Financial markets anticipate approximately 30 basis points of monetary easing at the upcoming September 17th Federal Open Market Committee (FOMC) meeting. This expectation is divided, with most forecasting a 25 basis point reduction and a smaller chance of a more aggressive 50 basis point cut.

A significant 50bps drop could potentially fuel a Bitcoin rally, possibly pushing it toward previous record highs.

Data from CME Group’s FedWatch tool, recorded on September 10th at 7:30 A.M. CT, indicated about a 90% probability of a 25 basis point cut, a roughly 10% chance of a 50 basis point cut, and almost no likelihood of no change. This implied a total cut size averaging between 27 and 29 basis points.

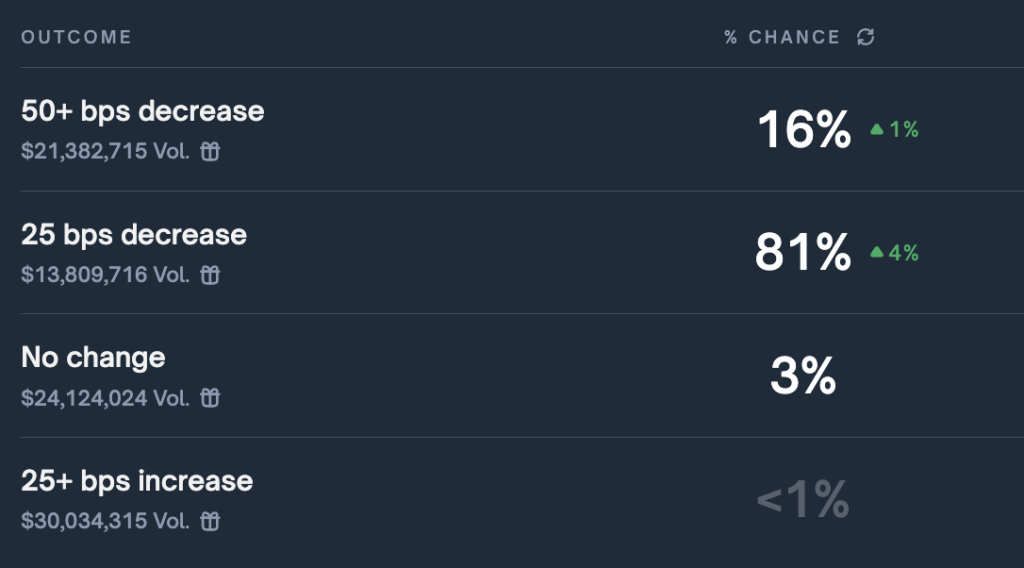

Furthermore, a Polymarket prediction contract, with $21 million at stake, suggests an even greater probability of a 50bps reduction. Predictions there are centering around an 81% likelihood of a 25bps cut, 17% for 50bps, and 3% for no change, translating to approximately 28.8 basis points of easing.

The environment influencing this key decision has significantly evolved over the preceding couple of months.

A revised benchmark from the Bureau of Labor Statistics revealed that the U.S. economy generated approximately 911,000 fewer jobs through March 2025 than initially reported. This marks the most substantial downward adjustment since 2009.

Inflation trends display inconsistency across different metrics. The core CPI, according to the BLS, rose about 3.1% year-over-year in August, while the core PCE, as per the Bureau of Economic Analysis, showed a 2.9% increase in July.

While short-term Treasury yields suggest an easing cycle, long-term yields remain supported by term premiums and fiscal factors.

A Reuters strategist survey forecasts a steeper yield curve by year-end. The two-year yield is expected to be around 3.40% in twelve months, with the ten-year yield near 4.25%, implying a two-ten spread near 85 basis points. Economists at the Cleveland Fed estimate the nominal neutral policy rate to be close to 3.7%. This means that even after a quarter or half-point rate cut, policy would still be above neutral.

Upcoming data releases before the FOMC announcement may sway the distribution. Producer Price Index (PPI) data was released at 8:30 A.M. ET today. The Consumer Price Index (CPI) is scheduled for release on Sept. 11th at 8:30 A.M. ET, and retail sales data will be available on Sept. 16th at 8:30 A.M. ET, based on official federal calendars.

The most recent PPI revealed a -0.1% change, leading to a slight increase in CME projections for a 50bps cut to 10%, although Polymarket odds decreased slightly to 16%.

These forthcoming releases can further influence the likelihood of a 25 versus 50 basis point cut, and shape the immediate reaction across various asset classes, particularly via the two-year yield and the U.S. dollar’s movements.

Potential 25bps Rate Cut in September

The most widely expected scenario is a 25 basis point cut, bringing the target range to 4.00 to 4.25 percent, coupled with a balanced Summary of Economic Projections (SEP). This is the market’s default assumption. Current forecasts generally anticipate a quarter-point reduction with two to three additional cuts in 2025, with the “dots” likely reflecting a gradual easing path into 2026 as economic growth moderates.

