An extract from our comprehensive 2025 Study of Cryptocurrency Geography. Get your advance copy now!

We’re pleased to present the sixth iteration of the Chainalysis Global Crypto Acceptance Index. Each year, we examine both on-blockchain and off-blockchain data to pinpoint the nations at the forefront of mainstream cryptocurrency use. Our analysis spotlights countries demonstrating distinct cryptocurrency applications, investigating the factors propelling individuals around the world to embrace crypto.

Keep reading to explore:

Our Approach to the Global Crypto Acceptance Index

The Global Crypto Acceptance Index is constructed from four sub-indices, each reflecting countries’ use of diverse cryptocurrency services. We rank all 151 countries with sufficient data for each sub-index. Then, we weight the rankings based on attributes like population size and purchasing power equivalence. Next, we calculate the geometric mean of each country’s rank across all four categories. Finally, this final number is translated onto a 0-to-1 scale to give each country a final score. A country’s ranking is directly proportional to its final score (0-1).

To determine our sub-indices, we estimate transaction volumes for various cryptocurrency services and protocols in each country. This estimation is based on internet traffic patterns to the websites of those services. Although web traffic data isn’t foolproof – as some crypto users might use VPNs or other tools to mask their actual location – our index encompasses hundreds of millions of cryptocurrency transactions and more than 13 billion website visits. Thus, any inaccuracies because of VPNs are likely small in the larger data collection. Local cryptocurrency experts and operators worldwide provide added insights, reinforcing our methodology’s accuracy.

Below are descriptions of our sub-indices, how they are calculated, and the advancements in our approach since the previous year.

Sub-index 1: On-Chain Cryptocurrency Value Received Via Centralized Exchanges, Adjusted for GDP Per Capita (PPP)

This sub-index is intended to grade each country by the total amount of cryptocurrency received through centralized services. The rankings give more weight to countries where the amount is more meaningful in relation to the average person’s income. The total on-chain value received by users of centralized services in each country is measured and adjusted by GDP per capita using PPP (Purchasing Power Parity). This assesses income per resident. The higher the ratio of on-chain value received to GDP per capita (PPP-adjusted), the higher the country’s ranking. For example, if two countries received equal amounts of cryptocurrency through centralized services, the country with a lower weighted GDP per capita (PPP-adjusted) would be ranked higher.

Sub-index 2: On-Chain Retail Cryptocurrency Value Received Via Centralized Exchanges, Adjusted for GDP Per Capita (PPP)

We also evaluate the activity of non-expert, individual cryptocurrency users on centralized services, based on the value of crypto they transact in relation to the average person’s purchasing power. This involves estimating the amount of cryptocurrency received at centralized services by users in each country, as in sub-index 1, but focusing only on retail-sized transactions (transactions under $10,000). Countries are then ranked, with an emphasis on those having a lower GDP per capita (PPP-adjusted).

Sub-index 3: On-Chain Cryptocurrency Value Received Via DeFi Protocols, Adjusted for GDP Per Capita (PPP)

Countries are ranked according to DeFi transaction volume, with higher rankings for countries with lower GDP per capita using PPP adjustments.

Sub-index 4: On-Chain Institutional Cryptocurrency Value Received Via Centralized Services, Adjusted for GDP Per Capita (PPP)

Similar to our assessment of retail activity, we evaluate institutional user activity on centralized services by examining the value of cryptocurrency traded in comparison to the average person’s buying power. We estimate the crypto amount received on centralized services by users in each country, similar to sub-index 1, focusing on transactions over $1 million. Countries are ranked by this metric, but weighted to prioritize countries with lower GDP per capita using PPP adjustments.

Methodological Updates

Update 1: DeFi Retail Sub-Index Removal

This year, the retail decentralized finance (DeFi) sub-index was removed from our calculations for total on-chain activity. While DeFi is still a big part of overall transaction volume globally, our research shows that it makes up a much smaller part of overall user activity, especially when compared to centralized platforms. Including retail DeFi as its own category gave too much weight to a somewhat niche activity, skewing the crypto engagement results.

We decided to remove this sub-index to better reflect the real composition of the current crypto system and to avoid overemphasizing high-volume, low-frequency user behavior. This change makes sure that the index gives user-level activity a more even weight across service types, leading to a more reliable and representative way to measure grassroots acceptance.

