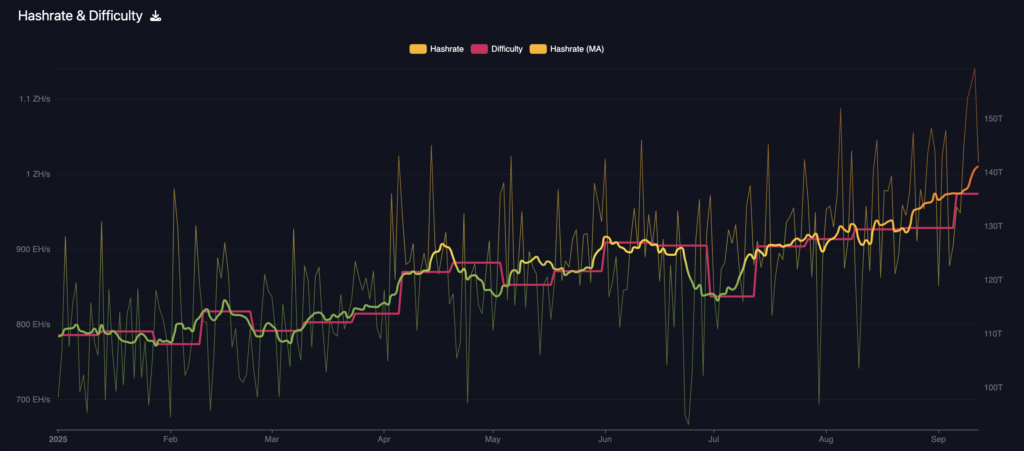

On September 4th, the Bitcoin network’s mining difficulty surged to

a staggering 136.04 trillion. Concurrently, the dollar value of Bitcoin mining hashprice experienced a slight

decline, settling at approximately $52 per petahash daily this past week. According to a report by

Hashrate Index, the most

recent adjustment marked a record high in difficulty. The forward market is currently forecasting an average

hashprice hovering around $49.17 per PH per day for the upcoming six-month period.

mempool.space)

This intensified competition has prompted Bitcoin miners to evaluate their strategies, considering options like

selling their digital asset reserves, merging operations to improve scale, or diversifying into the potentially

lucrative field of high-performance computing (HPC) that supports artificial intelligence (AI) development.

The overall production environment remains robust. The 7-day hashrate average remains near one zettahash per second.

Transaction fees only contribute a small percentage, slightly above 1%, to recent block rewards.

This combination places pressure on gross profit margins, occurring simultaneously with rising retail electricity

costs and escalating wholesale data center rental fees. According to

CBRE’s Global Data Center Trends

2025, global colocation prices were around $217.30 per kilowatt per month in Q1 of the year, with limited

availability observed in major data hub locations.

Strategic opportunities arise as computing demand redefines the energy landscape.

Earlier in the year, CoreWeave

announced its intent to acquire Core Scientific through an all-stock transaction, valuing the company at

approximately $9 billion in equity. This acquisition would unify around 1.3 gigawatts of installed capacity,

along with further potential for expansion.

CoreWeave’s deal documents highlighted potential improvements in lease efficiency and operational synergies projected

by 2027. This merger represents part of a wider AI infrastructure build-out that competes for grid access across

North America. The trajectory is apparent: AI workloads are rapidly becoming a central alternative use for power

and land formerly prioritized by proof-of-work systems.

The public markets have also experienced a shift with the introduction of

American

Bitcoin Corp. Following a merger with Gryphon Digital Mining, the company commenced trading on Nasdaq under

the ticker symbol ABTC. SEC filings reveal a controlled post-merger structure, with original American Bitcoin

stakeholders owning about 98%

of the combined entity based on fully diluted share counts.

This model prioritizes accumulation alongside internal mining operations, providing an extra mechanism for treasury

management, which could either increase or decrease market sales based on the differentials between mining costs,

spot prices, and available financing conditions.

Energy constraints and policy decisions continue to shape short-term supply behaviors.

