On July 31st, the head of the U.S. financial regulatory body, Paul Atkins, unveiled a sweeping initiative known as “Project Crypto.” This extensive reform plan, championed by the Securities and Exchange Commission (SEC), aims to overhaul the regulatory framework for digital assets in the United States. The goal is to facilitate the integration of financial markets onto blockchain technology, thereby realizing the vision put forth during the previous administration to establish the U.S. as the world’s premier hub for cryptocurrency innovation.

The previous “regulation through enforcement” approach pushed innovative crypto companies overseas to places like Singapore and Dubai. Further, it caused the U.S. to forfeit its chance to spearhead the next generation of financial infrastructure. “Project Crypto” represents a stark departure from past regulatory suppression tactics and signals a significant shift in strategy. It sends a clear message to the industry that the era of blockchain-based finance in the U.S. is now beginning.

Easing Regulations: A Prime Opportunity for DeFi Platforms Like Uniswap and Aave

The previous stances of SEC leaders on digital currencies and related financial products – especially Decentralized Finance (DeFi) – largely shaped activity levels in the U.S. digital asset market. During Gary Gensler’s tenure, the SEC concentrated on classifying tokens as securities and heavily using enforcement actions. This included encompassing token trading within the existing securities regulations. His administration oversaw 125+ enforcement actions related to cryptocurrency, which involved subpoenas and lawsuits against decentralized finance projects like Uniswap and Coinbase. These actions brought the compliance threshold for on-chain products to an all-time high.

Since Paul Atkins took charge in April of 2025, there’s been a radical regulatory makeover at the SEC. He immediately launched a discussion called “DeFi and the American Spirit” to promote less strict regulations on DeFi.

Atkins emphasized the original intent of U.S. securities laws within “Project Crypto,” stating their purpose is to safeguard investors and maintain market integrity. He believes these regulations should not stifle technological advancements, especially those that remove intermediaries. He asserts that DeFi protocols like automated market makers (AMMs) facilitate decentralized financial activities and are deserving of legitimate institutional support. Developers who “only write code” should be afforded strong protection and exemptions. Also, Atkins believes that intermediary entities that want to supply services built on these protocols should be given clear and feasible compliance pathways.

This change in regulatory direction undoubtedly sends positive signals to the entire DeFi ecosystem. In particular, protocols such as Lido, Uniswap, and Aave, all of which have established network effects and are largely autonomous, will benefit from institutional recognition and have more room for growth under a non-intermediated regulatory logic. Token valuations for projects previously impacted by the “securities shadow” are also anticipated to reshape as a result of relaxed policies and a return of market participants, potentially transitioning into “mainstream assets” in the investor community.

Next-Gen Financial Gateways: How Super-Apps Will Remodel Trading Platforms

Paul Atkins’s concept of a “Super-App” is both impactful and groundbreaking. He explained that current securities firms face difficult compliance and redundant licensing issues when providing services around traditional securities, crypto assets, and blockchain-based offerings. Atkins believes this problem hinders product innovation and user experience. He proposed that future trading platforms should integrate a suite of services including non-securities crypto assets (like $DOGE), securities crypto assets (like tokenized stocks), traditional securities (like U.S. stocks), and also staking and lending, all under a single license. This represents a streamlined approach to compliance and a new cornerstone of competitive advantage for trading platforms.

Regulatory bodies intend to encourage implementing this super application architecture. Atkins has said that the SEC will create a regulatory framework allowing different cryptocurrencies to co-exist and trade on SEC-registered platforms, whether or not they are considered securities. Moreover, the SEC is considering how to utilize current authority to ease listing requirements for particular assets on non-registered exchanges (such as platforms with just state-level licensing). Even derivatives platforms overseen by the CFTC could potentially incorporate certain leverage functions to unlock higher trading volume. The overarching goal of regulatory reform is to remove the hard boundary between securities and non-securities, allowing platforms the flexibility to allocate assets based on user needs and product characteristics instead of restrictive compliance frameworks.

Coinbase and Robinhood are the most apparent benefactors of this change. They have created broad trading infrastructures spanning mainstream crypto assets, standard securities trading, lending, and wallet services. Encouraged by Project Crypto, they might become the first platforms to take advantage of the new policies. By delivering one-stop services, these platforms can better merge on-chain products with traditional users. Notably, Robinhood has acquired Bitstamp and officially launched tokenized stock trading, which lists U.S. stocks like Apple, Nvidia, and Tesla in the ERC-20 format. This is a preview of the Super-App model: blending stock trading with on-chain protocols without disrupting user experience.

Coinbase is developing its developer ecosystem using the Base chain, with the goal of uniting exchanges, wallets, social media, and application layer services. If they can seamlessly merge traditional securities with on-chain assets at the compliance level, Coinbase could evolve into the “on-chain version of Charles Schwab” or a “next-generation Morgan Stanley”, serving not only as a gateway to assets but also as a platform for financial tools.