Update 2: New Institutional Activity Sub-Index

In 2025, institutional participation in cryptocurrency reached new highs. With the approval of multiple spot bitcoin ETFs in the U.S. and clearer regulations in big markets, traditional financial institutions are getting more involved – not just as investors, but also as infrastructure providers and liquidity sources.

To show this growing influence, we added a new sub-index for institutional activity. This index captures the total value transferred by large-scale entities and smart contract addresses that are believed to belong to professional investors, hedge funds, custodians, and other institutional players, based on the transfer size. Any transfer over $1 million is put in this category. With this addition, the index now gives a more complete picture of global crypto involvement, covering both bottom-up (retail) and top-down (institutional) activity.

Even though our index still mainly focuses on grassroots acceptance, including institutional flows gives valuable insights into how mainstream the crypto system has become, especially in developed markets where institutional transactions are often done for regular retail customers.

The 2025 Global Crypto Acceptance Index: Top 20

Asia-Pacific continued to be the main hub for grassroots crypto activity in 2025, led by India, Pakistan, and Vietnam. These countries saw widespread adoption of both centralized and decentralized services. At the same time, North America moved up to the second-highest regional position because of regulatory momentum, like the approval of spot bitcoin ETFs and clearer institutional frameworks, which helped to legitimize and speed up crypto participation through traditional financial channels.

| Country | Overall index ranking | Retail centralized service value received ranking | Centralized service value received ranking | DeFi value received ranking | Institutional centralized service value received ranking |

