Despite earlier signs of collaboration on cryptocurrency regulation, a group of Democratic Senators has reportedly proposed an alternative framework that could significantly impact decentralized finance (DeFi). The new proposal includes measures that could lead to the placement of DeFi protocols on a “restricted list” if they are perceived as carrying excessive risk.

Critics argue that this and other proposed actions could be devastating for the DeFi sector.

According to sources cited in a report by Punchbowl News, the Senate Banking Committee Democrats presented their proposal to Republican members on Thursday. The proposal seeks to mandate Know Your Customer (KYC) requirements for the user interfaces of cryptocurrency applications, including non-custodial wallets. Furthermore, it aims to remove certain legal protections currently afforded to crypto developers, a move that has drawn criticism from several industry observers.

Crypto legal expert Jake Chervinsky, among others, commented that this counter-proposal jeopardizes the potential for establishing a comprehensive regulatory framework for the crypto market. He highlighted that it could undermine the bipartisan support already achieved by the CLARITY Act, which successfully passed in the House in July with a vote of 294-134.

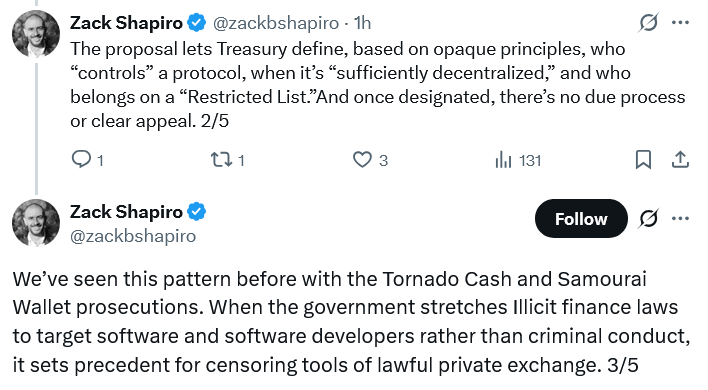

“This isn’t about regulation; it’s about prohibition,” Chervinsky stated, emphasizing the proposed measure that would allow the Treasury Department to create a “restricted list” for DeFi protocols deemed too risky. He argued that using a protocol on this list would become a criminal act.

Chervinsky further elaborated: “This proposal represents not a regulatory framework, but an unprecedented and potentially unconstitutional government takeover of an entire industry. It is not merely anti-crypto, but anti-innovation, and sets a dangerous precedent for the entire technology sector.”

According to Chervinsky, the Democratic Senators behind the counter-proposal include Mark Warner, Ruben Gallego, Andy Kim, Reverend Raphael Warnock, Angela Alsobrooks, and Lisa Blunt Rochester.

This development, occurring amidst a government shutdown, could be interpreted as a reversal of the regulatory momentum that had been building, especially considering previous pledges to establish the United States as a leading hub for cryptocurrency innovation.

Counter-Proposal Conflicts with Bipartisan RFIA Draft

The proposed measures also stand in contrast to elements of the Senate Banking Committee’s Responsible Financial Innovation Act (RFIA) draft, a bipartisan initiative introduced on September 9. The RFIA aims to grant the Commodity Futures Trading Commission (CFTC) oversight of spot markets and to curtail what some perceive as overreach by the Securities and Exchange Commission (SEC).

The RFIA further seeks to strengthen protections for cryptocurrency developers, allowing them to innovate without the constant fear of prosecution, particularly in light of recent actions against developers associated with Tornado Cash and Samourai Wallet.

Digital Chamber Argues Policy Should Not Penalize Decentralization

Zunera Mazhar, the vice president of government and policy affairs at the Digital Chamber, characterized the proposed measures as overly restrictive and ultimately ineffective. She cautioned that they could drive innovation overseas, rather than addressing the genuine risks associated with the industry.

Related: Democrats scrutinize bank regulator regarding Trump’s connections to stablecoins

Instead, Mazhar suggested that the Democrats should concentrate on targeting the key points where illicit financial activity occurs, adopting a risk-based approach that does not stifle innovation or create unnecessary regulatory uncertainty.

“Effective policy should not penalize decentralization. It should protect consumers, foster innovation, and combat illicit finance at its source.”

This is a developing story. Further updates will be provided as more information becomes available.

Magazine: EU’s controversial Chat Control bill faces delays, but the fight continues