The Rise of Digital Asset Treasury Firms

A novel type of publicly traded entity is gaining traction: Digital Asset Treasury Companies (DATCOs). These enterprises strategically prioritize the accumulation of digital currencies, most notably Bitcoin, as a primary business activity. While Strategy, led by Michael Saylor, established this approach by investing in Bitcoin in 2020, an influx of new participants and inventive capital strategies in the current year are highlighting DATCOs as a key element in both stock and cryptocurrency markets.

This analysis explores the DATCO landscape, analyzing the market dynamics influencing their valuations, illustrating their global distribution, and examining the financial frameworks that enable ongoing accumulation of significant crypto holdings. We will also consider the potential risks inherent in this business model, particularly when funding becomes limited or market premiums decline.

Key Findings

DATCOs currently possess over $100 billion worth of digital assets. Leading the pack are Strategy (MSTR), Metaplanet (3350.T), and SharpLink Gaming (SBET), all publicly listed.

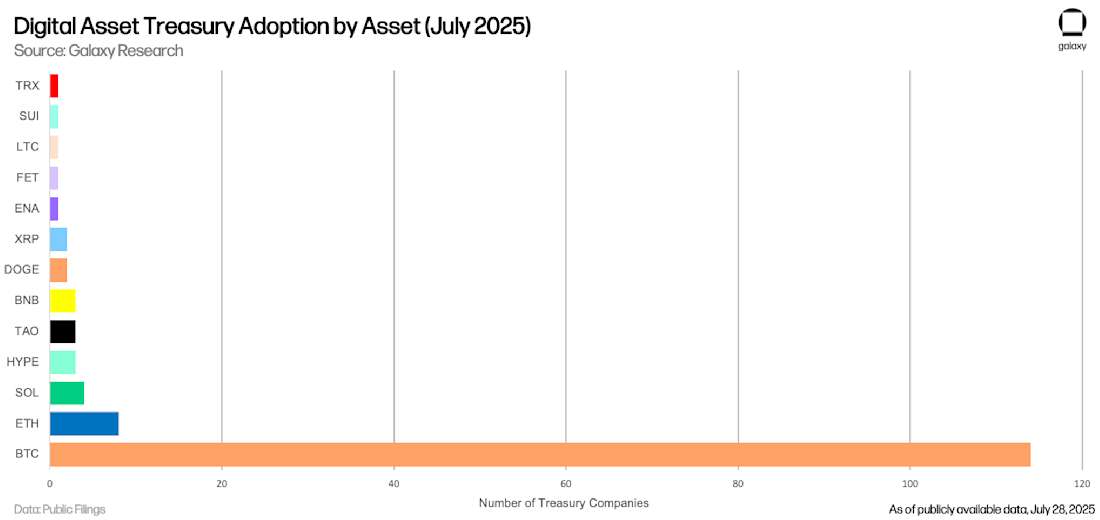

- Bitcoin-focused firms dominate, holding over $93 billion in BTC. Ethereum-centric DATCOs have accumulated over $4 billion in ETH.

- Treasury companies collectively hold 791,662 BTC and 1,313,318 ETH, representing about ~3.98% of the circulating BTC supply and ~1.09% of the ETH supply.

