The Bitcoin price experienced a dip over the past week, but the derivatives market remained resilient, avoiding significant liquidations often seen during periods of market stress.

Looking at BTC futures, open interest expressed in Bitcoin terms saw a modest increase. The notional value mirrored the 3.36% decrease in the spot price. Additionally, options interest grew steadily during the decline, suggesting a strategy of repricing and hedging rather than forced selling.

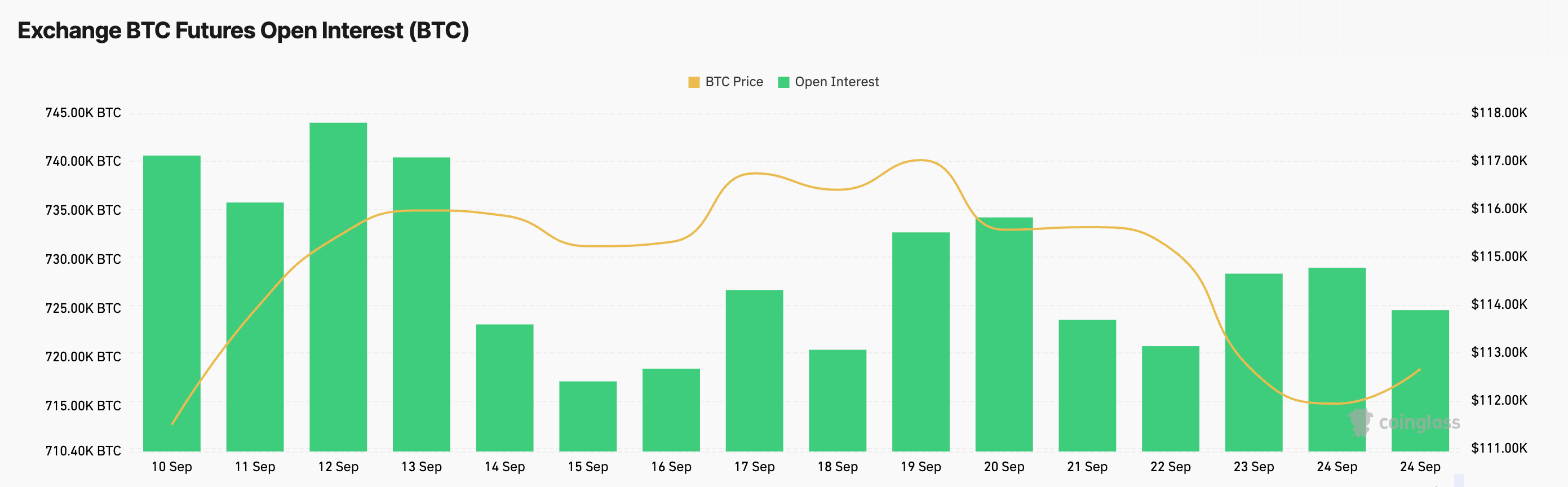

Despite a $3,910 pullback in the spot price, moving from $116,403 on September 18th to $112,493 by September 24th, futures positioning remained stable. Open interest in BTC contracts grew from 720,810 BTC to 724,990 BTC, marking a 0.58% rise.

