Since the early days of Bitcoin’s trading history, the “kimchi premium” in South Korea has served as a closely watched indicator.

When Bitcoin prices rise faster in South Korean exchanges compared to those in the United States, many observers interpret this as increased retail interest, restricted capital flow within Korea, and a general shift of liquidity towards East Asia.

Conversely, when this price difference shrinks, the interpretation shifts: global interest diminishes, arbitrage opportunities decrease, and market sentiment becomes negative. Despite periodic claims of its irrelevance, the premium consistently reappears.

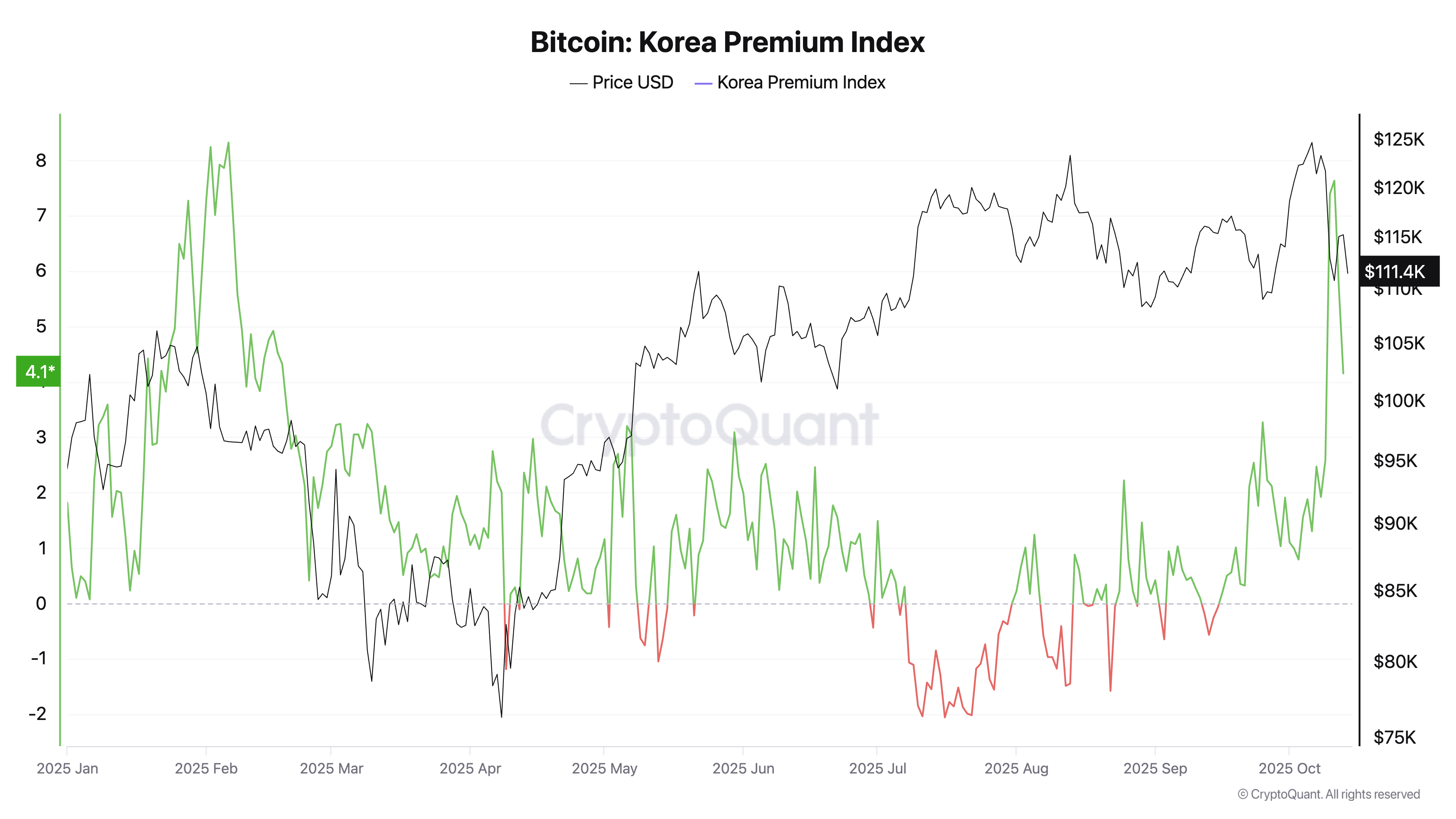

Currently, the kimchi premium, reflecting the difference in Bitcoin’s price between US and South Korean exchanges, has risen to around 4%, even as the overall Bitcoin price has declined approximately 5% over the past week.

