1. Overview

Since its inception in 2017, Chainlink has cemented its position as a vital component of the decentralized oracle network landscape. This project acts as a bridge, connecting blockchain technology with real-world information. Oracles are fundamental infrastructure, handling essential data needs like price feeds, enabling cross-chain operability, and providing access to tangible assets (RWA). With the rise of decentralized finance (DeFi), interconnected blockchain systems, and the tokenization of real-world assets as primary trends, Chainlink’s importance and strategic significance have become increasingly clear. This analysis aims to thoroughly investigate the reasons to invest in LINK, examining its medium-to-long-term prospects by factoring in broad market movements, progress in the RWA sector, Chainlink’s tech and financial framework, value accrual methods for its token, competitive forces, and future trajectory.

2. Market Conditions and Strategic Potential

The tokenization of physical assets (RWA) has recently become a major focus and a high-growth area within the crypto market. RWA involves digitally representing assets like bonds, currencies, property, certificates of deposit, precious metals, carbon credits, intellectual property, and even computational power on a blockchain. This transforms them, through smart contracts, into programmable, transferable, and composable instruments. Market research suggests that the RWA market could potentially be worth hundreds of trillions of dollars. For example, tokenized U.S. Treasury markets alone exceed $26 trillion, while the entire crypto market was valued at roughly $2.5 trillion in early 2025. This illustrates that significant RWA adoption could potentially lead to ten-fold or greater growth within the crypto sector. Investment firms, like M31 Capital, predict that tokenization of global assets could reach $30 trillion within the next decade, representing a major catalyst for blockchain technology applications. Furthermore, financial giants are signaling a shift in strategy. BlackRock is exploring tokenized money market funds, JPMorgan is testing Treasury tokenization settlements on their Onyx platform, and SWIFT alongside DTCC are exploring blockchain options for international payments and settlements. All these actions suggest that traditional financial entities are steadily exploring the on-chain economy through controlled trials. Oracles are key to unlocking the value of tokenized assets, serving as the crucial link between on-chain and off-chain environments. Chainlink, the leading oracle network worldwide, handles over 80% of data requests on major blockchains like Ethereum, making it indispensable to the RWA infrastructure. Consequently, Chainlink is uniquely positioned to benefit in the context of rapid RWA market expansion.

The convergence of RWA and institutional on-chain activity demands a robust foundation built on “reliable data, cross-chain settlements, and compliant implementation.” For instance, on-chain representations of U.S. stocks and ETFs require not only price data but also awareness of market hours, circuit breakers, data recency, and other contextual information to ensure accurate clearing and risk management. In August 2025, Chainlink introduced Data Streams, standardizing this suite of “data flow criteria for established market environments.” Major platforms like GMX and Kamino have adopted Data Streams, covering popular assets like SPY, QQQ, NVDA, AAPL, and MSFT. Currently, Data Streams are available across 37 networks, streamlining the development of compliant derivatives, synthetic assets, and collateral/lending platforms. Industry reports value the current RWA market at over $100 billion, with forecasts predicting it could reach several trillion dollars by 2030. Oracles and compliant interoperability are indispensable in this evolving landscape. SWIFT’s experiments and Proof-of-Concept exercises between 2023 and 2024 have demonstrated the viability of using existing SWIFT standards combined with Chainlink infrastructure to connect banks to multiple blockchains. Moreover, the DTCC Smart NAV pilot has successfully placed critical reference data, such as fund NAVs, on-chain, clearly indicating CCIP as the chosen interoperability solution. These examples set critical precedents for shifting traditional financial infrastructure encompassing “data, regulations, and settlement” processes onto the blockchain.

Chainlink’s value proposition is based on its oracle network capabilities. Blockchains like Ethereum cannot access off-chain data directly; oracles bridge this gap, providing verifiable, dependable, and decentralized data feeds. Chainlink ensures data accuracy through a network of thousands of independent nodes, which safeguards against single-point vulnerabilities and tampering. The product portfolio includes price feeds, verifiable random functions (VRF), and cross-chain interoperability protocols (CCIP). According to recent data, Chainlink secures over $11.3 billion in Total Value Secured (TVS), holding approximately 46% of the oracle market share, significantly outperforming competitors such as Pyth and Band. Within the Ethereum DeFi ecosystem, over 90% of lending platforms and derivative applications depend on Chainlink data. Core protocols like Aave, Synthetix, and Compound rely on Chainlink for accurate price information. Compared to other large-cap tokens like XRP, whose utility remains limited, LINK demonstrates clear advantages in practical integrations and revenue generation. Despite XRP’s market capitalization previously exceeding LINK’s by over 15 times, XRP’s ecosystem integration and adoption by institutions lag considerably behind Chainlink. This comparison suggests that LINK is currently undervalued and poised for potential appreciation through a re-evaluation of its real-world utility.

