The recent weekend saw significant price fluctuations for

Bitcoin, driven by broader economic factors. On Friday, escalating trade tensions with China sparked a sell-off in riskier assets, causing Bitcoin to dip below $110,000. This sharp decline triggered the

liquidation of approximately $7 billion in leveraged cryptocurrency positions due to rapid unwinding in a market with limited liquidity.

However, market sentiment improved from Sunday evening into Monday. A more reassuring statement from Trump regarding relations with China helped stabilize US markets, leading to a recovery in Chinese ADRs. Bitcoin mirrored this positive shift, experiencing a morning surge that partially offset the previous losses.

A key question arising from this weekend’s turbulent trading is whether the US spot ETF market, particularly

BlackRock’s IBIT, played a role in mitigating the severity of

Bitcoin’s price drop. Did these ETFs act as a buffer, preventing a more substantial decline?

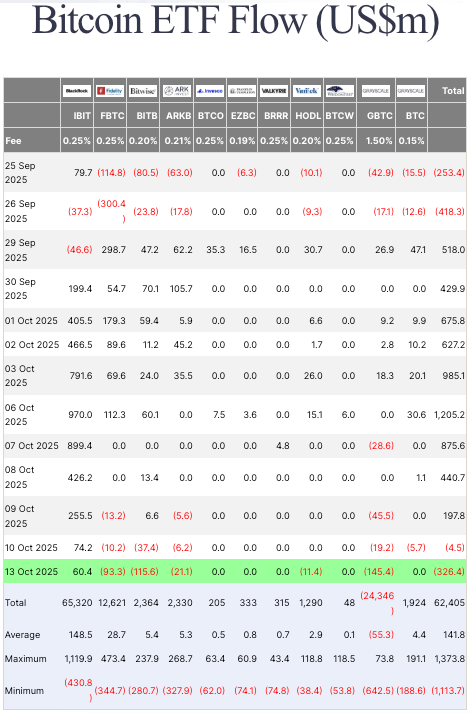

Examining the creation and redemption activity of these ETFs offers valuable insight. The early part of the preceding week witnessed an unprecedented surge in US spot Bitcoin ETF activity, with net inflows reaching approximately $1.21 billion on Oct. 6 alone – the largest single-day influx in several months.

This significant influx of capital occurred before the emergence of negative trade headlines, suggesting a pre-existing demand for Bitcoin exposure through these investment vehicles. Even when considering potentially inflated figures from some aggregators, the underlying trend remained consistent: a considerable amount of capital flowed into these ETFs in the days leading up to the macro shock.

Subsequently, the market experienced a downturn. If ETFs were inherently unstable, a wave of immediate redemptions on Friday would have been anticipated. However, this did not materialize. Data compiled by Farside indicates that aggregate US spot Bitcoin ETF flows for Friday, Oct. 10, resulted in a mere $4.5 million in net outflows.

Farside)

However, delving deeper reveals that

IBIT attracted $74.2 million in inflows, while the majority of its competitors experienced outflows. This divergence is significant because it demonstrates that the ETF market did not react uniformly to the market stress. While some investors sought to redeem their holdings, the largest fund continued to accumulate shares and custody Bitcoin. During a period characterized by forced selling and limited spot market depth, a consistent source of demand can effectively moderate the impact of a potential market collapse.

This difference became even more pronounced on Monday, Oct. 13. Data reveals a larger overall outflow of $326.4 million. Once again, IBIT distinguished itself as a net buyer, adding $60.4 million. Correlating this activity with price movements provides a clearer picture: the market recovery was not driven by widespread ETF buying.

Instead, the market stabilized due to the continuous accumulation of Bitcoin by the largest ETF, even as others experienced outflows. While IBIT is not necessarily a guaranteed price floor, it explains why the weekend’s sell-off failed to trigger a rapid decline below $100,000 once market sentiment improved.

To understand these trends, it’s crucial to consider the influx of capital into spot ETFs between Oct. 6 and 8. During this period, these ETFs absorbed hundreds of millions of dollars daily, including a record-breaking intake exceeding $1.2 billion.

These inflows translated into new Bitcoin holdings for custodians, providing these ETFs with a buffer of shares heading into the sell-off. When the market experienced volatility, investors in these ETFs were not quick to redeem their holdings, and IBIT, the fund with the most robust primary market activity, continued to attract investment.

From a structural perspective, ETF redemptions do not immediately result in selling pressure on exchanges. Authorized participants (APs) manage the process by exchanging baskets of assets and hedging exposure through futures and spot markets.

On Oct. 10, the relatively small net outflow across all ETFs likely exerted some short-term selling pressure as APs rebalanced their books. However, IBIT’s inflows worked in the opposite direction. The resulting effect was a neutral market position rather than unilateral hedging, contributing to Bitcoin’s stabilization once broader market sentiment improved.

Key Takeaways

Several conclusions can be drawn from this analysis:

First, the investor base is clearly segmented. ETF holders do not behave uniformly during market downturns. On both Oct. 10 and 13, IBIT experienced net inflows while its competitors recorded redemptions. This suggests a holder mix that is more tolerant of drawdowns within the largest, lowest-fee ETF, while smaller funds experience more rapid turnover.

From a price perspective, the primary market’s net effect is the most important factor. On the most challenging day, the cohort’s net outflow was insignificant and partially offset by IBIT’s accumulation.

Second, pre-downturn inflows influenced the starting point. The surge in early October meant that custodians already held newly created shares heading into Friday.

This provides stability. Holders must choose to redeem their shares to translate market stress into primary market selling. Data suggests that many did not, and when redemptions did occur, IBIT’s inflows mitigated the impact.

Third, derivatives continued to play a significant role. The $7 billion liquidation was driven by forced position closures, not ETF-related panic.

The ETF data provides additional context: a small net outflow on Friday, a larger net outflow on Monday, and a consistent inflow into IBIT.

This pattern helps to explain why Bitcoin did not experience a catastrophic collapse below $100,000 when the macro shock occurred, and why the market had the potential to rebound once the policy environment improved.