When the Super-App architecture is fully adopted, it will become a crucial arena for trading platforms to compete. A leading position in the subsequent stage of financial infrastructure improvements will go to whoever achieves compliant, multi-asset aggregated trading. Since the regulatory perspective has become increasingly evident, platforms are already quickening their integration, resulting in a streamlined trading process, an expansion of product variety, and a financial system that closely echoes the potential of the future for the end users.

ERC-3643: Bridging the Gap from Protocol to Policy for Real World Asset (RWA) Compliance

Paul Atkins highlighted the tokenization of traditional assets and particularly recognized ERC-3643, a token standard worthy of reference in regulatory frameworks. This was the only token standard mentioned throughout his address, signaling its importance and transition from a tech protocol to a policy-level reference model.

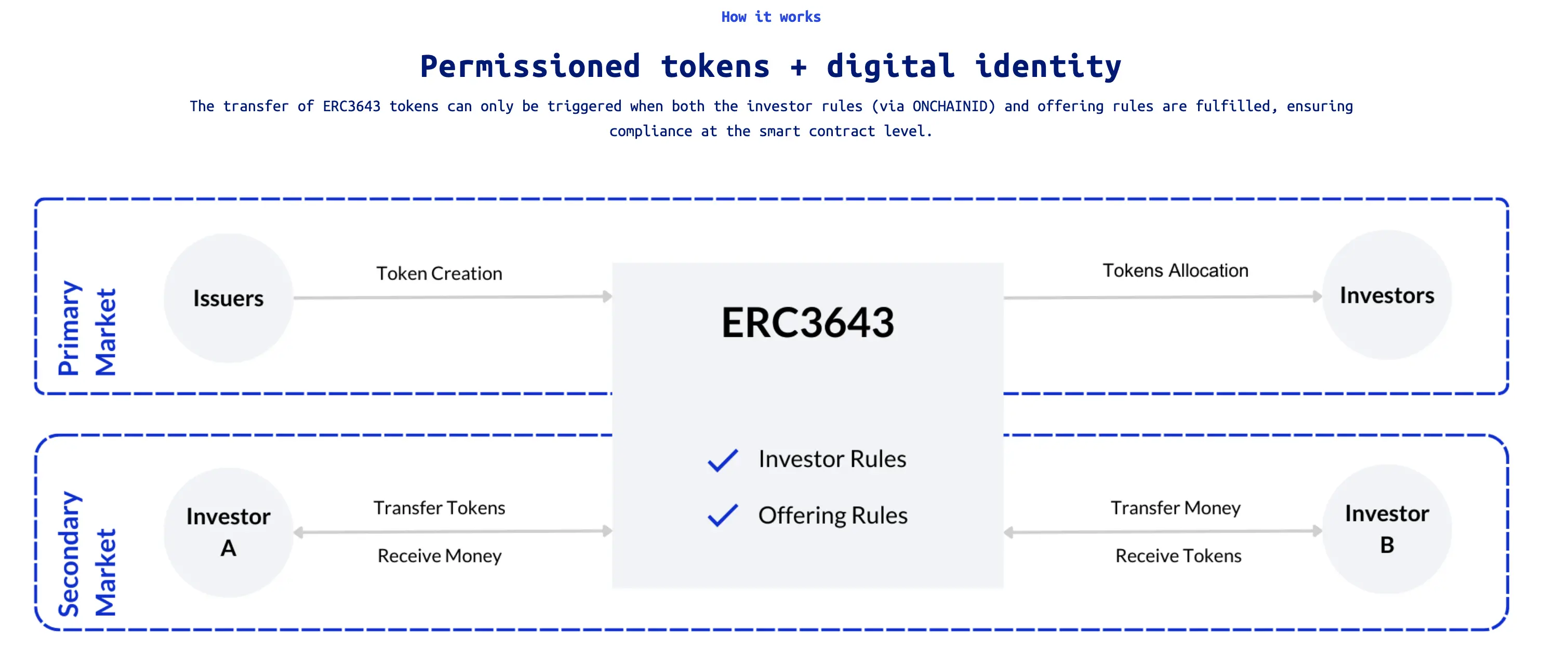

Paul stressed that, when creating an innovative exemption framework, the SEC will prioritize token systems which “embed compliance capabilities.” The smart contracts used in ERC-3643 incorporate mechanisms for permission control, identity verification, and transaction limitations. This directly supports KYC (Know Your Customer), AML (Anti-Money Laundering), and accredited investor verification, which are required by current securities regulations.

The most remarkable quality of ERC-3643 is that it prioritizes “compliance as code.” It uses a decentralized identity framework called ONCHAINID that requires all token holders to verify their identity and follow rules for holding and transferring tokens. Regardless of what blockchain the token resides on, these assets can only be owned by users who adhere to KYC requirements and accredited investor qualifications. Smart contracts handle compliance checks, eliminating the reliance on centralized audits, manual records, or off-chain procedures.

This is a major shift from ERC-20, which evolved from a fully accessible, permissionless on-chain native system where any wallet address can freely send and receive tokens, making it a fully fungible tool. In contrast, ERC-3643 focuses on high-value and closely regulated asset categories like securities, funds, and bonds. ERC-3643 emphasizes “who can hold” and “whether it is compliant,” making it a permissioned token standard. In short, ERC-20 is the free-flowing currency of the crypto world, whereas ERC-3643 is the compliant container for on-chain finance.