3. Key Elements of Value Accrual and Growth in RWA

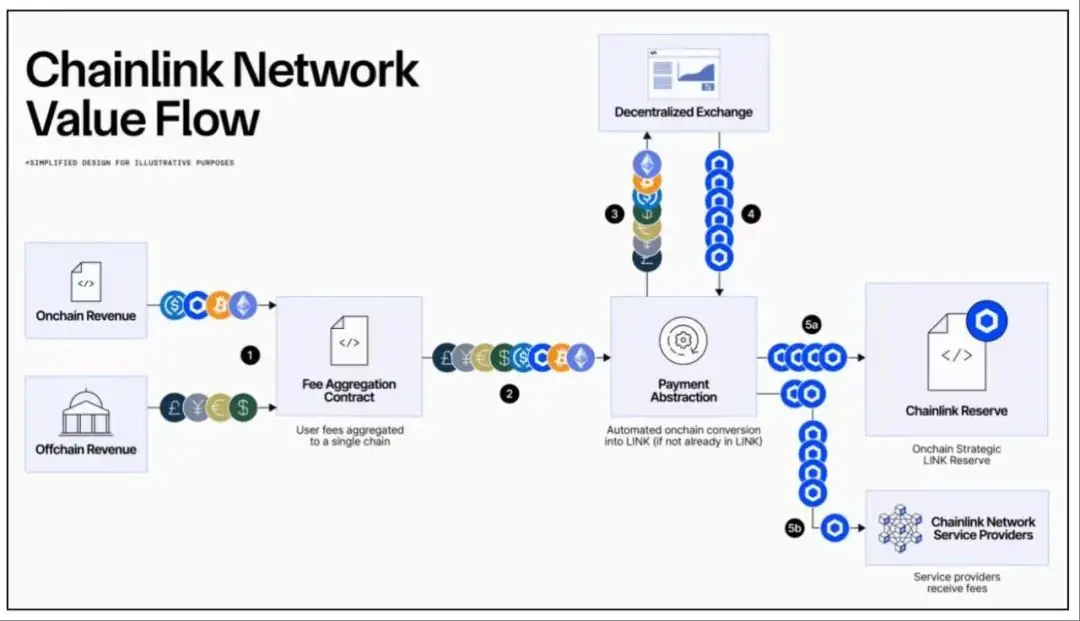

The most innovative feature of Chainlink’s financial structure is its value capture mechanism. First, users are required to pay for data requests using LINK tokens. These fees are partially distributed to node operators, with the remainder directed into the “LINK Reserve.” This reserve then automatically purchases LINK, injecting buying pressure into the market and driving up the token’s price. Second, the increasing use of RWA and DeFi will generate greater demand for frequent data updates and cross-chain data transfers, leading to exponential growth in protocol revenue. This, in turn, enhances the reserve buyback capacity, amplifying LINK’s value. Third, LINK’s staking mechanism, which provides approximately 4.3% annual yield, encourages long-term holding and node participation, reducing the circulating supply. These elements form a positive cycle involving adoption, revenue generation, token buybacks, price appreciation, and overall ecosystem growth, creating a flywheel effect. From late 2023 to early 2025, LINK’s price rose nearly 50%, indicating market anticipation of this mechanism.

From a financial perspective, Chainlink is beginning to showcase its commercial capabilities. Recent data shows revenue exceeding $110,000 within a 30-day period, with a noticeable upward trend. Despite this figure being modest compared to larger DeFi platforms, Chainlink’s revenue is potentially more sustainable due to its B2B infrastructure nature. Furthermore, Chainlink maintains a substantial market share, with over 46% indicating it has become an industry standard. Compared to competitors like Pyth and Band, Chainlink benefits from a larger number of nodes, deeper strategic partnerships, and enhanced integration with financial institutions. Upon successful implementation of RWA use cases, the demand for data resulting from asset tokenization is projected to surpass current DeFi scales, significantly amplifying LINK’s revenue opportunities.