This divergence prompts a recurring question: Does this price gap continue to predict Bitcoin’s movements, or is it merely random fluctuations magnified by market volatility?

The concise answer: it’s a tendency, not an absolute rule.

Data suggests that directional changes in the premium, specifically when Korean Bitcoin prices transition from trading at a discount to a premium or vice versa, tend to coincide with market turning points. However, the premium’s magnitude alone is not a reliable predictor.

After fluctuating between $110,000 and $120,000 throughout the summer and eventually surpassing its previous all-time high of $125,000, Bitcoin’s volatility surged last Friday due to concerns about potential tariffs impacting global markets. Bitcoin ETF trading volumes nearly hit $10 billion on Friday, coinciding with a 5% decline in Bitcoin’s price over the week.

Throughout these events, Korean exchanges began to command higher prices once more. The kimchi premium increased by 1.7 percentage points, while Coinbase’s premium remained relatively unchanged, hovering around a minimal 0.09%.

A common occurrence is a spike in the kimchi premium while the US premium on Coinbase stays stable. In 2021, considerable retail investment in Korea pushed premiums beyond 15%.

In 2018, the same metric went negative as local traders rapidly sold their holdings. The interesting element in 2025 is the timing: premiums are increasing amidst a drop, instead of following a rise. Historically, this pattern often signals upcoming price recoveries.

An examination of 2025 data shows that crossing points of the kimchi premium – the points when the premium switches from negative to positive – were historically succeeded by an average return of +1.7% after a week, and +6.2% after a month, with success rates of 67% and 70% correspondingly.

The link between the level of the premium and future returns is slightly inverse, approximately −0.06. This implies that a high premium itself doesn’t promise an upward movement.

The critical factor is the transition in capital flow direction. Conversely, Coinbase’s premium doesn’t present a similar signal. Its shifts typically lead to stable returns, with success rates around a weaker 55%. The difference underlines the varying characteristics of both markets.

South Korea’s regulations on capital, and limited ease of arbitrage, turn its local premium into a measure of limited purchasing pressure. The spread on Coinbase, narrow and institutionally-driven, shows friction in the market flow, rather than general buying trends.

This is because moving KRW in and out of Korean markets is challenging. When local traders are aggressive, the prices in Korea rise faster than arbitrageurs can level out. This discrepancy presents as a premium.

When sentiment turns negative, the reverse occurs.

The premium’s zero point (where prices in Seoul are equal to those in the US) is the brief instance that this imbalance is resolved. This is a pivotal change for traders. In effect, the kimchi premium acts as a gauge of sentiment, affected by regulatory restraints. It lags in global flows when capital is trapped, before excessively adjusting once liquidity follows. Its value is not in predicting Bitcoin’s movement; rather in identifying who is still buying when most are hesitant.

Last week’s decline fits this trend. Global institutions were reducing their exposure due to tariff worries, while Korean exchanges were still registering positive inflows. The premium widened while prices declined: a minor, but indicative separation.

Whether this pattern leads to a relief rally is contingent not just on South Korean movements but how quickly US traders regain spot exposure once macroeconomic issues calm. However, considering that the spot market is dwarfed by derivatives, it may take more than a change in sentiment to achieve significant volumes.

The figures also show that the effect of these differences reduces as the market develops. As arbitrage becomes easier and institutions engage, spreads between regions lose their significance.

At 4%, the kimchi premium is not indicative of a retail bubble. It is 1.35 standard deviations higher than its 2025 average, but within a common range of regional differences. This suggests that Korean traders are embracing volatility instead of retreating from it.

Local trends can still matter marginally even as the market becomes desensitized to large ETF movements.

So, does the kimchi premium anticipate Bitcoin movements?

In some instances, yes, but only when there is a definite directional move.

The change is the signal; not the level. Presently, South Korea is paying a premium while the rest of the world is doubtful. How this gap disappears – through a rally or exhaustion – will illustrate Bitcoin’s underlying volatility.