September saw US inflation rise slightly, reaching 3.0% compared to the previous year. Despite this, predictions within the financial markets still anticipate the Federal Reserve will lower interest rates in the coming week.

The Consumer Price Index (CPI) showed an increase of 3.0% annually and 0.3% monthly. Core CPI, which excludes volatile food and energy prices, remained stable at 3.0% year-over-year and 0.2% month-over-month. Gasoline prices jumped by 4.1% during the month, while housing costs (shelter inflation) maintained a level near 3.6%. The Bureau of Labor Statistics successfully released the data on schedule, ensuring Social Security cost-of-living adjustments could proceed as planned, despite recent government shutdowns.

Interest Rate Expectations Remain Largely Unchanged

The release of the inflation report had minimal impact on traders’ expectations regarding interest rates.

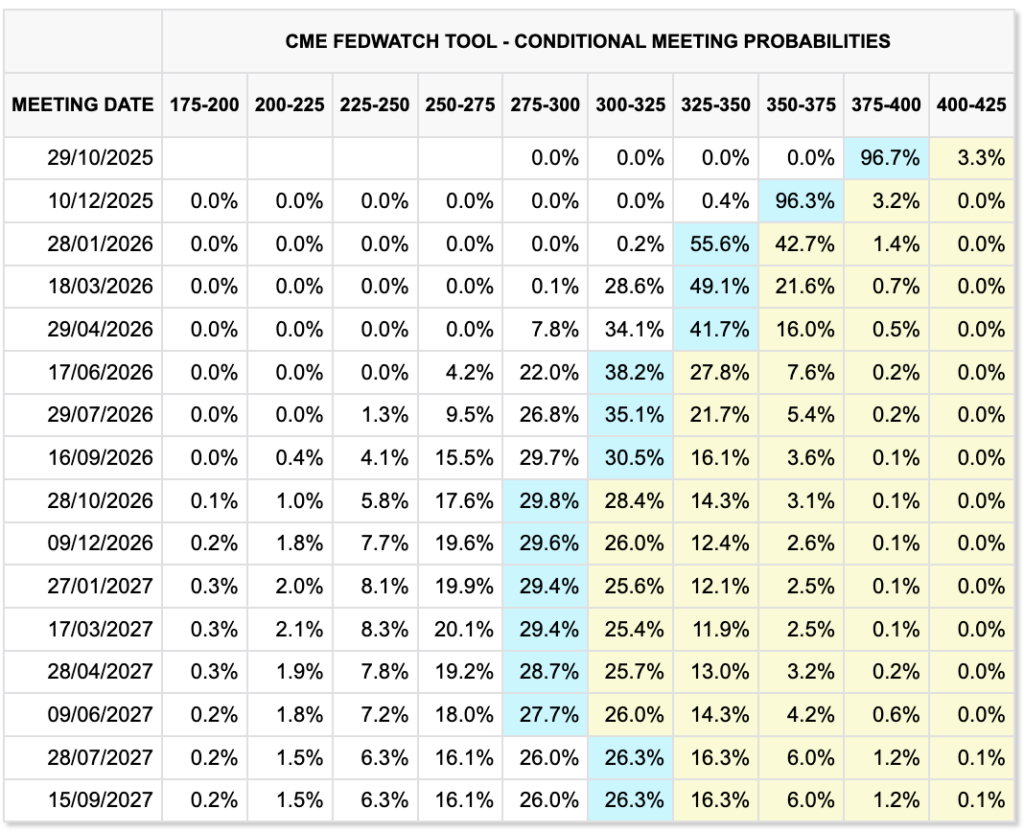

According to the CME Group’s FedWatch tool, futures contracts indicate a greater than 90% likelihood of a 0.25% (25 basis point) reduction by the Federal Open Market Committee (FOMC) at their meeting on October 29th. This move would adjust the target rate from its current range of 3.75% to 4.00% down to a new range of 3.50% to 3.75%.

Looking beyond the immediate meeting, the same FedWatch data suggests that the most probable average interest rate will be approximately 3% by this time next year.

For the FOMC meeting scheduled for October 28, 2026, the highest probabilities are concentrated in the 2.75% to 3.25% range, with slight possibilities for outcomes above or below this band.

A simplified, probability-weighted average calculation places the expected rate around 2.97%, aligning with a gradual decrease from current levels to approximately 3% over the coming year.

| Target range (%, Oct 28, 2026) | Probability |

|---|---|

| 2.50–2.75 | 17.6% |

| 2.75–3.00 | 29.8% |

| 3.00–3.25 | 28.4% |

| 3.25–3.50 | 14.3% |

| Other bins | 9.9% |

Analysis from financial institutions and model-based estimates offer further perspective. Goldman Sachs anticipates three rate cuts in 2025, followed by two additional cuts in 2026, ultimately positioning the federal funds rate within a range of 3.00% to 3.25% by the end of 2026.

