Ethena’s USDe, a synthetic dollar alternative, experienced a significant market capitalization drop exceeding $2 billion following a momentary detachment from its intended dollar value on the Binance exchange. This brief instability highlighted potential vulnerabilities within the cryptocurrency stablecoin ecosystem.

Data sourced by CryptoSlate reveals that USDe’s market capitalization decreased from $14.8 billion on October 10th to $12.6 billion by October 12th.

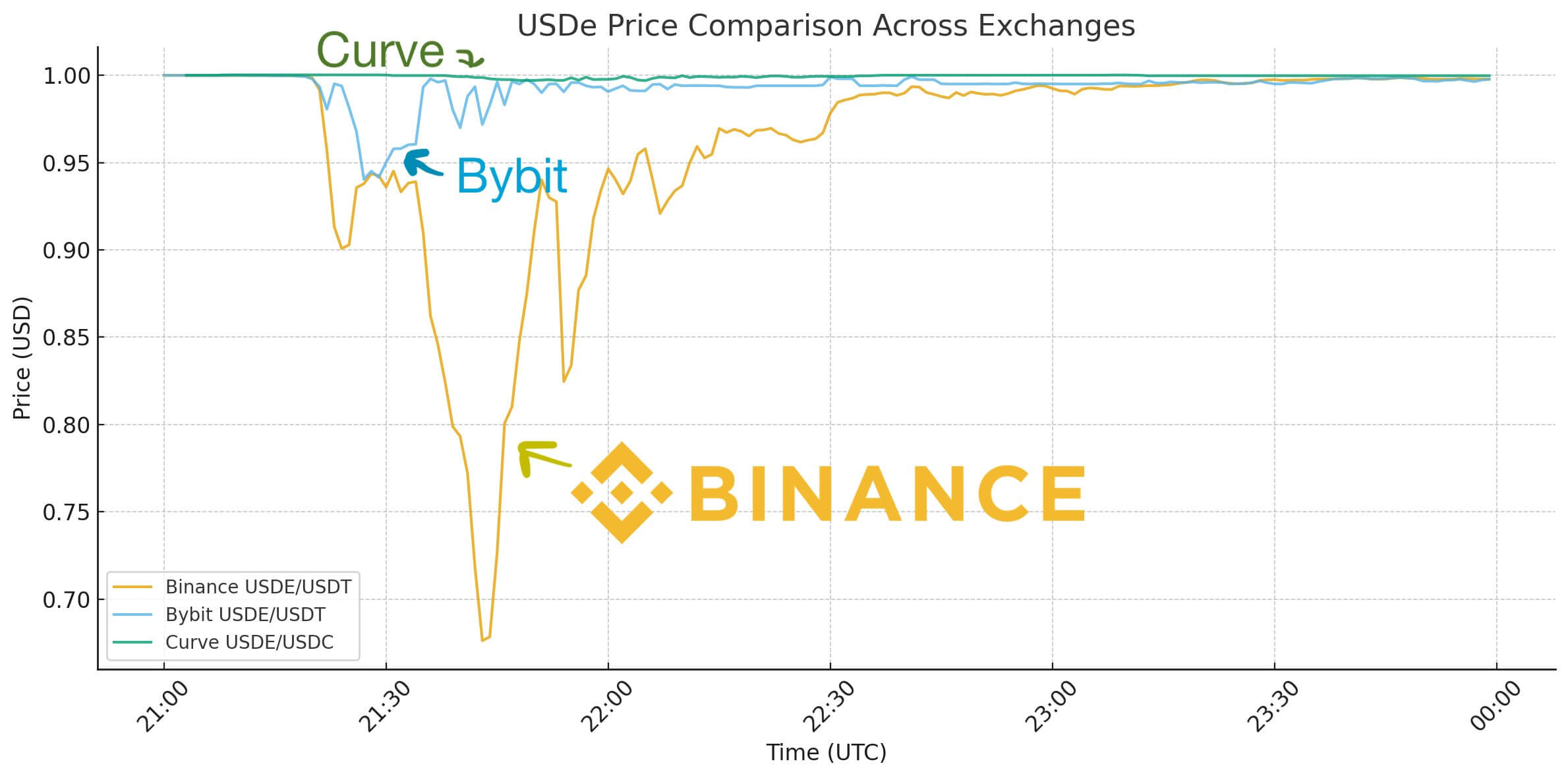

This decline coincided with a pricing anomaly on Binance that also affected wrapped tokens like wBETH and BNSOL, temporarily disrupting their association with their underlying assets.

USDe’s value briefly plunged to $0.65 before recovering back to its intended parity. Binance subsequently announced that they had compensated users with over $283 million for losses stemming from the incident.

Analyzing the Price Instability

The temporary price deviation of USDe happened during a period characterized by significant liquidations within the cryptocurrency market.

Digital asset markets experienced a sharp downturn after US President Donald Trump proposed a 100% tariff on goods imported from China, resulting in the elimination of over $20 billion in open interest across various digital assets. This caused a shift towards safer investments like gold, reducing risk appetite and exposing vulnerabilities in leveraged cryptocurrency positions.

USDe’s operational structure relies on a basis trading strategy, involving short positions in perpetual futures alongside long positions in spot markets through reserves held in USDT and USDC. Reduced funding rates can decrease returns from this strategy, potentially leading to increased redemption pressures within the system.

Despite this, the Ethena project maintains that the pricing anomaly was isolated to Binance and not indicative of a broader systemic issue.

Haseeb Qureshi from Dragonfly pointed out that USDe did not experience a uniform detachment from its peg across all exchanges, stating:

“While USDe’s price fluctuated on various centralized exchanges (CEXs), the degree of fluctuation varied. Bybit briefly saw a dip to $0.95 before quickly recovering, while Binance experienced a much more significant deviation and a prolonged recovery period. Curve, on the other hand, only saw a minor 0.3% dip.”

