A thorough examination of popular gold-backed tokens against five key trust criteria, comparing their performance to that of Bitcoin ETFs and direct Bitcoin settlements.

Changpeng Zhao, the founder of Binance, recently voiced concerns about the true nature of tokenized gold. His comments came in response to Peter Schiff’s suggestion that digital gold could potentially surpass Bitcoin.

Stating the obvious here. Most people involved in the crypto space are already aware of this, but those outside may not yet realize the distinction.

Tokenizing gold does NOT equate to having gold “on-chain.”

It essentially means you’re trusting a third party to provide you with physical gold at some future date, regardless of changes in their management, even decades down the line, potentially during times of conflict.

It’s essentially a “trust me” type of token.

This is precisely why “gold coins” haven’t truly gained widespread traction.

– @CZ_binance

The Foundation: Understanding the Ledger

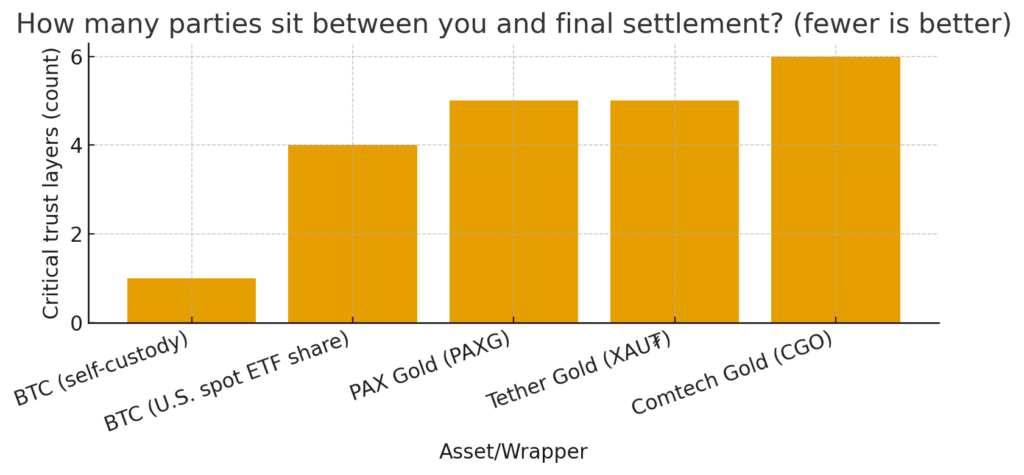

When an individual maintains direct control over their Bitcoin, the Bitcoin network provides a definitive and final settlement for the actual asset: spendable BTC.

Conversely, with a U.S. spot Bitcoin ETF, the shares are settled at the securities depository within one business day (T+1), while the Bitcoin backing the fund is settled within the custodian’s wallets on the Bitcoin network.

In the realm of tokenized gold, the blockchain verifies the token itself, but the legal ownership of the physical gold rests with the issuer, stored in their vault with associated documentation. Redeeming the gold requires the issuer, custodian, and physical logistics coordination.

The difference in redemption procedures highlights this distinction. Bitcoin can be withdrawn without permission by simply paying a transaction fee and waiting for confirmation.

In contrast, PAX Gold mandates a substantial minimum quantity, roughly 430 ounces, for direct physical redemption. Smaller amounts are processed through partners and may take several business days to complete, depending on the method used.

Tether Gold’s FAQ specifies a minimum of one London Good Delivery bar for direct redemption, subject to KYC procedures through TG Commodities, with the gold stored in Switzerland. Comtech Gold requires a minimum of one kilogram. Clearly, while token transfers are finalized on Ethereum or another Layer-1 blockchain, the actual delivery of the gold hinges on the issuer’s processes, KYC compliance, availability of gold bars, and logistical considerations.

The potential for administrative key interference introduces another point of concern. Paxos maintains control over freezing and upgrading PAXG tokens and has previously frozen addresses under the direction of U.S. law enforcement, including roughly 11,184 PAXG tokens linked to FTX in 2022.

Tether Gold and Comtech Gold also manage token contracts and redemption services according to their respective terms, meaning balances can be restricted either at the contract level or during the redemption process.

Bitcoin lacks any issuer key that could impact user UTXOs. While ETF shares can be suspended according to securities regulations, the underlying Bitcoin remains securely on-chain under the control of a qualified custodian.

Demonstrating Proof: A Complete View

Several Bitcoin ETF providers are enhancing their reserve transparency through more frequent reporting.

Bitwise utilizes daily, third-party verified proof of reserves for its spot Bitcoin ETF holdings, and ARK 21Shares actively publishes reserve data on-chain through Chainlink Proof of Reserves, powered by Coinbase.