Chainlink primarily uses a “B2D/B2B2C” on-demand payment system (fees for price/data services, CCIP cross-chain services, PoR audit/monitoring, Data Streams subscriptions, etc.). Revenues from these services are distributed to nodes and security budgets, integrated with Economics 2.0 for staking/collateral, alerts/penalties (slashing) to ensure greater economic security and better service through willingness to pay to achieve stronger revenue. Staking v0.2 boosts the pool cap to 45 million LINK (roughly 40.875 million for the community, with the remainder for node operators). By introducing an unbinding mechanism (28-day cool-down and 7-day withdrawal window) security and flexibility can be balanced. The node collateral portion establishes a baseline reward rate which can be combined with delegated rewards. The increased revenue from user fees should strengthen the cash flow characteristics of Staking. Media and research documents have repeatedly highlighted the “LINK reserve,” or a mechanism to purchase LINK periodically from sources like enterprise/service fees, to improve liquidity and supply elasticity in exchanges. However, as this mechanism is primarily discussed in media, and there is no systematic official whitepaper, it should be considered optional in valuations.

Chainlink is actively expanding RWA infrastructure. It is working with ICE to link off-chain pricing for foreign exchange and precious metals to blockchains, providing dependable values for tokenized assets. The CCIP facilitates asset and data transfer between blockchains, which is crucial for RWA asset liquidity in multichain setups. Additionally, Chainlink’s offerings, such as the DeFi Yield Index, strive to create traceable yield indices by integrating multiple DeFi yields, thereby providing financial institutions with integrable on-chain tooling. Chainlink serves as a standard interface across various sectors, including agricultural assets, intellectual property, computing power, and cross-border money market funds. The RWA tokenization relies on trusted data inputs and cross-chain settlement, establishing Chainlink as an important structural player.

4. Product Capabilities and Collaboration Within the Ecosystem

Chainlink’s product portfolio is divided into four layers: (1) Data: Price Feeds, Proof of Reserve, State Pricing (pricing for DEX assets), Data Streams (low-latency high-frequency data and metadata); (2) Interoperability: CCIP (cross-chain messaging/value transfer, programmable transfers, CCT standards), with v1.6 in 2025 adding Solana as the first non-EVM mainnet and reducing cross-chain execution costs, increasing the expansion speed to new chains; (3) Computing and Automation: Functions, Automation, VRF, etc.; (4) Compliance and Governance: Risk management, monitoring, and compliance modules for financial market regulation (with ACE added recently). CCIP v1.6 is claiming to support 57+ chains on the mainnet, recognizing many chains as official. On the Solana side, Zeus Network has combined CCIP and PoR, allowing assets like zBTC to move across Base/Ethereum/Solana/Sonic, expanding the BTCFi sector. Introduced in August 2025, the ICE Consolidated Feed offers institutional-grade foreign exchange and precious metal data and Data Streams reduce latency and provide anti-manipulation features, facilitating the operation of asset classes like foreign exchange, gold/silver, and others on-chain.

In ecosystem development, Chainlink builds connections with “financial institutions, public chains, DeFi protocols, and data providers.” For institutions, Swift is using existing standards to connect multiple chains with CCIP; the 2024 Swift/UBS/Chainlink pilot links tokenized assets with traditional payment methods; the 2024-2025 DTCC Smart NAV pilot designates CCIP as the interoperability layer. In August 2025, ICE and Chainlink announced a data collaboration, inputting ICE’s foreign exchange and precious metals data into Data Streams, providing real-time data for over 2,000 on-chain applications and institutions. On the asset management and banking side, ANZ, Fidelity International, Sygnum, and others are on Chainlink’s capital market cooperation list. CCIP is steadily operating on EVM chains like Ethereum, Arbitrum, Optimism, Polygon, Base, Avalanche, and BNB. In 2025 Solana was integrated, with Kamino and GMX-Solana already connecting to Data Streams, increasing the availability of U.S. stock and ETF data for institutional derivatives and collateral lending in non-EVM ecosystems. Aside from digital assets, there has been an expansion into U.S. stocks/ETFs, foreign exchange/precious metals in 2025, expanding asset coverage.