Furthermore, Guy Young, the founder of Ethena Labs, verified that minting and redemption processes remained functional throughout the event, handling $2 billion in redemptions within a 24-hour period.

Young also highlighted that major on-chain liquidity pools, including Curve, Uniswap, and Fluid, demonstrated minimal price deviations, with $9 billion in collateral (predominantly USDT and USDC) available for immediate redemption.

Based on these observations, Young stated:

“It’s inaccurate to portray this as a widespread USDe depeg when only one exchange experienced a price anomaly, while the most liquid pools showed no significant abnormal price movements.”

Implications for Bitcoin and the Wider Market

While USDe isn’t positioned as a conventional stablecoin, its growing integration within the crypto-financial system suggests that even minor pricing discrepancies can have cascading effects.

The recent disruption demonstrated how an issue localized to one venue can propagate through the broader market, leading to tangible losses.

Because USDe is now incorporated into several DeFi protocols and centralized exchanges, even a temporary divergence between its market value and the US dollar can impact other liquidity pools.

Such disruptions can potentially trigger forced liquidations in lending platforms, reduce liquidity in BTC and ETH trading pairs, and skew the reference prices utilized across decentralized applications.

Given these factors, Star Xu, founder of OKX, emphasized the importance of recognizing that USDe represents a tokenized hedge fund, rather than a simple “1:1 pegged stablecoin.”

According to Xu:

“These types of funds generally employ lower-risk strategies like delta-neutral basis trading or money-market investments, yet they still carry inherent risks, including auto-deleveraging (ADL) events, exchange-related problems, and custodial security breaches.”

Xu suggested that platforms using USDe as collateral need to employ adaptive risk management strategies instead of treating it as a conventional stablecoin. He argued that overlooking the asset’s structural nuances could expose the broader crypto ecosystem to systemic risks, transforming a localized incident into a wider crisis.