Currently, ERC-3643 has gained adoption with multiple countries and financial institutions throughout the world. Tokeny, a European digital securities platform, has been improving on the ERC-3643 standard for private market securitization in recent years. In June of this year, Tokeny announced their partnership with the digital securities platform Kerdo, with plans to build a blockchain-based private investment infrastructure by using ERC-3643, which includes asset types like real estate, private equity, hedge funds, and private debt.

ERC-3643 provides fundamental support for the partitioning, digitalization, and worldwide distribution of numerous assets, ranging from real estate to art collections and private equity to supply chain notes. Currently, it’s the only public blockchain token standard which combines on-chain identity verification, cross-border legal compatibility, programmable compliance, and integration opportunities with existing financial architectures.

Paul Atkins explained in his address that the future securities market must not only “operate on-chain” but also “comply on-chain.” ERC-3643 might be the bridge between the SEC and Ethereum, which ultimately connects TradFi and DeFi.

The Return of Entrepreneurs to the U.S.: Primary Markets Surge Again from On-Chain Offerings

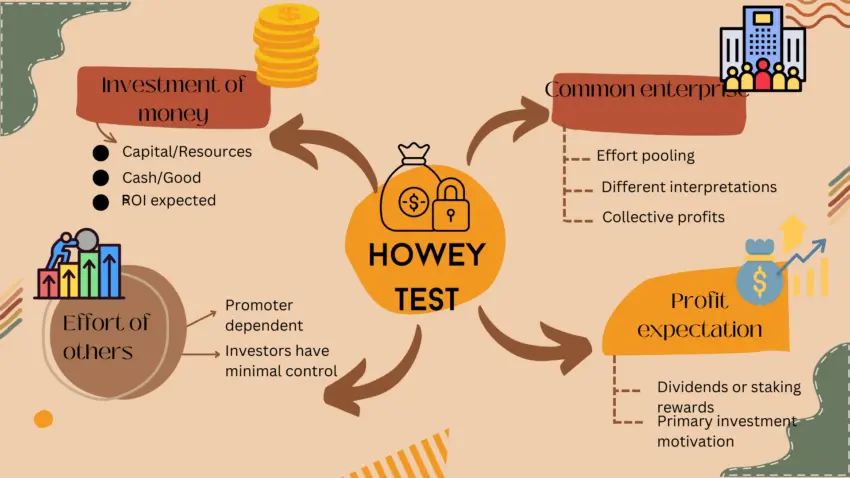

The Howey Test has long served as the main criteria to determine whether an asset should be classified as a security. It is comprised of four elements: a monetary investment, a common enterprise, the expectation of profits from the efforts of others, and the existence of said profits. A project that meets all four is considered a security and is bound by a series of securities law frameworks that include pre-issuance prospectuses, regulatory filings, and information disclosure.

Many projects have decided to forego the U.S. market to avoid regulatory risks due to the test’s vague requirements and inconsistent enforcement, even deliberately “blocking” U.S. users and withholding incentives and airdrops.

During the “Project Crypto” policy announcement, SEC Chairman Paul Atkins revealed that he will establish a reclassification standard for crypto assets. It provides understandable disclosure norms, exemption conditions, and safe harbor mechanisms for popular blockchain-based economic activities like airdrops, ICOs, and staking. The SEC will no longer regard “issuing tokens = securities” as the default stance but will rationally sort them into different categories. Such categories include digital commodities (like Bitcoin), digital collectibles (like NFTs), stablecoins, or security tokens based on their economic characteristics and providing relevant legal pathways.

This signals a key shift: project teams will not need to “pretend not to issue tokens,” nor will they have to use roundabout methods like foundations or DAOs to hide their incentive mechanisms. They will also no longer have to register their projects in the Cayman Islands. Teams that prioritize code and whose core foundation is technology will receive institutional recognition.

With the rapid development of emerging sectors such as AI, DePIN, and SocialFi, and the rising need for early-stage funding, this regulatory framework seeks to promote innovation. With this framework in place, more projects are expected to come back to the U.S. Instead of avoiding the market, crypto entrepreneurs may, once again, opt for the U.S. as their top choice for token issuance and fundraising.

Conclusion

“Project Crypto” is an all-encompassing set of systemic reforms instead of a single law. It imagines a future where token economies, decentralized software, and capital market compliance are seamlessly integrated. Paul Atkins is clear that regulation should pave the way for innovation and no longer stifle it.

This also sends the market an explicit indication of a policy shift. Whether it is DeFi, token fundraising, or Super Apps, the ultimate benefactor of these policy incentives will be whoever first responds to the U.S.-led revolution of the on-chain capital market.

Recommended Reading:

Solana and Base Founders Start a Debate: Does Content on Zora Have “Intrinsic Value”?

ChainCatcher advises readers to be sensible regarding blockchain. You should also increase your risk awareness and be cautious of virtual token issuances and speculations. All content on this site consists of market information or related party opinions. It does not offer investment advice. Please click “Report” if any sensitive data is encountered, and we will react immediately.