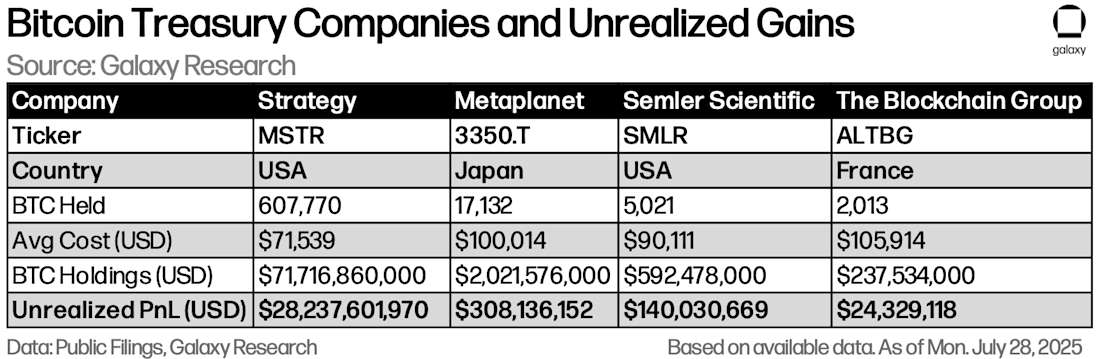

- Strategy has accrued more than $28 billion in unrealized profits, with Bitcoin holdings currently valued at $71.8 billion. Smaller players also exhibit low acquisition costs and significant potential for profit.

- New entrants are diversifying beyond Bitcoin and Ethereum, holding at least ten additional digital assets like SOL, XRP, BNB, and HYPE.

- Ethereum treasury firms are employing strategies such as staking and DeFi participation to generate returns on their holdings, an advantage unavailable to Bitcoin-only strategies.

- Although the United States remains a central hub, rising international interest in DATCOs is evident, driven by regional capital market forces.

- DATCOs differ from ETFs in their ability to raise and strategically allocate capital, potentially benefiting from narrative-driven investment.

- The DATCO model is susceptible to declining premiums, regulatory shifts, and disturbances in capital markets. Firms over-reliant on PIPEs or excessive borrowing face substantial downturns under less favorable market conditions.

- Currently, DATCOs are reinforcing upward pressure on cryptocurrency prices. However, should the sector grow excessively large, the potential for reversing this trend exists.

- Despite these considerations, the risk is currently theoretical. Excluding Strategy, DATCOs account for approximately $32 billion, or just ~0.83% of the $3.8 trillion total crypto market capitalization.

Core Terminology

The following terms are defined for clarity in understanding the DATCO model.

Digital Asset Treasury Companies (DATCOs): Publicly traded businesses holding Bitcoin or other digital assets as a core component of their corporate strategy. Unlike companies with peripheral crypto exposure (e.g., Tesla), DATCOs proactively seek to increase their digital asset holdings. Investors perceive investment in these companies as a leveraged, high-beta strategy for obtaining exposure to the underlying assets.

Equity Premium to NAV: This metric gauges how much higher a company’s share price is compared to its net asset value (NAV) per share. In this report, it is defined as:

Premium (%) = ((Share Price / NAV per Share) – 1) * 100

This metric reveals how favorably or unfavorably public equity markets assess the company’s digital asset portfolio.

Note: This differs from a full enterprise valuation premium, which includes debt and all potential shares, often used in analyzing these companies.

mNAV: “Multiple of Net Asset Value” – expresses the same concept as the premium, but as a multiple instead of a percentage.

Example: A stock trading at 2.75x mNAV shows a 175% premium.

ATM (At-the-Market Equity Programs): ATMs allow companies to gradually issue new shares at current market prices. When a company’s share price exceeds its NAV, each dollar generated through an ATM program enables the purchase of a higher amount of cryptocurrency per share than the resulting dilution. ATMs are a preferred method of raising capital for DATCOs because of their flexibility and avoidance of large, discounted offerings.

PIPEs (Private Investments in Public Equity): PIPEs are negotiated investments where large investors purchase newly issued stock at a set price, typically involving stocks with low liquidity or small floats. Although PIPEs facilitate quick fundraising, they often cause significant dilution and increase short-term pricing risks, explained in more detail later.

Bitcoin Yield: A key metric demonstrating how effectively a Bitcoin treasury company increases its Bitcoin holdings per diluted share over time. It measures the company’s efficiency in converting raised capital into Bitcoin without significant dilution. Higher Bitcoin Yield correlates with higher equity premiums.