Historically, such a scenario has tended to produce a modest bull steepening in rate markets. This typically results in the two-year yield declining by approximately 10 to 20 basis points over a period of one to three days, the ten-year yield remaining relatively stable or decreasing by up to 10 basis points, and the dollar depreciating by around 0.3 to 0.8 percent.

Equity market performance usually hinges on the tone conveyed during the press conference, rather than solely on the official statement. Based on past FOMC meeting behavior, the S&P 500 (SPY) typically rises by roughly 0.3 to 1.2 percent if recessionary risks are not emphasized.

Don’t Get Left Holding the Bag

Join The Crypto Investor Blueprint — 5 days of pro-level strategies to turbocharge your portfolio.

Brought to you by CryptoSlate

In the cryptocurrency market, a decline in real yields and a weaker dollar generally provide short-term support for Bitcoin (BTC) and Ethereum (ETH), potentially leading to price increases of 1 to 3 percent. However, the overall path of liquidity is more significant than any single rate cut.

Scenarios: 50bps Rate Cut or a Hold

The possibility of a more aggressive 50 basis point “insurance” cut, bringing the target range to 3.75 to 4.00 percent, has gained traction following the recent BLS revisions. Standard Chartered is forecasting a 50bps cut in September after weaker labor statistics, while Bank of America anticipates two 25bps cuts in September and December.

If the FOMC accompanies a larger rate cut with communication emphasizing risk management rather than the beginning of an aggressive easing cycle, the yield curve could steepen at a faster pace. This scenario could see the two-year yield decline by approximately 25 to 40 basis points over the subsequent one to three days, the ten-year yield decreasing by 5 to 15 basis points due to persistent term premiums, and the dollar depreciating by roughly 0.8 to 1.5 percent.

Historically, equity markets have exhibited stronger initial gains in response to larger easing scenarios. Under such circumstances, the S&P 500 (SPY) could trade within a range of 0.8 to 2.0 percent, although there exists a “sell-the-news” risk if the press conference unduly emphasizes growth concerns.

Bitcoin and Ethereum would likely experience a more pronounced positive impulse from easier monetary policy and a weaker dollar, potentially resulting in gains of 2 to 5 percent. This effect could be tempered if equity markets interpret the move as a sign of growth weakness rather than a boost to liquidity.

A hawkish surprise, defined as holding rates steady while providing only guidance, is considered a low-probability outcome. The likelihood of this outcome increases if upcoming CPI and PPI data releases reveal upside surprises. In this event, the two-year yield could rise by approximately 10 to 20 basis points, the dollar could strengthen by 0.4 to 1.0 percent, the S&P 500 (SPY) could decline by 0.8 to 1.8 percent, and Bitcoin and Ethereum could fall by 2 to 5 percent as real yields increase.

Research examining predictable price movements around FOMC meetings indicates that the guidance channel exerts a significant influence on market reactions, not just the rate decision itself. Therefore, close attention should be paid to the SEP path and Chairman Powell’s description of the labor market.

Broader Market Context

Gold prices have reached record highs this week as rate cut probabilities have increased and geopolitical factors have added further support. Oil prices remain sensitive to news from the Middle East, although price movements have been contained relative to previous spikes.

Bitcoin reached a new record high near $124,000 in mid-August, driven by expectations of easier monetary policy. This makes the cryptocurrency market sensitive to the interplay of dollar direction, real yields, and language concerning economic growth in the coming week. The persistence of the term premium could limit the downside for the ten-year yield even if the two-year yield declines, thereby limiting the potential for exuberance in longer-duration assets.

The trajectory following September will be influenced by economic growth data, revisions to labor market statistics, and inflation dynamics. Market participants and forecasters generally anticipate two to three rate cuts in 2025, followed by a slower pace of easing in 2026. This aligns with the survey’s twelve-month forecasts for the two-year and ten-year yields.

If economic growth weakens, the probability shifts toward a larger front-loading of rate cuts.

If inflation accelerates, the policy discussion will likely pivot to the acceptable level of core inflation near 3 percent rather than a rapid return to 2 percent. The Cleveland Fed’s neutral rate estimate provides a useful framework: Maintaining a policy stance that remains above neutral, even after the initial rate cut, prevents a collapse in financial conditions. This factor is ultimately more important for the performance of risk assets than the first step itself.

On decision day, keep track of the “dots” for 2025 and 2026 compared to June, the language used to describe the cooling or deteriorating labor market, the initial trajectory of the two-year yield, and the initial reaction of the U.S. dollar.

These factors will determine whether the outcome is a rate cut with caveats or a more significant recalibration linked to the revised labor market picture.