The surge in artificial intelligence is currently acting as a significant support for the American economy, but financial analysts at Deutsche Bank suggest that its present rate of growth might not be sustainable in the long run.

A recent report issued by the German financial institution highlights the extraordinary levels of capital expenditure in the AI sector. These investments are so substantial that they are playing a crucial role in preventing a potential economic downturn in the United States.

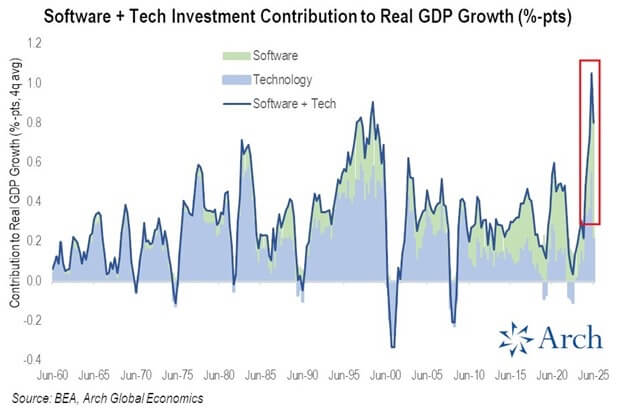

Deutsche Bank is not alone in observing the considerable influence of AI on the economic landscape. The Kobeissi Letter shared a visual representation from Arch Global Economies, illustrating that investments in software and technology have contributed over 1% to the U.S. real GDP growth – a historical first. This surpasses even the levels seen during the dot-com boom of 1998.

“This is unprecedented… The AI boom is driving economic growth.”

However, Deutsche Bank expresses concern regarding the mismatch between investment and actual productivity increases, suggesting potential challenges ahead.

Deutsche Bank Emphasizes Investment-Driven Growth Over Software Performance

The magnitude of investment is remarkable. Goldman Sachs estimates that global AI-related capital expenditure reached approximately $368 billion between early 2023 and August 2025. The majority of these funds have been allocated to tangible assets, such as constructing data centers, enhancing power infrastructure, and deploying advanced equipment.

Nevertheless, the tangible benefits derived from AI software, specifically its projected boost in productivity and efficiency, remain somewhat limited. Deutsche Bank points out that excluding technology-related expenditures, the U.S. real GDP growth is close to zero in both 2024 and 2025. This implies that the economy would already be experiencing a recession without these large investments into data centers.

The key issue is that continued contribution to GDP would require the tech cycle to increase at an accelerating rate each quarter, a pattern Deutsche Bank considers highly unlikely. Such exponential growth is not sustainable.

The present AI expansion seems more like a short burst of activity; characterized by unsustainable speed, heavily focused on initial development, and predicted to slow once the construction phase stabilizes. Considering that tech stocks have accounted for around 50% of the S&P 500’s gains in the current year, the implications are relevant not only for GDP but also for the broader financial markets.

The $800 Billion Gap

Consulting firm Bain & Co. adds further weight to these concerns. Their analysis indicates that by 2030, the AI sector would require an annual investment of $2 trillion to meet the demand for computing power. However, even when factoring in improvements in efficiency and reductions in costs, there remains an estimated $800 billion shortfall in revenue.

This deficit presents a pressing question: Who will cover the expenses? If the need for AI computing exceeds its associated revenue, the industry may face challenges related to excess capacity and declining profit margins, reminiscent of the challenges during the dot-com bubble.

On the other hand, there exists a somewhat more hopeful outlook. Goldman Sachs predicts that the benefits of AI-driven productivity will ultimately materialize, contributing approximately 0.4 percentage points annually to the U.S. GDP in the short term and around 1.5% in the long term. While it may not be exponentially explosive growth, this could provide a smoother transition compared to an abrupt AI collapse.

According to Deutsche Bank, the “balanced” view suggests that improvements in productivity are indeed on the way, but not at a pace that justifies the high level of current investment. In other words, AI has the potential to reshape the economy. However, the current timeline doesn’t match the intensity of building and investment activities underway.

Currently, AI capital expenditure is driving construction projects, encouraging investment in power infrastructure, and stimulating activity in equity markets. However, in the long run, there are concerns regarding the sustainability of this foundation, and whether the world risks creating a very expensive and unstable situation.