The Federal Reserve Bank of Cleveland’s Simple Monetary Policy Rules dashboard indicates that median rule projections, dependent on the specific economic forecast utilized, point to rates in the high-3% range for 2026. This serves as a reminder that persistent inflationary pressures could potentially keep policy rates higher than what futures markets currently predict. The divergence between these forecasts introduces the possibility of a more hawkish (restrictive) monetary policy stance if the decline in core inflation stalls.

Yield Curve Context Influences the Impact of Easing

The yield on two-year Treasury notes has remained close to the 3.4% to 3.5% level, while the 10-year yield has hovered around 4%. Furthermore, the 30-year breakeven inflation rate is approximately 2.25%.

A survey of strategists conducted by Reuters suggests that longer-term Treasury yields will remain relatively stable around 4.1% to 4.2% over the next 6 to 12 months, as the term premium (the extra yield investors demand for holding longer-term bonds) and government debt issuance limit potential declines.

If long-term yields remain elevated while short-term yields decrease, the yield curve will steepen. This could moderate the extent to which overall financial conditions become “easier,” even with cuts to the policy interest rate.

For digital assets like Bitcoin, the connection to monetary policy is now influenced by both real yields (inflation-adjusted yields) and investment flows. According to CoinShares, global cryptocurrency exchange-traded products (ETPs) experienced a record weekly inflow of $5.95 billion in early October, coinciding with Bitcoin reaching a new high near $126,000. However, the following week saw outflows, primarily driven by Bitcoin, totaling approximately $946 million amidst increased volatility. Additionally, over $19 billion in cryptocurrency positions were liquidated following announcements by US President Donald Trump regarding new tariffs on China, which impacted overall macroeconomic expectations.

Bitcoin’s price has been consolidating in a range between $108,000 and $111,000 leading up to the release of the CPI data and the upcoming FOMC meeting. These investment flow dynamics are critical in determining how macroeconomic factors translate into price movements, given that ETF demand now accounts for a significant portion of incremental buying pressure.

In the short term, a 0.25% rate cut, coupled with cautious forward guidance from the Fed, is likely to lower short-term interest rates while the 10-year Treasury yield remains near 4%. Should the Fed’s dot plot (a chart showing individual members’ interest rate projections) and accompanying statement suggest a potential for further rate cuts in December, the easing of short-term rates would become more pronounced, and the US dollar might weaken slightly.

Conversely, if the FOMC pushes back against expectations for further easing, and short-term real rates increase, risk assets typically decline in value until new economic data prompts a reassessment of the policy outlook.

The CPI data provides the Federal Reserve with justification to maintain its current course toward a first rate cut, especially since gasoline prices were a primary driver of the monthly increase. A subsequent decline in gasoline prices during October or November would further support the narrative of gradual disinflation.

Potential Scenarios for October 2026

Looking ahead to October 2026, three distinct scenarios can be envisioned, shaping the range of outcomes implied by futures markets and policy rules.

In a base-case scenario characterized by slow and steady disinflation, where core inflation gradually declines without a significant shock to the labor market, the policy rate is expected to settle within a range of 2.75% to 3.25%, and real yields will gradually decrease as short-term rates fall.

Alternatively, in a scenario where inflation proves more persistent (sticky inflation), core inflation remains near or above 3%, prompting the Federal Reserve to adopt a more cautious stance. In this case, the federal funds rate would likely stabilize closer to 3.25% to 3.75%, resulting in a stronger dollar and intermittent tightening of financial conditions, consistent with the Cleveland Fed’s policy rule bias.

Finally, a growth-scare scenario, characterized by concerns over economic growth, would lead to more aggressive, front-loaded rate cuts, potentially pushing the policy rate down to 2.25% to 2.75%. This would likely result in a weaker dollar following an initial period of risk aversion.

Regardless of the scenario, Bitcoin’s sensitivity (beta) to real yields remains a key factor, and ETF-related investment flows will amplify price movements during periods of monetary easing.

| Path to Oct 2026 | Policy rate range | Macro markers | BTC read-through |

|---|---|---|---|

| Glide and grind disinflation | 2.75%–3.25% | Core cools gradually, 10-year near 4.0%–4.2% | Constructively bullish if real yields edge lower and ETF inflows persist |

| Sticky inflation | 3.25%–3.75% | Core near 3%+, breakevens firm | Range-bound with USD firm and higher real rates |

| Growth scare | 2.25%–2.75% | Unemployment rises, ISM below 50 | Two-step, risk-off then liquidity-driven recovery |

Global economic factors add further complexity to the picture. The European Central Bank (ECB) has paused its rate-cutting cycle following initial cuts in early 2025, and major banks do not expect further easing in 2025, which limits the potential for a euro-driven decline in the US dollar.

The Bank of England is proceeding more cautiously with its easing measures, given that UK inflation remains above its target level. In the United States, the Chicago Fed National Financial Conditions Index and the 10-year Treasury Inflation-Protected Securities (TIPS) yield remain valuable indicators for tracking Bitcoin’s sensitivity to macroeconomic factors, as tracked by FRED.

The most immediate catalyst for market movement is the FOMC decision next week. Futures markets strongly suggest that a 0.25% rate cut is already priced in, and expectations center around a policy rate of roughly 3% by October 2026.