Solana has witnessed an influx of funds over the past month, even though user engagement demonstrates inconsistent progress.

According to data from

DeFiLlama

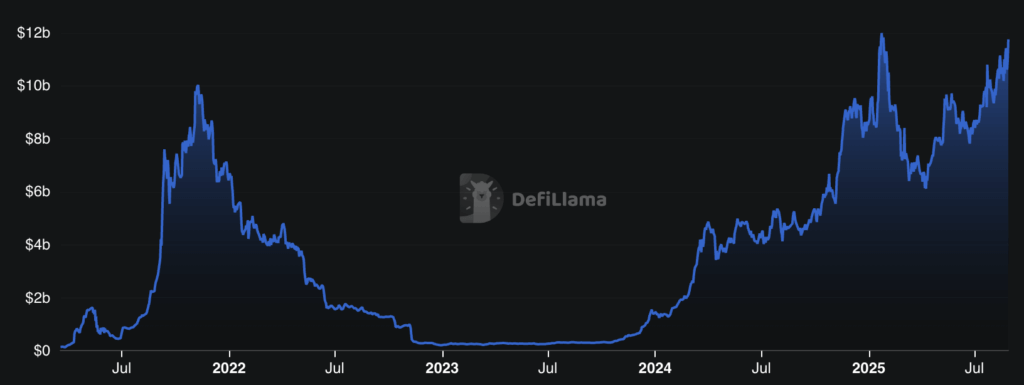

, Solana’s daily decentralized exchange (DEX) trading volume recently hit approximately $4.6 billion, with perpetuals contributing close to $2.1 billion. The supply of stablecoins is around $12 billion. The Total Value Locked (TVL) natively on Solana is nearing its record high at $11.7 billion, while bridged TVL is estimated at around $57 billion. Daily active addresses remain in the millions.

Simultaneously, chain fees over a 24-hour period are about $1.6 million, with daily transactions reaching roughly 65 million. This pattern indicates high liquidity and consistent throughput, rather than a rapid increase in fee generation. At the time of this writing, SOL was trading around $198.

This disparity between liquidity and utilization has been evident since the second quarter of the year.

Messari’s Q2 report on Solana

highlighted a 45.4% drop in average daily spot DEX volume to $2.5 billion compared to the previous quarter. This decrease occurred after the hype around meme coins subsided, even as DeFi TVL increased, positioning Solana as the second largest network by TVL.

This context helps explain the current dynamics: capital and order flow are present and readily available when risk appetite returns. However, fee and revenue growth remain closely tied to market cycles and the nature of network activity.

The Solana mix

The derivatives market further confirms the availability of liquidity.

CoinGlass

shows strong activity in Solana perpetuals.

Funding rates seem well-managed, indicating that leverage is present but not excessive. This is important for the market’s structure. Stable funding reduces the likelihood of large, forced liquidations and ensures market makers maintain sufficient depth when spot prices lead or follow.

Even without a corresponding surge in monetization, on-chain funds and trading platforms are still focusing on Solana. DeFiLlama indicates that stablecoins are above $12 billion, and daily DEX turnover is multi-billion dollar. Still, app fees and overall chain revenue are significantly lower than the peaks recorded earlier in the year.

This combination means users can efficiently route significant volumes through Solana at low marginal costs, which is beneficial for market making, MEV-aware routing and aggregation, and arbitrage across different platforms. However, this doesn’t guarantee higher fee revenue for validators and applications.

The context from Messari’s Q2 report adds another layer of understanding. The report pointed out that liquidity providers and aggregators gained more market share during the first half of the year as speculative trading cooled down. Protocol revenues did not keep pace with trading activity.

Furthermore, stablecoins continue to be a crucial foundation for settlement and inventory management on Solana, maintaining balances on the chain even when transaction activity decreases.

In the short term, the focus is less on potential catalysts and more on the composition of network activity. If activity continues to favor low-fee transfers and efficient DEX routing, liquidity will remain abundant, and spreads will stay tight. However, fee capture and revenue at the application level could lag behind.

If trading volume shifts towards higher-fee activities, revenue and fees should increase without requiring additional infrastructure.

Currently, Solana is handling substantial trading volumes with only a modest increase in fees. This dynamic ensures Solana remains a magnet for liquidity, but user monetization doesn’t match the volume of transactions.