Research Approach

This analysis uses data from both primary and secondary sources to assess the structure, market effects, and capitalization strategies of DATCOs as of July 2025. The approach emphasizes publicly accessible data and a standardized framework for all companies considered.

Sources of Information

The analysis is grounded in:

Company Selection

For a company to be categorized as a DATCO in this analysis, it must:

- Be publicly listed on a major stock exchange (e.g., Nasdaq, Tokyo Stock Exchange).

- Maintain significant digital asset holdings on its balance sheet.

- Follow a purposeful treasury strategy, where asset accumulation is a core business function.

- This specifically excludes Bitcoin mining operations where digital asset holdings are primarily a byproduct of mining activities, rather than deliberate capital allocation (e.g., Riot, Marathon).

- It also excludes firms like Tesla and Block, where digital asset acquisitions are not central to their primary business strategies.

Asset Holdings and Valuation

- Bitcoin and Ethereum holdings are based on the most recent publicly disclosed balances (as of July 28, 2025).

- Market prices used in calculations (as of July 28):

- Bitcoin price: $118,000

- Ethereum price: $3,800

- All foreign currency denominated holdings (e.g., Metaplanet in JPY, ALTBG in EUR) were converted to USD using spot FX rates at the time of reporting:

- EUR/USD: 1.17

- JPY/USD: 144.2

Background

The DATCO business model began with Michael Saylor’s MicroStrategy in 2020. The company became the first public company to allocate a substantial portion of its cash to Bitcoin (at a price of $11,650). This reimagined Bitcoin as a strategic reserve “immune” to currency depreciation.

MicroStrategy’s approach increased its market value and fostered a new perception of Bitcoin as a valuable corporate treasury asset, encouraging others to follow.

Saylor’s formula, which included issuing debt to purchase more Bitcoin, launching ATM equity programs, and actively promoting Bitcoin, became a repeatable strategy. Although MicroStrategy initially operated alone, it set the stage for other companies.

2023-2025 Trends

From 2023 to 2025, several significant factors contributed to the expansion of DATCOs from a singular instance to a broader trend:

- A 2023 update to FASB accounting rules allowed public companies to mark their digital asset holdings to market using fair-value accounting.

- The SEC’s 2024 approval of U.S. spot Bitcoin ETFs legitimized Bitcoin within mainstream finance.

- Escalating global tensions and fiat currency volatility drove more companies to seek Bitcoin as a store of value.

- In 2024, Metaplanet (3350.T) branded itself as “Japan’s MicroStrategy,” pursuing an aggressive Bitcoin accumulation strategy that showcased capital-efficient Bitcoin growth outside of the U.S.

- In the current year, there’s been a rise in treasury strategies focusing on alternative cryptocurrencies. Companies like SharpLink Gaming (SBET), BitMine (BMNR), and GameSquare (GAME) have adopted yield-enhanced treasury models that capitalize on staking rewards from blockchains using consensus mechanisms beyond proof-of-work.

Rationale for DATCOs

Digital asset treasury firms act as capital market mechanisms offering amplified exposure to digital assets, particularly Bitcoin, and an increasing range of other cryptocurrencies.

An earlier Galaxy Research report, “Why Are Bitcoin Treasury Companies Trading at Such High Premiums to NAV?” explores this phenomenon in depth.

Regulatory limits imposed on institutional investors, preventing direct crypto investments, contribute to the DATCO model’s appeal. As economist Lyn Alden observes in “The Rise of Bitcoin Stocks and Bonds,” global capital managed under mandates often prohibits direct crypto ownership but allows investment in public equities. DATCOs provide these investors (pensions, sovereign wealth funds, endowments) compliant access to the crypto market, which impacts share valuations. Investors are not just buying existing crypto assets but also benefiting from the regulatory arbitrage and capital formation potential.

Market Makeup and Asset Holdings

As of July 28, DATCOs collectively hold over 791,000 BTC and 1,300,000 ETH, representing approximately $93 billion and $5 billion, respectively, at recent market prices.