| India | 1 | 1 | 1 | 1 | 1 |

| United States | 2 | 10 | 2 | 2 | 2 |

| Pakistan | 3 | 2 | 3 | 10 | 3 |

| Vietnam | 4 | 3 | 4 | 6 | 4 |

| Brazil | 5 | 5 | 5 | 5 | 5 |

| Nigeria | 6 | 7 | 8 | 3 | 8 |

| Indonesia | 7 | 9 | 7 | 4 | 7 |

| Ukraine | 8 | 4 | 6 | 8 | 6 |

| Philippines | 9 | 6 | 9 | 13 | 10 |

| Russian Federation | 10 | 8 | 10 | 9 | 11 |

| United Kingdom | 11 | 27 | 12 | 12 | 9 |

| Ethiopia | 12 | 16 | 19 | 7 | 20 |

| Bangladesh | 13 | 14 | 15 | 14 | 14 |

| Turkiye | 14 | 11 | 13 | 22 | 12 |

| Korea, Rep. | 15 | 12 | 11 | 24 | 13 |

| Yemen, Rep. | 16 | 15 | 16 | 21 | 16 |

| Thailand | 17 | 21 | 17 | 15 | 17 |

| Venezuela, RB | 18 | 13 | 14 | 37 | 15 |

| Japan | 19 | 17 | 20 | 16 | 27 |

| Argentina | 20 | 18 | 18 | 29 | 19 |

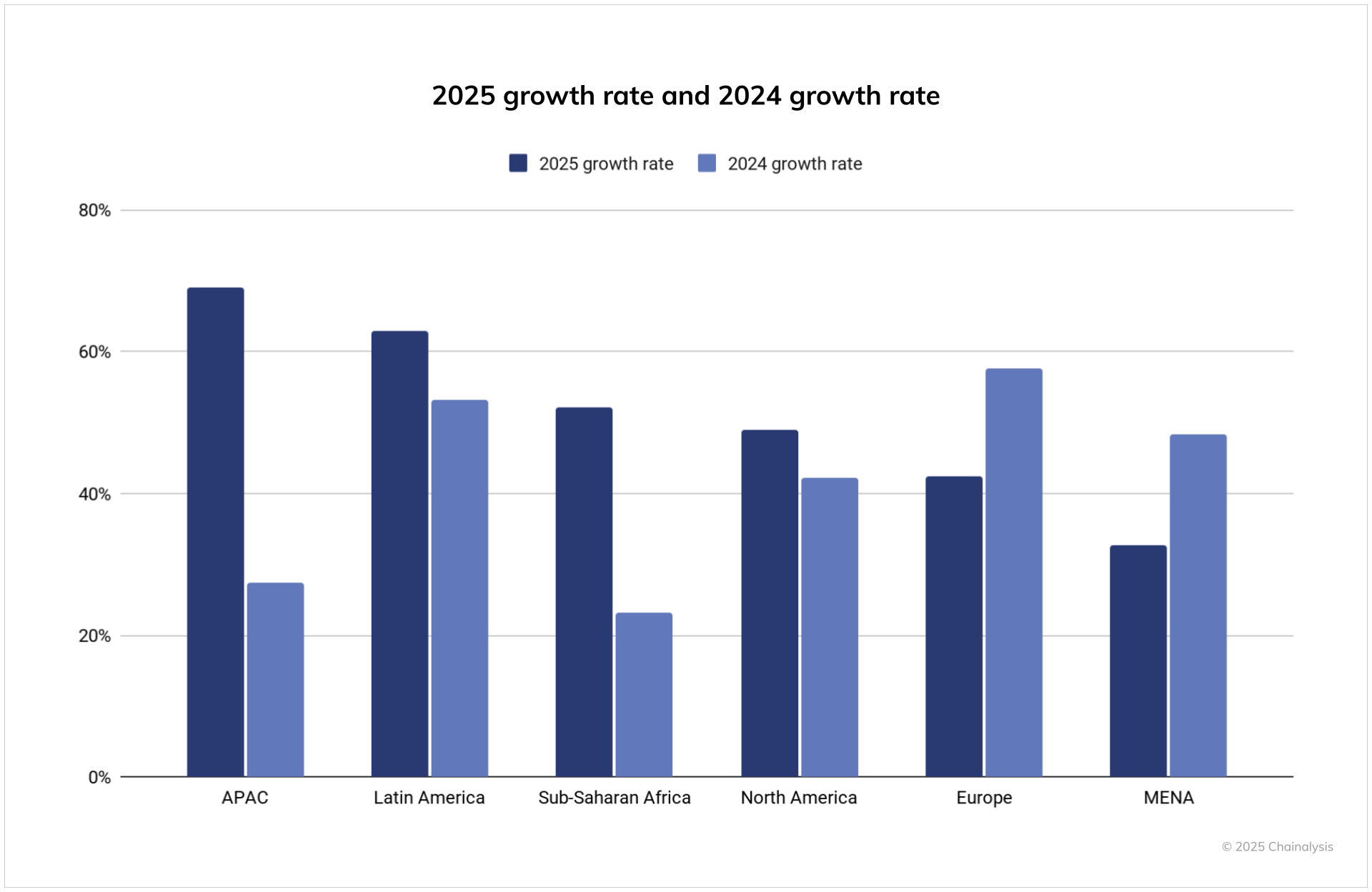

APAC Shows Fastest Growth

For the year ending in June 2025, the APAC area grew faster than any other area for on-chain crypto activity, with a 69% increase in value received. Total crypto transaction volume in APAC increased from $1.4 trillion to $2.36 trillion, helped by strong involvement in big markets like India, Vietnam, and Pakistan.

Latin America wasn’t far behind, with crypto acceptance growing by 63%. This reflects increased acceptance in both retail and institutional areas. Sub-Saharan Africa’s acceptance grew by 52%, showing that the area still relies on crypto for remittances and everyday payments. These numbers show a wider trend in crypto momentum toward the Global South, where real-world use is driving adoption.

{kind=link}

However, North America and Europe still lead in total numbers, receiving over $2.2 trillion and $2.6 trillion, respectively, in the past year. North America’s 49% growth reflects a year of renewed institutional interest, supported by the launch of spot bitcoin ETFs and better regulations. Europe’s 42% gain, while less than other areas, is still a big increase because of its already high base. This shows the continent’s continued institutional activity and growing user base. Meanwhile, MENA saw a more moderate 33% growth, suggesting a slower pace of acceptance compared to other rising markets, but total volume still went over half a trillion dollars.

Compared to the year before, this cycle saw faster growth in almost every area, with especially sharp increases in APAC and Latin America. Last year, APAC only grew by 27%, but that number more than doubled to 69% in the most recent period. Latin America also jumped from 53% to 63% year-over-year, strengthening the area’s position as one of crypto’s fastest-growing hubs. Europe, MENA, and Sub-Saharan Africa also saw quick growth, suggesting wide global expansion. Interestingly, North America’s growth rate also went up from 42% to 49%, which further indicates that the regulatory clarity and institutional inflows of 2025 are starting to show up in transaction data.

Adjusting for Population Shows a New Picture: Eastern Europe Dominates

Our index has usually focused on total activity adjusted for GDP per capita, which worked best when crypto was limited and used mainly by high-volume users. But as acceptance grows, population-adjusted metrics give a clearer idea of where crypto is really gaining traction.