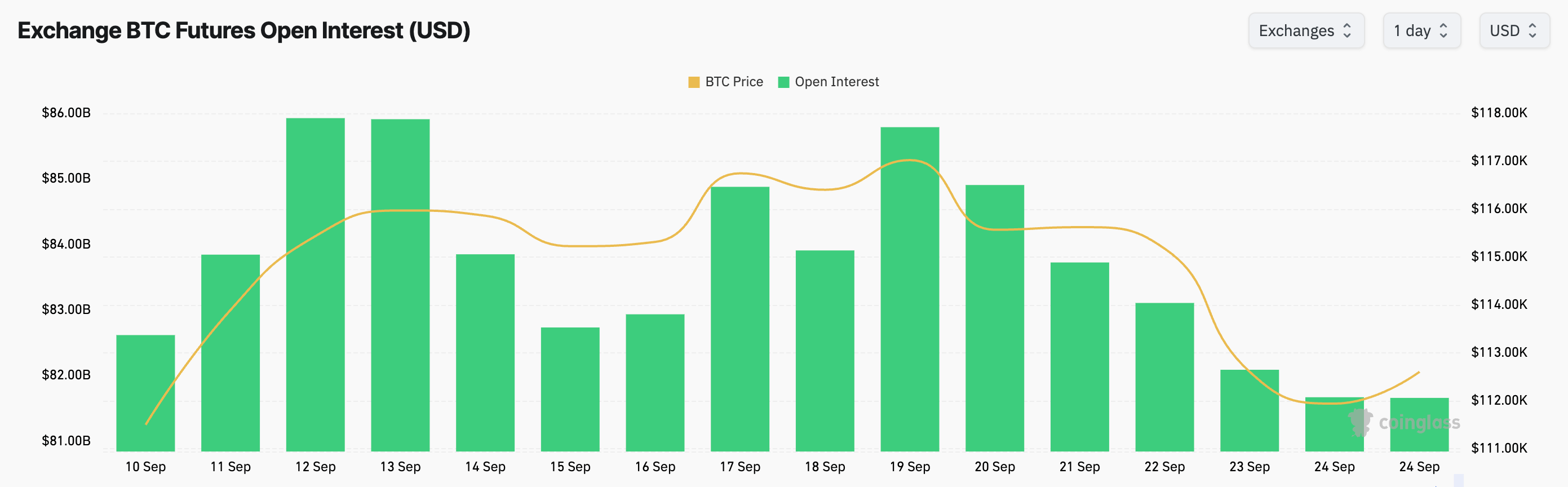

When valued in US dollars, these same positions declined from $83.91 billion to $81.58 billion, a 2.78% decrease directly influenced by the lower spot price.

Consistent Market Behavior

The dollar notional value peaked at $85.79 billion on September 19th, then slightly decreased the following day before gradually declining until the close of September 24th. The number of contract units reached a high of 734,350 BTC on September 20th and bottomed out around 720,680 BTC on September 23rd before stabilizing. This indicates that market participants were holding their positions but adjusting them to the lower price, suggesting repricing rather than a wave of forced liquidations.

