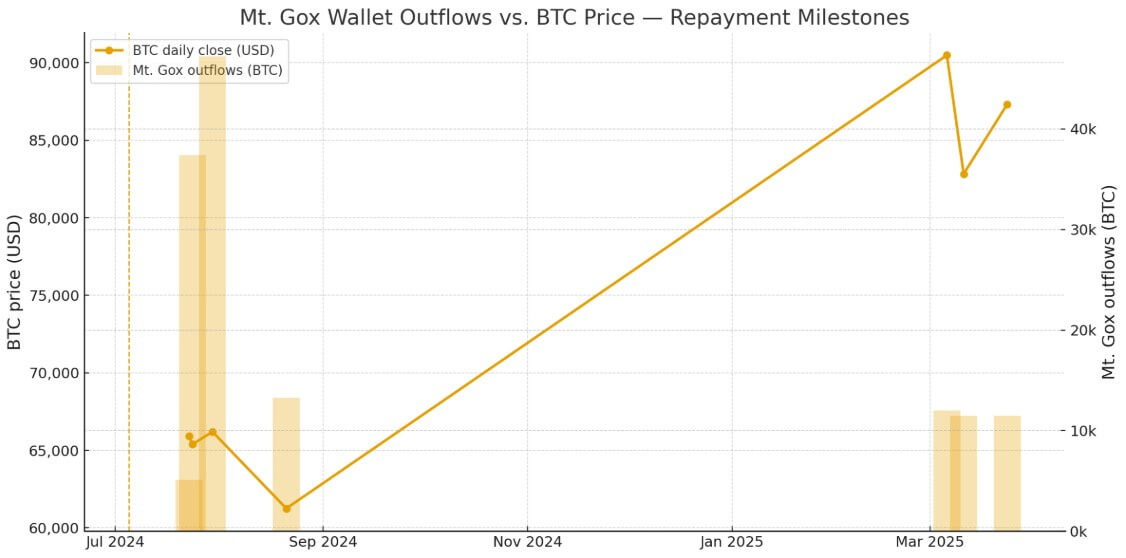

The trustees managing the Mt. Gox bankruptcy estate are working towards an October 31st deadline for completing initial repayments in Bitcoin (BTC) to creditors, specifically the Base, Early Lump-Sum, and Intermediate payouts. Approximately 34,689 BTC remain in wallets associated with Mt. Gox as the final date approaches.

After facing hurdles such as processing delays and incomplete documentation, which initially held up distributions that began in July 2024, the Tokyo District Court granted a one-year extension to the original October 31, 2024, deadline.

The appointed trustee facilitates the distribution of Bitcoin and Bitcoin Cash via recognized cryptocurrency exchanges, including Bitstamp and Kraken. Creditors who did not opt to receive cryptocurrency are being compensated in cash.

It’s important to note that October 31st signifies the final date for completion of these repayment phases, not a single, unified payout event. The trustee has indicated that these phases are “largely completed” for those creditors who have furnished all the necessary documentation.

This situation raises questions about the potential impact on cryptocurrency exchanges: Will they be able to absorb a possible surge in supply towards the end of the month, or will creditors choose alternative routes such as custody solutions or over-the-counter (OTC) trading?

| Stage | What it does | Prerequisites / trigger | Asset form & route | Timing window | Other mechanics |

|---|---|---|---|---|---|

| Base Repayment | Serves as the primary mandatory distribution tier; covers Small-Sum claims up to ¥200,000; safeguards fiat currency claims; and reduces the remaining balance after the Base Repayment. | Requires court confirmation; completion of creditor KYC/portal processes; and a signed Agency Receipt Agreement with the designated exchange or custodian. | Payouts are made in JPY via bank or transfer service, and in BTC/BCH through designated exchanges or BitGo, depending on the creditor’s preference. | Cryptocurrency distributions began on July 5, 2024, and are scheduled to conclude by October 31, 2025 (JST). | Can be processed concurrently with the Early Lump-Sum option but must precede the Intermediate repayment. |

