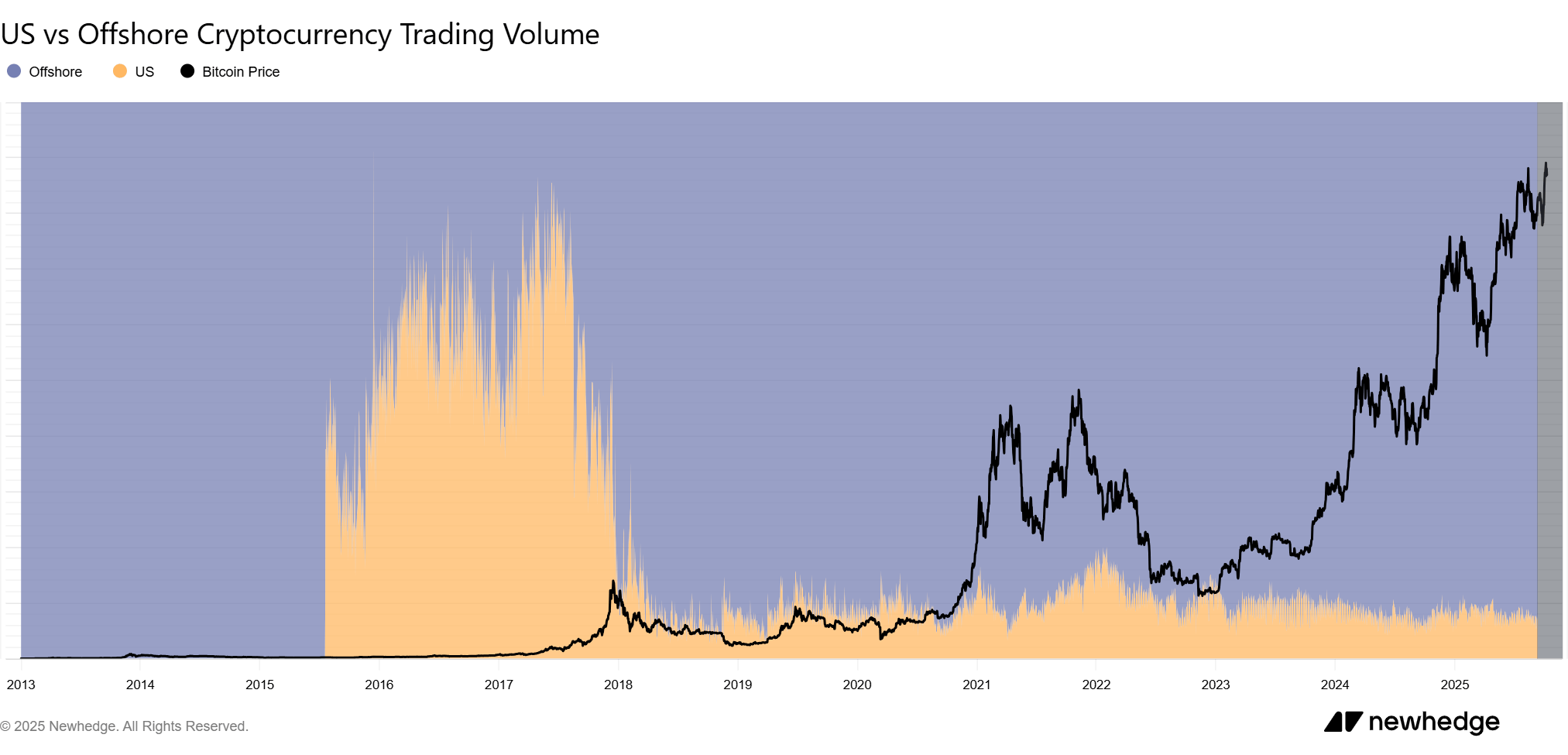

To grasp the potential consequences, one must examine the present situation, in which a small proportion of total worldwide trade volume takes place on platforms operating in the U.S.

Newhedge

data

reveals that current U.S.-based crypto trading platforms account for less than 10% of worldwide trading activity, while the top eight platforms, largely located outside the U.S., account for roughly 90% of overall market liquidity.

These data points suggest that liquidity tends to concentrate on platforms where regulatory restrictions are less stringent. Mandated compliance at the protocol level, as suggested by the Senate proposal, could hasten the movement of liquidity.

If users in the United States are required to engage exclusively via KYC-verified interfaces, or if the Treasury possesses the capability to restrict accessibility to certain protocols, traders seeking anonymity, adaptability, and lower transaction costs may choose bridges or international exchanges where restrictions are either less stringent or not enforced.

Over time, this shift could reinforce the status of offshore platforms as liquidity hubs, bolster the dominance of established exchanges outside the United States, and result in fragmented trading activity across multiple jurisdictions.

Simultaneously, reduced trading activity, wider bid-ask spreads, and less liquidity could cause a reduction in the size of liquidity pools in the U.S. This fragmentation might stifle innovation, exacerbate inefficiencies in the market, and undermine the competitive advantages of the U.S. within the global cryptocurrency ecosystem.

Additionally, enacting these regulations could affect how American cryptocurrency users connect with the expanding DeFi market.

A recent report by DeFi Funds

suggested

that a number of individuals in the U.S. are skeptical of the established financial system.

Consequently, the DeFi industry has generated their interest as they believe it provides improvements over the current system, like authority over their money and decreased transaction fees.

Industry backlash

Due to the bill’s potential significant market impact, industry experts have voiced opposition to it.

Jake Chervinsky, chief legal officer for Variant Fund,

stated

:

“Numerous aspects of the plan are inherently unworkable and fundamentally flawed. It is not a ‘first offer’ to commence negotiations, but a list of demands seemingly aimed at killing the bill.”

Chervinsky also argued this was an “unprecedented government appropriation of an entire market, with potential violations of constitutional principles.” He added:

“It’s not just anti-crypto; it is anti-innovation and establishes a hazardous framework for the entire technical industry.”

Zack Shapiro, head of policy at the Bitcoin Policy Institute, agreed, highlighting that the legislation “broadens illicit-finance legislation to include software and software developers rather than illegal conduct.”

He believes this establishes a worrying precedence for censoring legitimate private exchanges, analogous to government

targeting

of Tornado Cash and Samourai Wallet developers.

Brian Armstrong, CEO of Coinbase,

said

the bill “would impede innovation for years” and block America from becoming a leader in crypto finance.

He mentioned:

“We categorically refuse to accept this. It is a poorly conceived strategy that would inhibit progress and keep the U.S. from becoming the global hub for digital assets.”

Hayden Adams, founder of Uniswap, stated that the legislation “would destroy DeFi” within the United States.

He, therefore, wants a “significant change from Democratic senators” to maintain progress on market-structure reform.