The high-risk, high-reward era of using substantial borrowed funds for

Bitcoin trading is evolving into a more calculated approach.

The market, once a whirlwind of speculative activity, is showing characteristics more aligned with traditional bond markets.

Trading in options has surpassed perpetual futures contracts in popularity.

Realized price swings have narrowed, and the largest Bitcoin investment fund,

BlackRock’s

iShares Bitcoin Trust (IBIT), is now utilized more for generating consistent income

through sophisticated strategies rather than making outright directional bets.

Previously, the dominant trading strategy centered around anticipating the next major price increase for Bitcoin.

Now, the primary focus is on generating stable returns by strategically selling off Bitcoin’s price volatility.

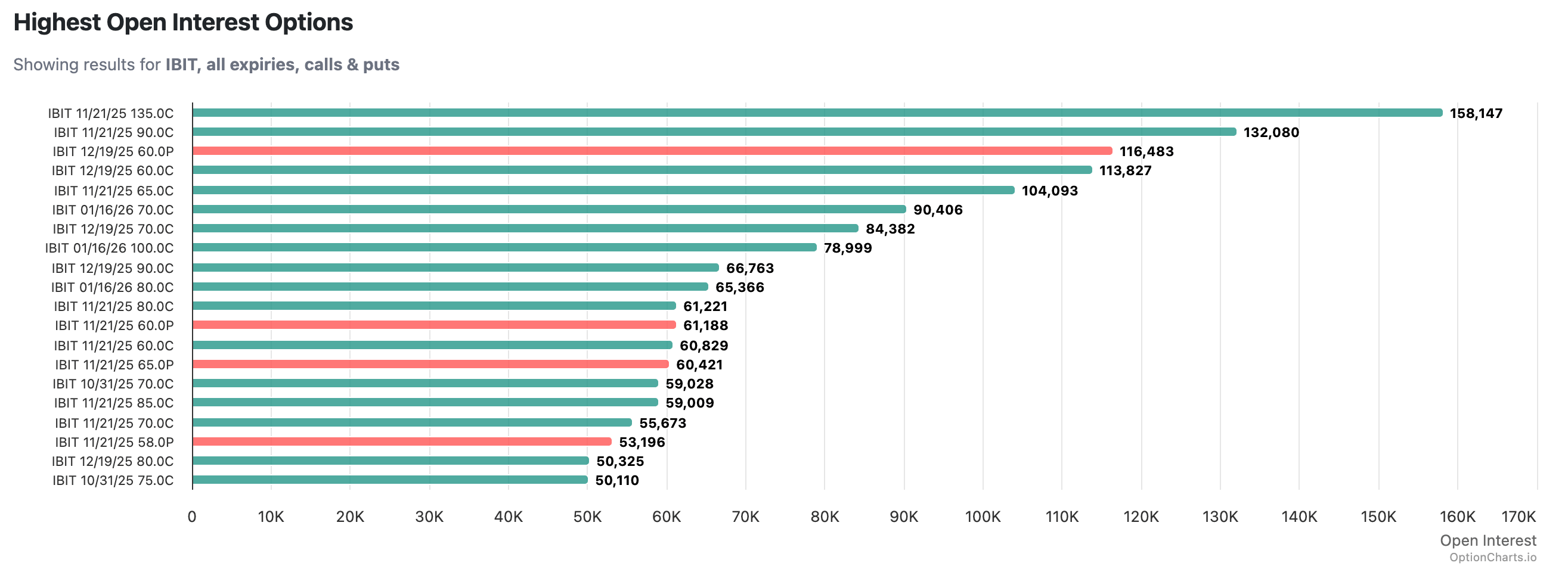

Market data indicates a fundamental shift. IBIT options currently hold an open interest of nearly seven million contracts.

This equals roughly $44 billion in potential exposure, exhibiting a put-to-call ratio of 0.40.

Buying contracts outweigh sell contracts, concentrated around target prices ranging from $65 to $75, expiring primarily in late October and November.

These contract levels are consistent with investors writing covered call options.

This approach involves simultaneously holding IBIT shares and selling short-term call options that are unlikely to be exercised to generate a premium.