When we adjust our index for population, we see a very different set of leading countries. Countries in Eastern Europe, including Ukraine, Moldova, and Georgia, top the list, showing high levels of crypto activity compared to their population size. Economic uncertainty, distrust in traditional financial institutions, and high technical literacy in the area might be driving adoption in Eastern Europe. These factors make crypto an attractive choice for saving wealth and doing cross-border transactions, especially in countries dealing with inflation, war, or banking restrictions.

The 2025 Global Crypto Acceptance Index Top 20, Adjusted by Population

| Country | Overall index ranking | Retail centralized service value received ranking | Centralized service value received ranking | DeFi value received ranking | Institutional centralized service value received ranking |

| Ukraine | 1 | 1 | 1 | 4 | 1 |

| Moldova | 2 | 2 | 2 | 14 | 2 |

| Georgia | 3 | 4 | 5 | 5 | 8 |

| Jordan | 4 | 10 | 16 | 1 | 24 |

| Hong Kong SAR, China | 5 | 17 | 9 | 6 | 9 |

| Vietnam | 6 | 7 | 6 | 10 | 7 |

| Latvia | 7 | 16 | 12 | 7 | 10 |

| Montenegro | 8 | 8 | 22 | 3 | 33 |

| Venezuela, RB | 9 | 3 | 3 | 52 | 4 |

| Slovenia | 10 | 25 | 7 | 16 | 5 |

| Estonia | 11 | 29 | 13 | 11 | 6 |

| Yemen, Rep. | 12 | 12 | 14 | 29 | 14 |

| Cambodia | 13 | 11 | 10 | 46 | 11 |

| Armenia | 14 | 6 | 8 | 56 | 12 |

| Singapore | 15 | 42 | 20 | 13 | 16 |

| Finland | 16 | 51 | 29 | 8 | 23 |

| Belarus | 17 | 9 | 17 | 39 | 27 |

| Korea, Rep. | 18 | 14 | 11 | 48 | 19 |

| Kyrgyz Republic | 19 | 20 | 15 | 47 | 15 |

| Portugal | 20 | 47 | 33 | 9 | 29 |

Stablecoins Increase Globally for Various Uses

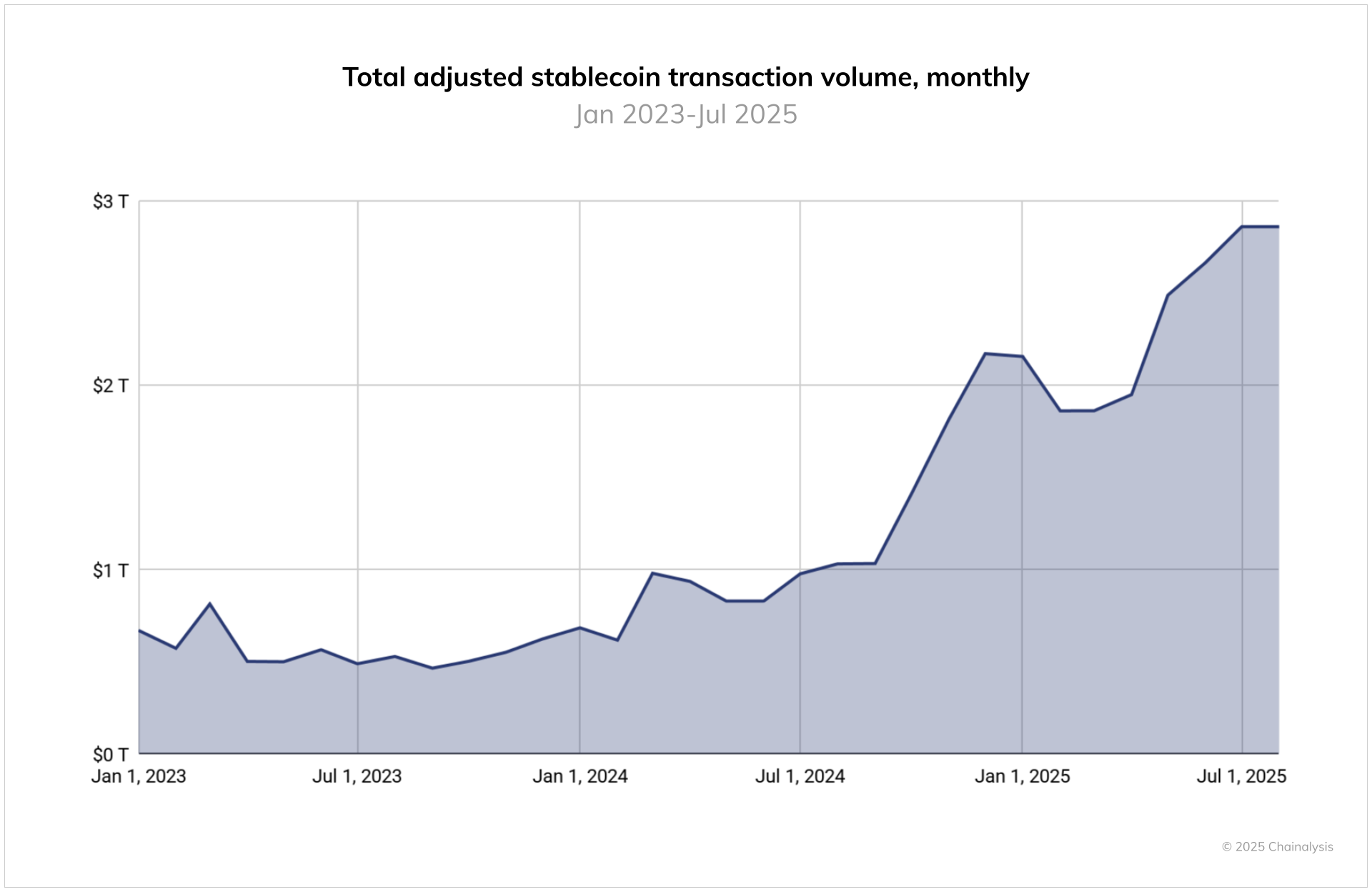

The stablecoin regulatory landscape has changed a lot in the past year. While the GENIUS Act in the U.S. hasn’t taken effect yet, its passage has led to strong institutional interest. In the EU, the MiCA stablecoin system has paved the way for the launch of licensed euro-referenced stablecoins like EURC.

Still, when we look at on-chain data, stablecoin transaction volume is mainly USDT (Tether) and USDC, which are much bigger than other stablecoins. From June 2024 to June 2025, USDT processed over $1 trillion per month, peaking at $1.14T in January 2025. USDC ranged from $1.24T to $3.29T monthly, with especially high activity in October 2024. These volumes show that Tether and USDC are still very important in crypto market infrastructure, especially for cross-border payments and institutional activity.