Gold tokens typically rely on attestations from accounting firms and bar-allocation portals, rather than cryptographic proofs of vault holdings. Paxos issues monthly reports, now provided by KPMG.

Tether Gold publishes monthly reports conducted by BDO Italia, as stated in its FAQ. While these documents are helpful, they do not establish a verifiable link between the state of the vault and the public blockchain’s state at the vault’s perimeter.

A straightforward trust assessment helps to compare the settlement process, redemption mechanics, and potential for intervention across different assets.

| Asset | Settlement ledger for what you own | Redemption path | Admin-key surface | Proof cadence | Custodian / Vault |

|---|---|---|---|---|---|

| BTC, self-custody | Bitcoin L1 finality for spendable BTC | Permissionless withdrawal, network fee and confirmations | No issuer keys on L1 | N/A | User holds keys |

| BTC spot ETF shares | DTCC share ledger, T+1 settlement | Brokerage rails, APs create and redeem | Corporate actions under securities rules | Daily PoR for some issuers, Chainlink PoR feeds | Qualified crypto custodian holds BTC |

| PAX Gold (PAXG) | Ethereum token ledger for IOU, metal title off-chain | Direct bar redemption ≈ 430 oz, smaller via partners, KYC | Issuer can freeze and upgrade, prior freezes executed | Monthly KPMG attestations | Brink’s London via Paxos Trust |

| Tether Gold (XAU₮) | Ethereum token ledger for IOU, metal title off-chain | Direct 400 oz LGD bar after KYC via TG Commodities | Issuer-administered contract and redemption | Monthly BDO Italia reports | Swiss vaults, TG Commodities |

| Comtech Gold (CGO) | XDC token ledger for IOU, bar records on DMCC Tradeflow | Direct redemption minimum 1 kg | Issuer-administered contract and redemption | Attestations via DMCC processes | DMCC-approved vaults |

Point-in-time supply snapshots provide further context regarding scale and distribution. Etherscan indicates that approximately 331,000 PAXG tokens are outstanding on Ethereum as of October 23rd. Tether Gold’s Ethereum contract reflects a maximum total supply nearing 522,000 XAU₮, with additional supply across other networks. Since explorer panels can sometimes display a mix of circulating and maximum amounts, issuer attestations remain the most reliable source for determining total issuance.

The ETF landscape has seen a strengthening of the link between shares and on-chain Bitcoin. The SEC approved in-kind creations and redemptions for spot Bitcoin ETFs on July 29, 2025, allowing authorized participants to deliver or receive Bitcoin directly, instead of solely using cash, thereby reducing inefficiencies between the ETF’s share register and the underlying Bitcoin holdings.

U.S. equity markets operate on a T+1 settlement cycle for shares, which dictates intraday tracking and primary market windows for the funds, according to DMCC. BlackRock’s spot vehicle has attracted substantial asset inflows this month, with IBIT ranking among the top 20 U.S. ETFs by AUM.

Impact of Macroeconomic Conditions

Gold prices reached record intraday highs above $4,200 per ounce in October 2025, driven by safe-haven demand and policy expectations. HSBC has revised its 2025 average forecast upwards to $3,355, from $3,215, according to Reuters.

If prices surge and token holders attempt to redeem large quantities of gold, the primary constraint will likely be the redemption desk and vault logistics, rather than the blockchain itself. Minimum bar sizes, KYC processing capacity, and gold bar availability could create bottlenecks and price slippage, potentially resulting in premiums or discounts relative to the spot price during periods of high demand.

Conversely, in-kind ETF mechanisms provide Authorized Participants (APs) a direct route to exchange Bitcoin for shares, which can help the fund track its net asset value more accurately than a cash-only model, particularly when market conditions are volatile.

Risks associated with freezing or compulsory actions also differ. PAXG’s 2022 immobilization linked to FTX demonstrates that token balances can be frozen even when held in self-custodied wallets. While ETF shares can be subject to trading halts or corporate actions, the underlying Bitcoin remains securely on-chain under custodian control, rather than facing per-address freezes at the Layer-1 level.

The central observation across these examples remains consistent.

Tokenized gold utilizes public blockchains for token settlement, but final ownership of the physical gold resides in off-chain vault and custody systems governed by issuers and their partners.

Bitcoin in self-custody is settled directly on the blockchain. Bitcoin spot ETFs settle shares at the DTCC while the fund’s coin holdings are settled on Layer-1 within custodians, and several issuers now provide transparent reserve data through daily attestations or on-chain oracles.

In essence, if tokenized gold is a ticket, the blockchain records who holds the ticket, not who possesses the gold bar.