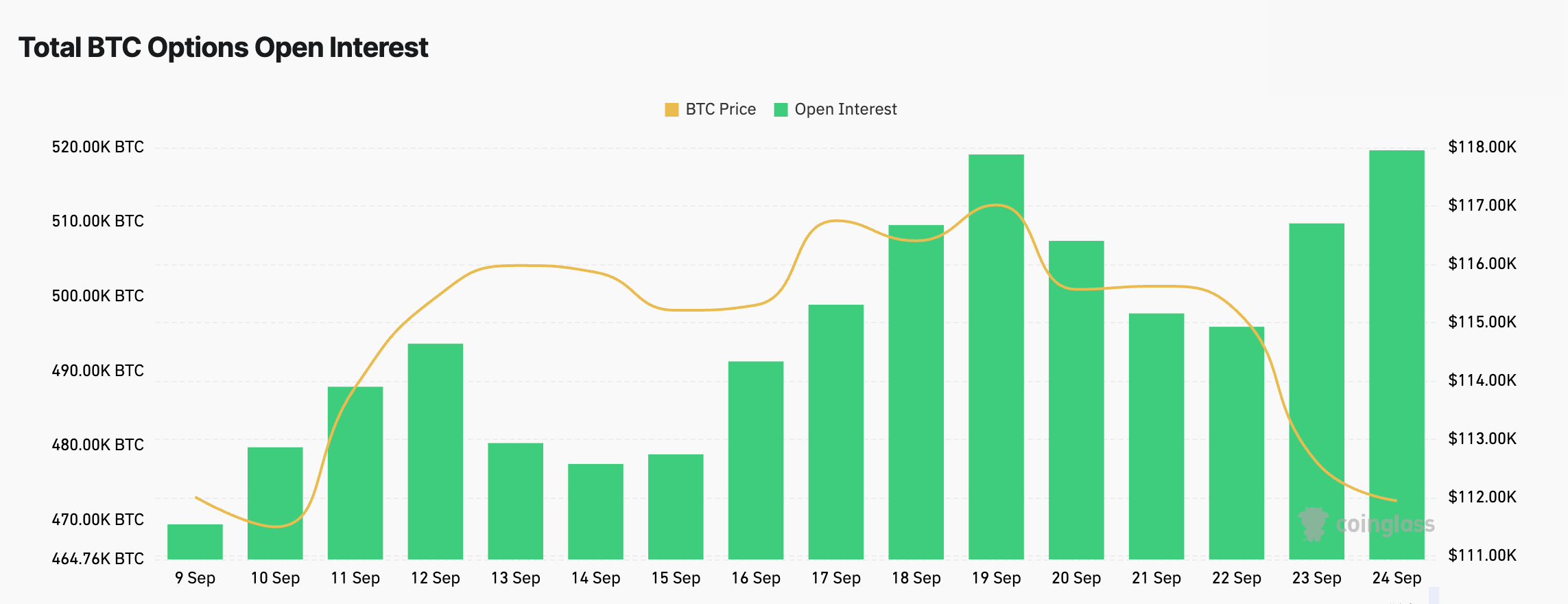

Options open interest decreased until September 22nd, reaching 495,960 BTC. Afterward, it reversed with two notable increases: +13,870 BTC on September 23rd and +9,810 BTC on September 24th. By the week’s end, total options OI stood at 519,640 BTC, up 1.97% from September 18th.

The increase in options activity coincided with the spot price dipping into the low $112,000 range. This suggests the activity was driven by hedging and structured flows, rather than speculative buying. It’s likely that dealers’ gamma exposure became more negative around September 23rd, potentially contributing to downside pressure while limiting upward momentum.