This data highlights Bitcoin’s prominence and the increased interest in Ethereum treasury strategies, especially among newer firms targeting staking and ecosystem exposure.

Strategy (MSTR) is still the dominant force, holding over 600,000 BTC, or 70% of Bitcoin held by public treasury companies, ranking third globally behind Satoshi Nakamoto and BlackRock’s ETF. The second tier includes firms like Metaplanet and Semler Scientific, which hold significant market value and unrealized gains.

While Strategy leads, companies like Metaplanet and Semler Scientific show considerable unrealized gains. Data reflects publicly disclosed balances and assumes a Bitcoin market price of $118,000. Note: Minor discrepancies between calculated and reported unrealized gains may reflect variable FX rates at the time of acquisition.

Aside from Bitcoin, a growing number of firms are launching strategies centered on alternative cryptocurrencies. These companies, which include SharpLink Gaming (SBET), Bit Digital (BTBT), and Tron Inc. (TRON), are acquiring non-Bitcoin digital assets and exploring strategies to generate yield. This model introduces a productivity layer that is currently not widely available for Bitcoin.

For a deeper analysis on the role of Ethereum in corporate treasury strategy, see analyst Christopher Rosa’s report on Ethereum as a treasury asset.

While Bitcoin dominates DATCO portfolios, firms are starting to include ETH, SOL, XRP, BNB, HYPE, and other tokens, based on specific theses.

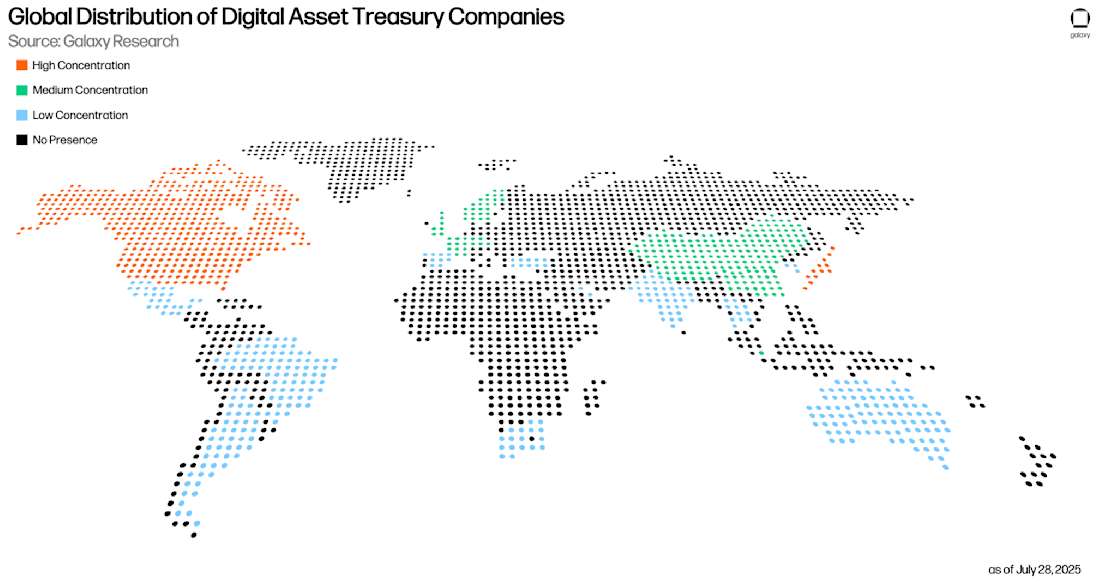

Global Presence of DATCOs

DATCOs are now a worldwide trend. The map below, created by Galaxy Research, illustrates the global distribution of DATCOs as of July 2025, based on disclosed crypto holdings.

Countries were tiered by DATCO activity: high, low, and medium concentration based on the number of public DATCOs and the extent of their holdings.