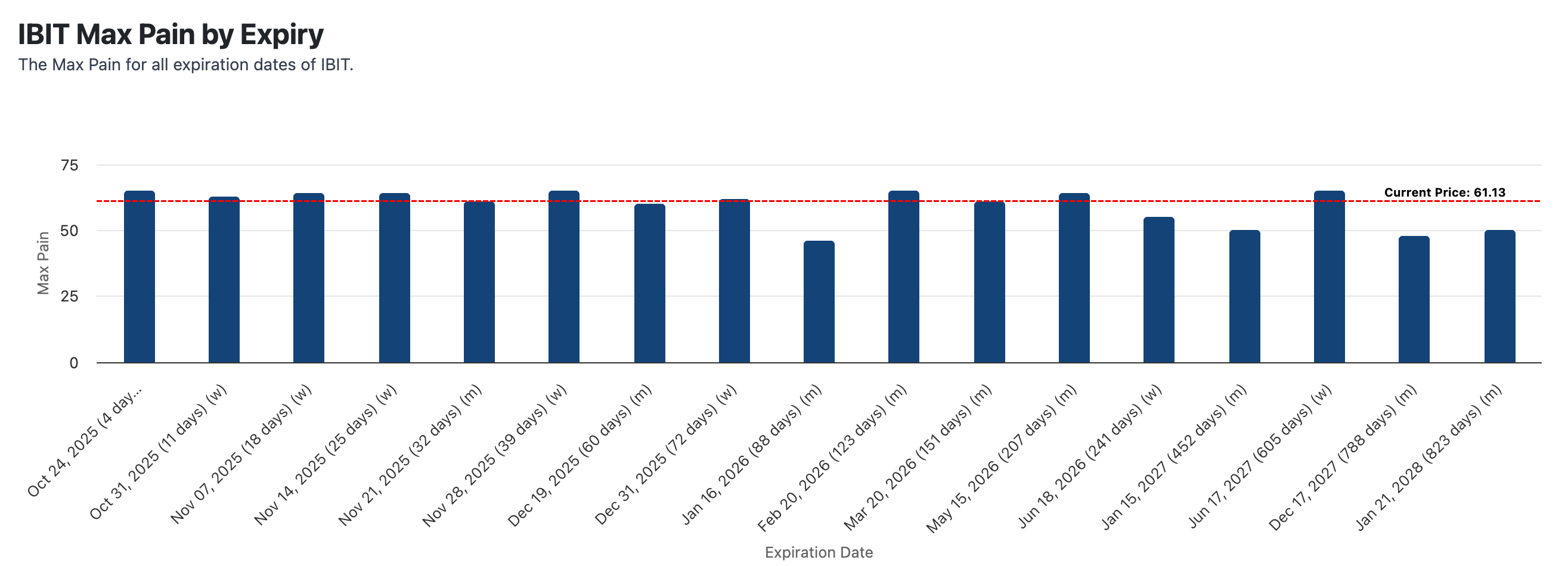

The “max pain” points, representing the price levels where option buyers would experience the most loss at expiry, are concentrated around the mid-$60 range for upcoming expirations. This aligns closely with IBIT’s current price of around $63.

The minimal difference suggests a clear strategy: to secure income in exchange for potentially limiting upside gains.

The overseas derivatives market reinforces this trend. On Deribit, a major cryptocurrency derivatives exchange, the activity in Bitcoin options is focused on out-of-the-money buying contracts set far above the current price between $120,000 and $210,000, with sell contracts grouped between $80,000 to $100,000.

While the total potential value involved reaches $46.6 billion, the actual premium at risk is $1.6 billion, implying less speculative trading.

The futures markets are reflecting this cautious attitude; across major exchanges, annualized premiums remain relatively low, significantly below the double-digit spreads seen in 2021. Profit generation through volatility sale has replaced aggressive trading.

The popular covered call strategy involves buying IBIT shares to gain Bitcoin exposure and then selling short-term call options around 10 percent above the current market value. This generates returns that can range from 12 to 20 percent annually, depending on Bitcoin’s volatility.

The outcome is a stable return stream suitable for institutions looking to participate without forecasting short-term market movements. This echoes the “basis trade” of 2020-2021, where traders bought Bitcoin and sold futures to secure arbitrage profits, with the key difference now being returns generated through option premiums.

The institutional presence is evident, concentrating their activity in maturities and levels that align with overwrite strategies frequently implemented by established entities.

These entities are running automated strategies to transforms Bitcoin into revenue streams. The capacity to use a 40 Act ETF, rather than prime brokerage has invited a class of participants who require liquidity and custody.

This trend is changing the way Bitcoin performs. The short selling of call contracts is reducing the degree of realized volatility. When the market shifts towards specified prices, dealer trading absorbs that volatility.

Breakthrough movements are slow, and market decreases are lessened. Data from the last three months indicate that the Bitcoin’s realized volatility decreased by 60 percent, in line with structural compression.

Bitcoin ETF flow data corroborates how insulated this new market has become. Throughout October, Bitcoin ETFs experienced various amounts of flows, from $1.2 billion net creations earlier in the month to a $40 million net redemption on Oct. 20.

And, the activity in IBIT options has remained persistent. As IBIT reported an outflow of $100.7 million, option volume and open interest stayed consolidated across the same expirations. This pattern shows the strategy is autonomous from day-to-day activity: a yield engine, not a bet.

In general, the Bitcoin trade works as a carrier. In prior cycles, the carrier existed in high futures financed by stablecoins. The carrier now sells volatility on an ETF.

The finances are similar: consistent income from structures. Yet, the participants and infrastructure are entirely new. For offices that did equity overwrite programs, IBIT has transformed to accommodate familiar mechanics.

The result carries implications for the market. The presence of short-selling weakens the explosivity when the price spikes. Price swings that triggered explosions now meet those looking to balance the risks.

Institutional maturity could be self-limiting because the more it becomes part of the traditional portfolio, the more tame its price action becomes. The market gains stability, but loses it trademark features.

Those who newly participate find the exchange useful. Volatility compression increases returns. Bitcoin income also appeals to those who saw BTC as out of control.

The market is systematically selling Bitcoin to earn revenue. Firms are not betting that Bitcoin will increase; they are betting that it will remain the same.

The market is domesticating; derivates are stable, funding rates are low, and options are supportive of large programs.

Bitcoin has not lost its explosive nature; a surge or ETF inflow would break the cycle, but the coin trades for returns. The casino has become a yield generator.

The market transformation is becoming more integrated to traditional finance. Volatility is an asset, and extracted by firms. The new approach may not be defined by movement, but by the value extracted from silence.