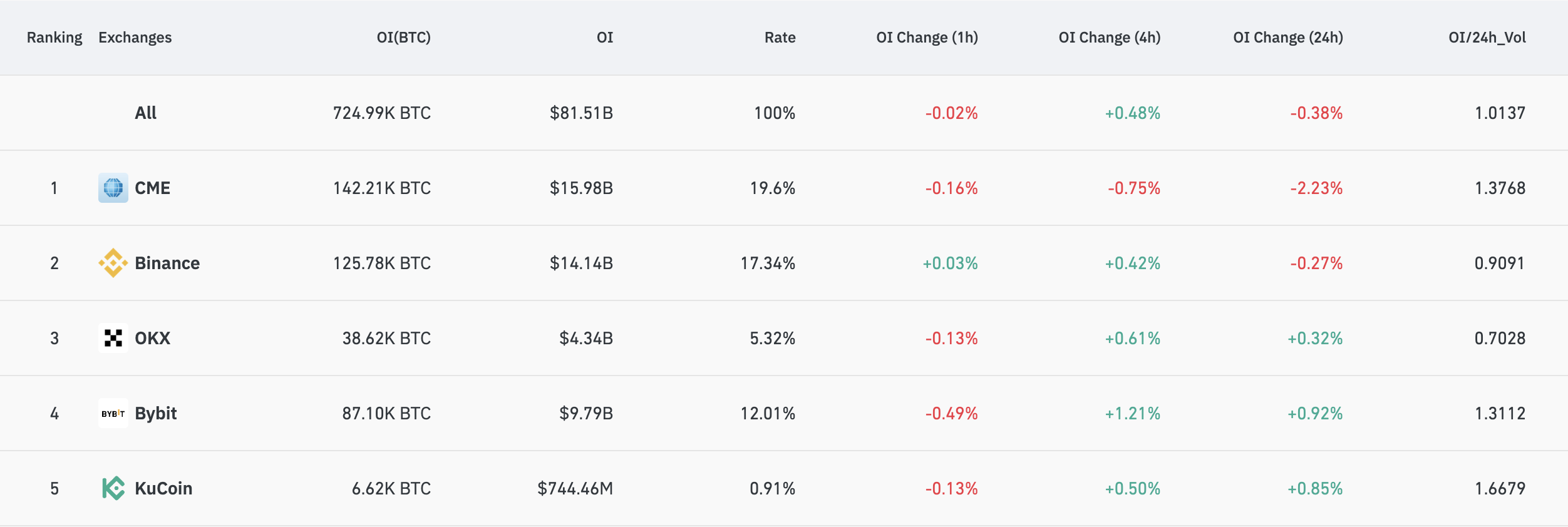

CME held 142,210 BTC of open interest, valued at $15.98 billion, experiencing a 2.23% contraction over 24 hours. Conversely, offshore exchanges showed a different trend: Bybit increased by 0.92%, OKX by 0.32%, and KuCoin by 0.85%. Binance saw a slight decrease of 0.27%.

This difference likely reflects the participant profiles on each platform: institutional investors reducing their positions on CME, while crypto-native traders maintained or modestly increased their exposure on offshore platforms.

Open interest to volume ratios further reinforced the idea of sticky positioning. CME and Bybit both registered above 1.3, and KuCoin exceeded 1.6, signifying that OI remained high relative to trading volume.

September 23rd was particularly significant. The spot price declined 2.29% to $112,604, futures notional value dropped by $1.02 billion, but BTC open interest remained relatively unchanged, and options open interest increased notably. A liquidation event driven by futures selling would have resulted in a clear decrease in BTC open interest and a more significant drop in notional value.

Instead, the data points towards stable futures positions combined with new options hedges. On September 24th, the spot price remained relatively flat, notional value decreased slightly again, and options OI continued to climb. This suggests a market that is positioned defensively, but without evidence of panic-driven selling.

Correlations across the week support this interpretation. The price and dollar-denominated futures OI moved nearly in sync, while the price and BTC OI showed little correlation.

Options OI exhibited a slight negative correlation with the spot price, reflecting hedging demand during periods of weakness. These correlations point towards a robust market structure rather than one vulnerable to disorderly liquidations.

Key Implications

Firstly, the absence of overleveraged long positions means that any stabilization in the spot price could lead to a quick expansion of notional value without the need for new positions. This increases the potential for significant recovery rallies if buying interest returns.

Secondly, because option hedges were implemented during the price decline, any upward movements might be limited until these structures expire or are adjusted. Hedging activity could therefore dampen intraday volatility, leading to a more gradual and less volatile price action.

The differences in activity across exchanges add further complexity. If CME continues to experience a decline in OI while Bybit and OKX see increases, basis and funding rates might diverge during U.S. trading hours. This presents tactical arbitrage opportunities between regulated and offshore markets, particularly during periods of uneven ETF inflows or macro-driven market movements.

Crucially, the data shows no indication of widespread panic. Futures open interest in BTC terms is holding steady, options hedges are being established, and the market appears prepared to absorb the next directional move.

As the week concludes, Bitcoin is positioned defensively but in an organized manner. The spot price is near $112,500, futures positions are stable, and options hedges are providing downside protection.

Regardless of whether the price stabilizes or continues to decline, the current positioning suggests that the market is set to react in a controlled way, rather than through abrupt, forced liquidations.

A move above the mid $113,000 range would likely trigger a rapid increase in notional value and reduce the impact of existing hedges, while a further decline would likely lead to continued building of options positions.

In either case, the market is heading into the next phase protected by hedges, rather than exposed and fragile.