High-concentration countries have 10+ DATCOs, or significant crypto reserves (e.g., Japan because of Metaplanet). Medium-concentration countries have three to nine DATCOs, showing increasing institutional engagement. Low-concentration countries have one or two DATCOs, indicating early-stage participation.

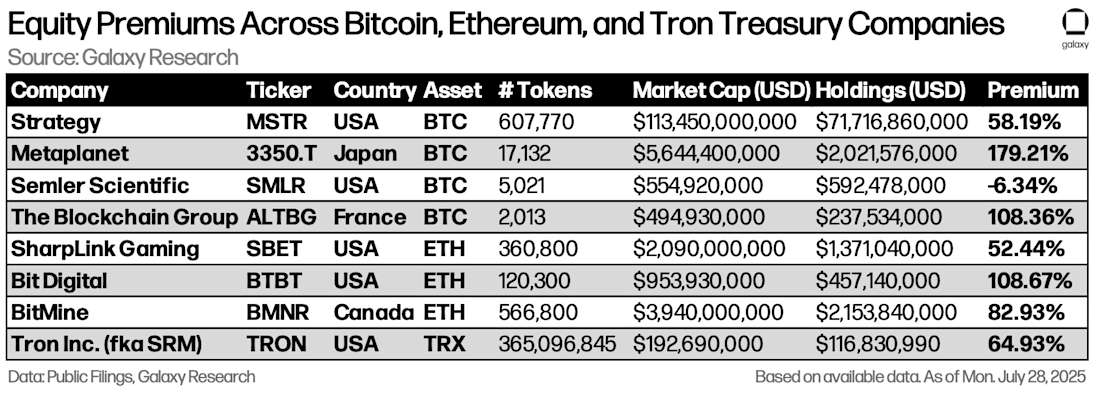

Valuation Differences and Equity Premiums

DATCOs are not all valued the same. Investors assign varying equity premiums to NAV, despite similar digital asset strategies.

The table below shows this, comparing eight Bitcoin, Ethereum, and TRX treasury companies with publicly disclosed holdings and market capitalizations as of July 28.

Some, like Strategy (MSTR) trade at modest premiums (58%), due to size and maturity. Metaplanet trades at a higher premium (179%) because of its aggressive approach.

Differences are more pronounced among ETH DATCOs. Bit Digital, for example, trades at 108% premium to its USD value of ETH holdings. The yield potential is factored into future capital efficiency.

Premiums cannot all be tied to treasury strategy. Companies have fundamental revenue streams. SharpLink Gaming, for example, operates a sports betting platform.

The chart also shows Tron Inc. (formerly SRM Entertainment), which staked 365 million TRX and changed its ticker to TRON. Despite a smaller treasury, it trades at a 64% premium, reflecting branding and ecosystem exposure. For altcoin treasuries, symbolism and signaling carry valuation weight.

Capital Deployment

DATCOs gain capital at a premium and reinvest to buy more crypto per share. The most effective are typically valued at the highest premiums. At-the-Market (ATMs) and Private Investment in Public Equity (PIPEs) are commonly used.

At-the-Market (ATMs)

At-the-Market (ATM) programs are typically used for continuous accumulation. Companies issue shares gradually at market prices, avoiding steep discounts and volatility. This allows firms to control capital raised and align with market sentiment.

When a DATCO’s share price is above NAV, each dollar obtained through an ATM buys more crypto per share than it dilutes. This boosts the NAV per share, widening the premium, a concept called “accretive dilution.” Metaplanet has effectively used ATMs to boost Bitcoin exposure.

ATM programs have risks, namely over use, but judicious utilization is a capital-efficient driver of growth for DATCOs.

Private Investment in Public Equity (PIPEs)

Private Investments in Public Equity (PIPEs) are used by smaller DATCOs to quickly access capital. Unlike ATMs, PIPEs are fixed-price deals with institutional buyers, at a discount. They are quick but result in dilution and future