| Early Lump-Sum | This is an optional payment representing 21% of the remaining balance after the Base Repayment; it is irrevocable and generally replaces the Intermediate and Final repayments, although some exceptions exist for limited risk compensation. | Requires the creditor to have chosen the Early Lump-Sum option via the portal, completed all necessary verification checks, and have the trustee operationally prepared with all payment venues. | Payments are made in cash and/or BTC/BCH using the same channels as the Base Repayment. | Executed in conjunction with the Base Repayment for eligible creditors, and scheduled to conclude by October 31, 2025 (JST). | Creditors who opt for the Early Lump-Sum typically waive their right to Intermediate and Final repayments. |

| Intermediate | These are optional installment payments offered to creditors who did not choose the Early Lump-Sum option; they are distributed between the time of confirmation and the Final repayment. | Requires completion of the Base Repayment, court and operational clearance, and designation of funds by the trustee. | Payments are made in JPY and/or BTC/BCH via the established channels (banks/transfer providers, exchanges, BitGo). | May be distributed in batches until October 31, 2025 (JST). | Distributed pro-rata across all eligible claims and cannot precede the Base Repayment. |

Potential pathways

Of the original 142,000 BTC involved, it’s reported that roughly 107,000 BTC has been successfully transferred to the intended recipients.

Glassnode indicated that approximately 59,000 BTC flowed into exchanges by July 29, 2024, while BitGo was holding around 33,023 BTC in tracked wallets as of mid-August.

Subsequent distributions occurred throughout the late summer period, but the current breakdown between cryptocurrency flowing to exchanges versus custodial solutions remains undisclosed.

The ultimate arrival of the remaining 34,689 BTC to the market before the deadline hinges on three possible scenarios.

In the first scenario, distributions are staggered throughout October, allowing creditors to choose to either hold their coins or transfer them into custodial storage, thereby mitigating immediate selling pressure on the market.

Processing times at Kraken and Bitstamp can take up to 90 and 60 days respectively. This means that individual credits could be disbursed on different dates even within the same repayment phase, which spreads potential sales across several weeks instead of concentrating them.

The second scenario involves creditors opting for over-the-counter (OTC) desks to sell their cryptocurrency. This method could reduce available liquidity for institutional purchasers without significantly impacting public exchange order books.

Transactions conducted via OTC desks completely bypass standard exchange infrastructure. As a result, spot trading volumes and basis trades remain largely unaffected, even as distributions are completed before the October 31st deadline.

The third scenario anticipates unexpected inflows to exchanges as batches of cleared custodial transfers are added to the order books of Bitstamp or Kraken.

Substantial inflows of this kind would likely be evident in spot trading volumes, potentially compressing basis spreads and influencing ETF arbitrage opportunities as market makers adjust their hedging strategies.

Exchange-bound deliveries are generally easier to track than custodial or OTC transactions, making sudden wallet movements a critical signal for traders who are monitoring Mt. Gox-related addresses leading up to the month-end deadline.

What does history tell?

Of the approximately 107,000 BTC distributed so far, available data suggests that around 59,000 BTC ended up on exchanges, while about 33,000 BTC were processed through BitGo. Information on the destination of the remaining BTC is not publicly available. Based on the 92,000 BTC that were tracked, approximately 64.1% was sent to exchanges.

If this ratio were applied to the remaining Bitcoin to be distributed, the most extreme scenario would involve approximately 22,253 BTC being deposited on exchanges simultaneously. With Bitcoin trading at $106,795.03 at the time of writing, this represents a potential $2.4 billion in sell pressure.

However, the broader market decline observed around the same period last year was primarily attributed to the unwinding of the Yen carry trade, which saw BTC plummet from $58,315.08 to $49,351.27 on August 4th.

Concerning earlier Mt. Gox-related movements, Bitcoin’s price showed relative stability on July 30th, despite the transfer of 47,229 BTC across three separate wallets. At the time, this amount was equivalent to $3.1 billion.

Therefore, even if the “worst-case” scenario of $2.4 billion worth of Bitcoin were to flood exchanges, historical price movements suggest that the price impact may only be relatively minor fluctuations.