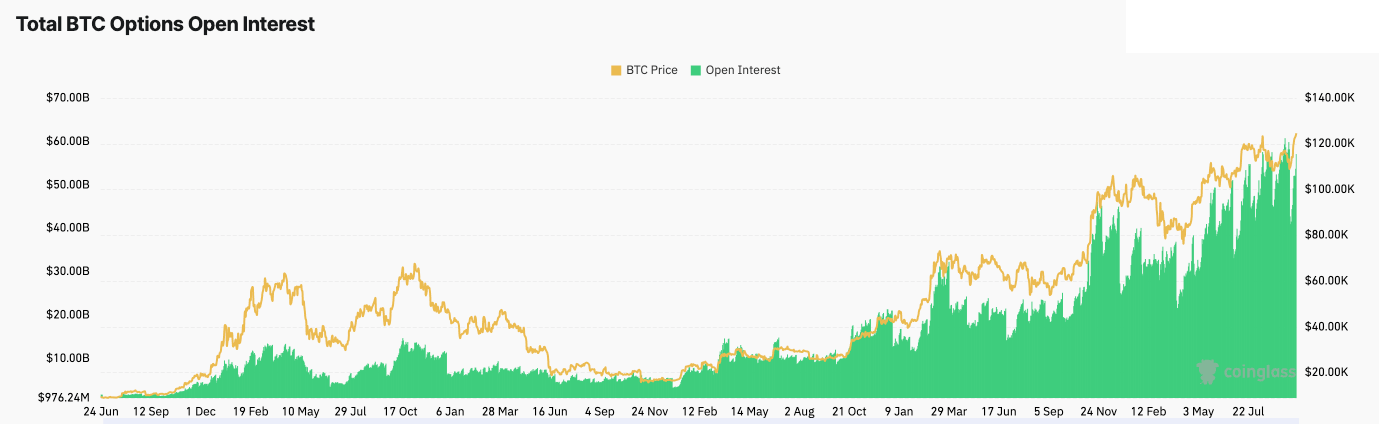

Unseen forces govern every Bitcoin price swing, whether soaring or plummeting: option traders readjusting their substantial Bitcoin holdings. With total outstanding option contracts now exceeding $57 billion, price movements are increasingly dictated by these hedging actions, overshadowing market sentiment.

Historically, Bitcoin prices were largely determined by the spot market, where retail investors and long-term holders set the pace. Derivatives, meanwhile, played a supporting role. This dynamic has shifted considerably over the past eighteen months.

The Bitcoin options market has evolved to a point where its magnitude influences the underlying asset. Data sourced from CoinGlass reveals that option open interest is now comparable to futures, rising significantly from approximately 45% of futures open interest at the start of the year to about 74% by late September.

This situation has created a self-reinforcing mechanism. As Bitcoin gains value, options dealers who have sold call options are compelled to buy Bitcoin in the spot market to maintain their hedge. Conversely, when the price declines, they sell Bitcoin to decrease their exposure.

Decoding Bitcoin’s Price Swings: Options Greeks Explained

The “Greeks,” specifically option gamma, offer a more nuanced explanation. For options contracts expiring at the end of October, gamma peaks in the $110,000 to $135,000 range, indicating significant dealer exposure near these price levels. Within this band, dealer hedging activities tend to reduce volatility; however, outside this range, these very same actions can amplify price swings.

Delta positioning shifts around the $125,000 mark, a price point that has become crucial for short-term directional movements. Vega, which measures sensitivity to volatility changes, also peaks near this level. Theta, representing the time decay of option value, reaches its lowest point. The data paints a picture of intense market exposure, with Bitcoin price seemingly balanced on a razor’s edge, where mathematical hedging calculations have more influence than underlying belief.

This represents a fundamental shift in Bitcoin’s character. Once considered a store of value or a play on digital scarcity, it now increasingly behaves like a volatility product. Implied volatility is now preceding actual realized volatility, suggesting that options markets are anticipating upcoming moves rather than simply reacting to them. When volatility spikes, the resulting demand for options drives trading volume as much as any significant news event or the Bitcoin halving.

While Deribit remains a key platform for crypto-native traders, institutional hedging activity has largely migrated to ETF-linked options, particularly BlackRock’s IBIT. Asset managers are implementing the same hedging strategies they use for traditional equities, such as selling covered calls to generate income and purchasing put options for downside protection.

Each component of these strategies necessitates hedging by dealers through CME futures or ETF creation mechanisms. This hedging process is continuous. Every incremental rise in Bitcoin’s price triggers delta adjustments, which then cascade across various liquidity pools.

The broader consequences are clear: Bitcoin’s financialization is complete. It has joined the ranks of equities and foreign exchange (FX) as a reflexive volatility-driven asset, where its price reacts more to market positioning than fundamental factors.

Increased open interest enhances liquidity and reduces volatility, while a decrease in open interest leads to diminished liquidity and amplified price fluctuations. Hedging strategies serve as liquidity infusions, whereas margin calls function similarly to quantitative tightening. The underlying framework of risk management has become the dominant factor influencing price.

Bitcoin ETFs Reinforce the Same Dynamic

During late September, US-based spot Bitcoin ETFs attracted over $1.1 billion in new capital, largely flowing into IBIT. Each ETF creation adds physical Bitcoin to the ETF’s holdings, simultaneously providing dealers with assets to hedge against short-term options.

When inflows decelerate, these hedges are unwound, withdrawing liquidity from the market and transforming gradual price declines into sharper drops. The ETF ecosystem is now an integral part of this feedback loop, where spot market activity, futures contracts, and options are intertwined within a unified liquidity framework.

Data confirms the rapid pace of this structural evolution. In 2020, the ratio of Bitcoin’s options open interest to futures open interest was approximately 30%. By early 2023, it had risen to around 37%, briefly reaching parity during the banking sector turmoil in March before surging to 74% this fall.

The trend shows a clear direction. Each price increase pulls in more participants to the hedging network, including market makers and asset managers, to the point where the derivative layer becomes inseparable from the asset itself.

Bitcoin’s Price Action Now Resembles a Complex Equation

Every price change prompts a reassessment of deltas, vegas, and margin requirements. When traders have a high gamma position (long gamma), they tend to buy during dips and sell during rallies, thereby dampening volatility. Conversely, when they have a low gamma position (short gamma), they exacerbate price movements by chasing them.

This dynamic explains why Bitcoin can experience periods of relative calm followed by sudden and unexpected surges, as the underlying flow changes from stabilizing to destabilizing. While traditional drivers like ETF inflows, macroeconomic risks, and Federal Reserve policy decisions still hold significance, their impact is now mediated through this complex mechanism. Fundamentals are interpreted and acted upon through balance sheet considerations.

The zone near $125,000 is critical. Within this range, hedging tends to stabilize volatility. A decisive break above $135,000 could trigger a rapid upward surge as dealers rush to cover their positions, while a drop below $115,000 could initiate a cascading sell-off.

These price thresholds are not based on market sentiment but represent mechanical pivot points determined by options exposure. Traders who grasp this underlying structure can anticipate potential pressure before it becomes apparent on price charts.

The derivatives era has arrived. The hundreds of billions of dollars in open interest across various derivatives markets now form the foundational framework of the modern Bitcoin market, extending beyond mere speculative froth.