In Texas, miners commonly reduce operations during the

Four Coincident Peak season to lower costs and qualify

for credits. This trend is reflected in Riot

Platforms’ June operational summary. Curtailments might temporarily increase hashprice and shift revenue

streams; however, they also underscore the importance of forward hedging. Luxor’s marketplace reveals an active

trading environment, with median quotes detailed on the Hashrate Forward Curve.

The breakeven math remains straightforward but exacting. The following estimates illustrate breakeven power prices in

cents per kilowatt-hour, assuming a hashprice of $53 per PH per day and common pool fees.

The inputs are based on published specifications for the

Antminer S21 and

WhatsMiner M60S, along

with incremental firmware improvements demonstrated through

LuxOS

testing.

| Efficiency band, J/TH | Example hardware | Illustrative breakeven power, c/kWh |

|---|---|---|

| ~17.5 | S21 class, stock |

~7.0–7.5 |

| ~18.5 | M60S class, stock |

~6.5–7.0 |

| ~15–16 | S21 with tuned firmware |

~8.0–8.5 |

These estimations suggest that mining operations incurring power costs exceeding single-digit rates will face

financial strain if hashprice tracks the

forward average. This is pushing firms to hedge positions on the

hashrate curve, intensify curtailment efforts during peak-priced periods, and diversify

revenue streams beyond mining.

These extended revenue opportunities include AI colocation facilities and managed GPU services, where contract rental

rates are typically quoted per megawatt per year, and power load aligns with computing demand.

Don’t Get Left Holding the Bag

Join The Crypto Investor Blueprint — 5 days of pro-level strategies to turbocharge your portfolio.

Brought to you by CryptoSlate

Recent contracts illustrate the potential revenue transformation.

TeraWulf has reported over $3.7 billion in anticipated hosting revenue based on multi-year agreements. Public

reports indicate an approximate annualized revenue rate of around $1.85 million per megawatt for the initial

phase.

The following comparison leverages these publicly available figures alongside CBRE’s benchmarks for rental rates to

demonstrate the substantial difference between established AI colocation revenue and current mining cash generation

per power unit at prevailing hashprices.

| Use of 1 MW | Representative annual revenue | Notes |

|---|---|---|

| AI colocation | ~$1.5M–$2.0M per MW | Based on announced deals and coverage in financial media |

| Bitcoin mining | ~$0.9M–$1.3M per MW | Derived from $52 per PH per day hashprice and sub-19 J/TH fleets on current averages |

This differential does not automatically necessitate that all miners should transition.

Retrofitting requires significant capital expenditure, liquid cooling infrastructure, and higher-density racks, which

might overload existing transformers. Furthermore, enforceable take-or-pay contractual obligations may limit

short-term flexibility.

However, the combination of

limited colocation supply and mergers like

CoreWeave’s acquisition, will probably keep AI hosting rents robust throughout

the remainder of the year. This is factored into treasury decisions, especially when Bitcoin’s transaction fee

contribution remains low.

Miners that can effectively monetize demand response programs, for example, the ERCOT 4CP structure, and fine-tune

their operations with efficient firmware, can broaden their breakeven thresholds without resorting to selling

cryptocurrencies.

Case studies demonstrate the range of available options. Alongside self-mining, Iris Energy is increasingly expanding

GPU capacity and cloud revenue, utilizing a dual-track strategy that buffers cash flow against hashprice volatility.

American Bitcoin presents a treasury-centric approach, blending on-balance sheet accumulation

with mining activities. Control structures and share counts are detailed in the

SEC

filing. These strategies exist alongside pure-play hosting solutions that capitalize on AI demand and

infrastructure premiums.

The immediate market question revolves around whether company balance sheets will become a primary source of supply by

year-end. Should hashprice follow the forward curve and transaction fees stay near current levels, miners facing costs

above the single-digit band will be more inclined to raise capital through cryptocurrency sales or by pre-selling

hashrate.

If AI colocation projects increase on previously announced contracts, some of the potential selling pressure could be

counterbalanced through compute reallocation and existing hedges that were set in place during the summer premium

period.

The balance of these factors will ultimately determine the quantity of miner-generated supply reaching exchanges

during the fourth quarter.