However, growth trends show a different picture. While Tether and USDC had some ups and downs, smaller stablecoins like EURC, PYUSD, and DAI grew quickly. For example, EURC grew almost 89% month-over-month on average, with monthly volume increasing from around $47 million in June 2024 to over $7.5 billion by June 2025. PYUSD also showed steady growth, rising from about $783 million to $3.95 billion in the same period.

These changes coincide with an increase in institutional activity around stablecoins. Stripe, Mastercard, and Visa have all launched products that let users spend stablecoins through traditional systems. Platforms like MetaMask, Kraken, and Crypto.com have introduced card-linked stablecoin payments. On the merchant side, partnerships between Circle, Paxos, and companies like Nuvei aim to simplify settlement in stablecoins. Traditional financial institutions like Citi and Bank of America have announced plans to explore expanding their offerings and possibly launching their own stablecoins.

Regionally, this may indicate a change in how stablecoins are used. USDC’s growth seems closely tied to U.S.-based institutional systems and regulated corridors. EURC’s growth suggests a growing interest in euro-denominated digital assets, possibly driven by MiCA-compliant platforms and European fintech adoption. PYUSD’s growth could indicate a wider interest in alternative, highly regulated stablecoins in retail and payment contexts. These trends show a fragmented but growing stablecoin landscape, where local uses are increasingly shaping global volumes.

Fiat On-Ramping: Bitcoin is Still the Main Entry Point

To assess how people are using fiat on-ramps, we looked at purchases made on centralized exchanges between July 2024 and June 2025, where users bought cryptocurrencies using fiat trading pairs. Each transaction was put into a category based on the type of asset bought, which helped us see which types of tokens are the main gateway into the crypto world.

Bitcoin leads by a large margin, accounting for over $4.6 trillion in fiat inflows during this period. That’s more than double the next-highest category, Layer 1 tokens (excluding BTC and ETH), which saw about $3.8 trillion in volume. Stablecoins were third at $1.3 trillion, and altcoins followed at about $540 billion. Other categories, including low-liquidity tokens, meme coins, and DeFi, each received less than $300 billion in fiat inflows.

The United States is still the world’s biggest fiat on-ramp, with over $4.2 trillion in total volume, which is more than four times the next-