5. Investment Considerations and Potential

LINK is currently forming a new support structure between $22 and $30. If this range can stay stable, it can be the base for further increases. After ETH broke through $400 in 2020, it entered an exponential growth phase, and LINK could have a similar trend. Funds have been flowing from exchange wallets to cold storage and staking contracts, indicating accumulating long-term funds. This, combined with buybacks, suggests a bullish trend in the medium to long term.

Chainlink is ranked first by oracles, with market share between 46% and 68%. Its share in Ethereum data is around 80%. Its strategy focuses on “high-value scenarios.” While competitors (like Pyth) have had TVS increases by connecting with exchanges and providing high-frequency data in 2023-2024, the compliance cooperation with Swift, DTCC, and ICE is helping to retain Chainlink’s institutional compliance and standardization. This allows the product matrix to meet the demands of the traditional market. Coverage across EVM/non-EVM with Solana is a milestone. Short-term fluctuations are normal, but for “multi-asset, multi-chain compliance,” standards and ecosystems are crucial.

Chainlink is an infrastructure and levered RWA investment. M31 Capital suggests LINK has 20-30 times upside potential in RWA, based on the potential of the RWA market to reach $30 trillion, and LINK’s position as the data standard. The current market cap is undervalued compared to projects like XRP. From a risk-reward perspective, LINK is good for long-term investors.

There are 1 billion LINK tokens, distributed as follows: 35% public sale, 35% node incentives, and 30% company. Staking v0.2 secures the network. Fees are gradually shifting from “pure expectations” to “cash flow.” There are three layers of demand: usage demand, security demand, and liquidity demand. Supply releases and the “node incentive usage” will impact the market’s supply and demand balance.

Chainlink’s TVS has hit hundreds of billions in 2025. Its official homepage states it has “cumulatively supported on-chain transaction volumes in the hundreds of trillions of dollars.” Recent fees are climbing, with penetration into high-quality scenarios (GMX/Kamino’s Data Streams, and U.S. stocks/ETFs, foreign exchange, and precious metals) is likely to bring a “qualitative change.” The staking pool filled quickly after launching v0.2, indicating the desire for network security. Projections are based on TVS fee rates, scenario weight, and chain coverage.

LINK’s value can be broken down into three parts: (A) “platform option value” for RWA activities, (B) “operating cash flow,” and (C) “security budget” with staking and fee sharing. Three scenarios are presented: crypto-native expansion; Data Streams increase ARPU; settlement and tokenization increase CCIP transfers. Important tracking metrics are Data Streams protocols, CCIP messaging, PoR monitoring, staking inflows, and institutional data usage.

6. Risks and Strategies

Despite its lead position, Chainlink has risks. Competition with cost-effective models can decrease market share. The speed of fees and value capture may not meet expectations. There are uncertainties regarding cross-border data regulations. Long-term data and messaging require stable “defense in depth” and node governance. It is important to cautiously address new mechanisms, such as the “LINK reserve,” if not implemented officially.

LINK suits medium-to-long-term holding. Staking can help reduce circulation. Cooperation with financial institutions should be deepened. RWA data and settlement mechanisms should be standardized. Ecosystem developers can use Chainlink’s data and service interfaces as the foundation for DeFi and RWA products.

LINK (Chainlink) is a core asset of “on-chain infrastructure”. Its data and oracle service is the de facto standard. CCIP is steadily expanding. Its product family and institutional data drives expansion from crypto-native to traditional asset data. Chainlink’s economic model couples network fees with security and ecosystem growth through “fees — services — collateral — nodes — ecosystem return”. Given institutional cooperation, multi-chain coverage, demand for RWA, and non-EVM ecosystems, LINK has both β and α characteristics.

7. Final Thoughts

Chainlink is a leader in oracles and cross-chain infrastructure. Its value capture mechanism forms a strong economic model. As the RWA market expands, its uses will grow, increasing both revenue and value. LINK is currently undervalued compared to other high-market-cap tokens, with rebound potential. Despite risks in technology and competition, Chainlink could be a key player in linking traditional finance to crypto.

ChainCatcher advises readers to approach blockchain with caution, be risk aware, and be wary of virtual token speculation. All content on this site is market information, and does not constitute investment advice. Please click “Report” to report any sensitive information, and we will handle it promptly.